SGB Tax Benefits: Why It Beats Gold FD Post-Tax Returns

Gold is rarely bought only for return. In Indian portfolios, it also carries family memory, currency-hedge instincts, and distrust of market cycles. Yet when a high-income investor compares a Sovereign Gold Bond with a Gold FD, comfort has to meet post-tax arithmetic. The strongest SGB tax benefits come from a specific combination: gold-linked redemption value, 2.5% annual interest, demat convenience, and potential capital gains exemption for eligible holders. By the end, you'll know when SGB tax benefits beat Gold FD returns, when the 2026 tax change matters, and why secondary-market SGB purchases need extra care.

How SGB Tax Benefits Change Sovereign Gold Bond Taxation

Sovereign gold bond taxation differs from physical gold, gold ETFs, and bank deposits. SGB tax benefits are most visible at redemption, where similar pre-tax returns can produce different post-tax results.

Are SGB capital gains tax-free on maturity?

SGB capital gains can be tax-free at maturity, but only if the investor fits the current exemption conditions. From April 1, 2026, Section 70(1)(x) narrows SGB tax benefits to an individual who subscribed at original issue and held until maturity.

That means the cleanest case is not "any SGB held by anyone." It is an original-issue holding bought during the tranche window and held eight years.

If an investor bought at Rs 5,000 per gram and redeems at Rs 12,000, appreciation is Rs 7,000. Valid SGB tax benefits can shelter that gain, while many gold formats face capital gains tax.

What happens if I redeem SGB before maturity?

SGBs have an eight-year maturity, with premature redemption through RBI available after the fifth year on coupon dates. That improves liquidity, but differs from holding to maturity for the revised SGB tax benefits test.

After the 2026 amendment, early RBI redemption can become taxable because the wording focuses on holding from original issue "till maturity." A stock-exchange sale is also taxed as capital gains.

Treat tax-free SGB tax benefits as available only for original subscribers who can hold until scheduled maturity. If liquidity is likely in year five or six, use an after-tax exit value.

| SGB Holding Route | Likely Tax Treatment After April 1, 2026 | Planning Implication |

|---|---|---|

| Original subscriber holds till eight-year maturity | Capital gains may be exempt for an eligible individual | Best fit for long-term gold allocation |

| Original subscriber uses RBI premature redemption after year five | Capital gains may be taxable because maturity condition is not met | Model after-tax proceeds before exiting |

| Investor sells SGB on stock exchange | Taxable capital gains on transfer | Useful for liquidity, not for tax-free exit |

| Investor buys SGB from secondary market | Maturity exemption generally should not be assumed | Check discount, remaining coupon, and tax cost |

Why Gold FD Returns Need a Post-tax and Access Check

Gold FD returns can look intuitive: deposit gold, receive a certificate, and earn interest. The comparison with SGB tax benefits is harder because Gold FDs sit inside the Gold Monetisation Scheme, where availability and purity conversion matter.

How are Gold FDs taxed in India?

Under the Gold Monetisation Scheme, deposit certificates have historically received favourable tax treatment. Interest on eligible certificates is exempt from income tax, and the certificates are excluded from the definition of capital asset.

That sounds stronger than SGB tax benefits because SGB interest is taxable. Yet tax is only one part of the return stack. A Gold FD usually requires physical gold to undergo testing and melting.

Like choosing between a locker key and a demat statement, the better option depends on what you hold. For fresh financial exposure, SGB tax benefits are usually cleaner.

Why STBD and discontinued MLTGD matter for comparison

The Gold Monetisation Scheme has several moving parts. Short Term Bank Deposits, or STBDs, can continue at banks' discretion. Medium and Long Term Government Deposit components, known as MLTGD, were discontinued for fresh mobilisation from March 26, 2025.

That affects comparability. Older Gold FD comparisons assumed medium or long government-backed deposits would remain available. A 2026 investor may instead find only short-tenure bank options or no attractive Gold FD route.

SGBs also have an availability issue because no new tranche may be open. Existing bonds trade on the secondary market, but those purchases no longer receive the same maturity exemption.

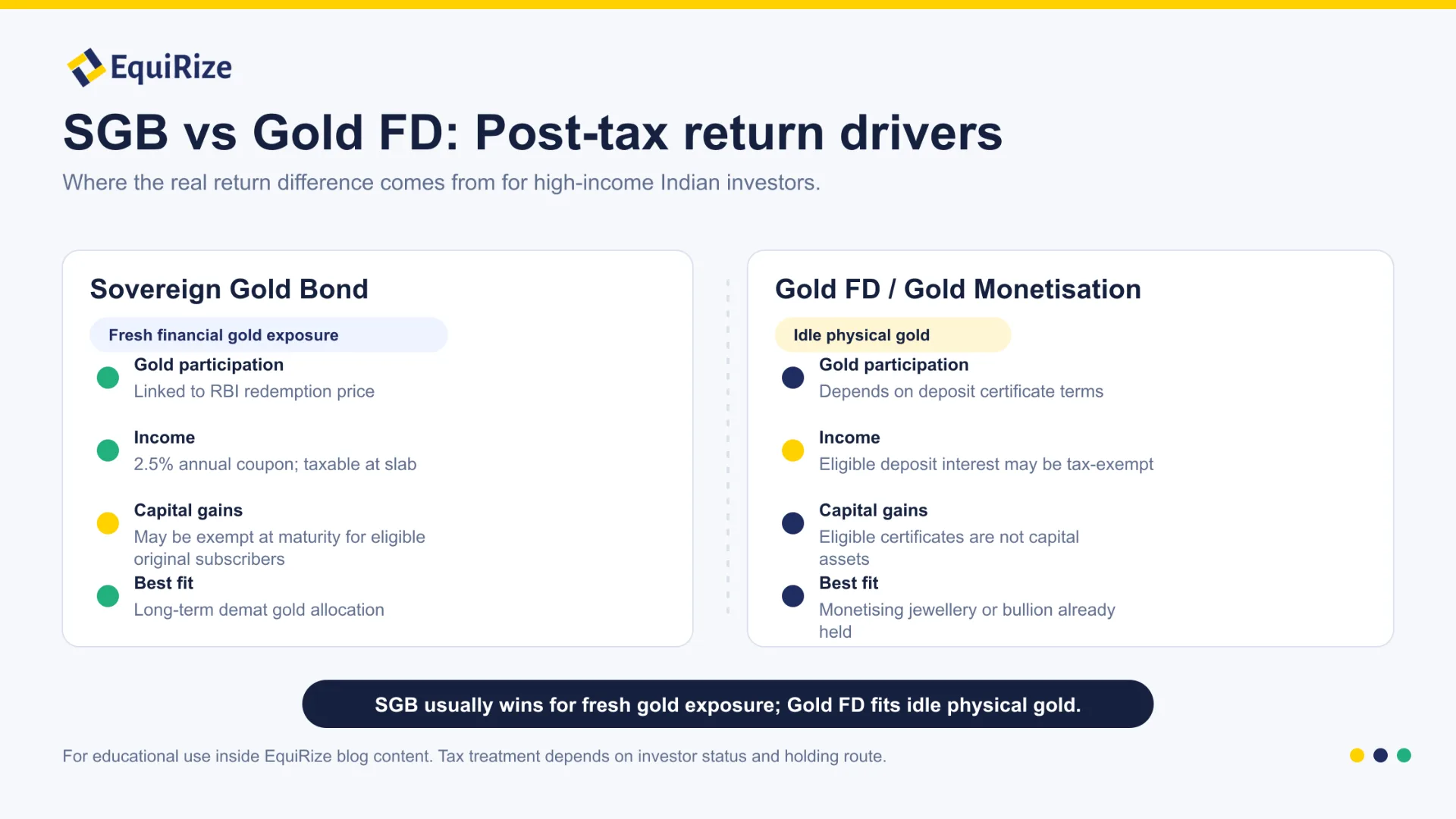

| Feature | Sovereign Gold Bond | Gold FD Under Gold Monetisation Scheme |

|---|---|---|

| Starting asset | Fresh rupee investment or existing listed SGB purchase | Existing physical gold, jewellery, coins, or bullion |

| Income treatment | 2.5% annual interest taxable at slab rate | Eligible deposit interest may be tax-exempt |

| Capital gains treatment | Eligible original-issue maturity redemption may be exempt | Eligible deposit certificates are not treated as capital assets |

| Liquidity | Exchange sale possible in demat; RBI premature redemption after year five | Depends on deposit category, bank process, and scheme availability |

| Best fit | Fresh financial gold exposure | Monetising idle physical gold |

How SGB Interest Taxable Income Affects Post-tax Returns Gold

Post-tax returns gold comparisons often mix capital appreciation and income. SGB tax benefits include taxable interest and potentially exempt capital appreciation, so the right metric is total after-tax value.

Is SGB interest taxable in India?

Yes, SGB interest taxable income is reported under income from other sources and taxed at slab rate. The coupon is 2.5% per annum on issue price, so a Rs 10 lakh subscription produces Rs 25,000 before tax.

For someone in the 30% slab, ignoring surcharge and cess, that coupon becomes Rs 17,500 after tax. Over eight years, post-tax coupon value is Rs 1.40 lakh.

That tax reduces the headline benefit, but it doesn't erase SGB tax benefits. Physical gold has no coupon. A Gold FD may have tax-free interest, yet rate and availability vary.

Why a 30% slab investor still may prefer SGB

Consider a high-income investor allocating Rs 10 lakh to gold exposure. If SGBs are bought at original issue and held to maturity, the investor receives taxable interest plus maturity value linked to gold. If gold rises 8% annually, the eligible capital component may compound without capital gains tax.

A Gold FD may offer tax-free interest, but the investor first needs eligible physical gold and must accept the scheme's process. SGB tax benefits can still win because gold-price appreciation may escape tax at maturity.

This is the heart of SGB tax benefits for high income investors: tax drag falls on the 2.5% coupon, not necessarily on the full gold appreciation. For a 30% slab investor, that asymmetry can matter.

When the SGB Redemption Tax Exemption Beats Gold Investment Tax India

Gold investment tax India rules differ sharply across instruments. Physical gold and many gold fund structures face capital gains taxation, while SGB tax benefits can create a zero-tax capital appreciation outcome for the right holder.

Should I buy an SGB on the secondary market after 2026?

Buying SGB from the secondary market after 2026 needs a sharper lens. The revised exemption is tied to original subscription and maturity holding, so a stock-exchange buyer should not assume SGB tax benefits merely because the instrument is an SGB.

That does not make secondary-market SGBs useless. They may trade at a discount or premium to implied gold value, and they still carry the 2.5% coupon based on original issue price. A discount can offset some tax disadvantage.

The right test is numerical: purchase price, expected maturity value, remaining coupon, likely tax, costs, and liquidity. A steep premium can weaken the post-tax case; a discount near maturity may still be rational.

SGB vs Gold FD: Which is better after tax?

SGB vs Gold FD which is better after tax depends on the investor's starting point. For fresh allocation, SGB tax benefits are often stronger when bought at original issue and held to maturity.

For an investor with idle jewellery or bullion, a Gold FD can make sense if the family is comfortable converting physical gold into a deposit certificate. Its tax treatment can be efficient, but the process is less liquid than buying a demat security.

In plain terms, SGB tax benefits suit investors who want financial gold exposure. Gold FDs suit households with idle physical gold. A bank FD is not a gold product; it offers rupee interest but no gold-price participation.

Real-world Scenarios: How HNIs and NRIs Use SBG Tax Benefits

The best product is rarely universal. SGB tax benefits depend on liquidity needs, residency, and the tax-relevant holding period.

Ananya, a salaried executive building a gold allocation

Ananya is 42, works in Bengaluru, and wants to allocate Rs 12 lakh to gold without storing coins or jewellery. She is in the 30% tax slab and can accept an eight-year lock-in.

For her, SGB tax benefits are strong if a fresh tranche opens or if she already holds original-issue SGBs. On Rs 12 lakh, the annual coupon is Rs 30,000 before tax and about Rs 21,000 after tax at a simplified 30% rate. The bigger attraction is exempt eligible maturity gains.

Rajiv and Meera, HNIs evaluating family jewellery deposits

Rajiv and Meera are 58 and 55, based in Mumbai, with around 700 grams of inherited jewellery that no one wears. A Gold FD could convert idle gold into an earning asset, but the family is uncomfortable melting heirloom pieces.

They split the decision. Jewellery with emotional value stays outside the portfolio. For incremental exposure, they prefer SGB tax benefits when available, because pricing is transparent. Gold FD becomes a monetisation tool for unwanted physical gold.

Vikram, an NRI inheriting SGBs from a parent

Vikram lives in Singapore and inherits SGBs from his late father, who subscribed during an RBI issue. RBI's FAQ permits an NRI nominee to hold the security until early redemption or maturity, though proceeds are not repatriable.

His tax question is different from Ananya's. Because the 2026 exemption focuses on the original subscriber holding until maturity, Vikram should not assume the same SGB tax benefits apply to inherited holdings. He needs India tax advice before maturity or sale.

How to Decide if SGB Tax Benefits are Worth it After 2026

This is the section to use before buying, holding, or exiting. The right answer is not "SGB always wins"; it is whether your route, tenure, and liquidity needs allow the tax structure to work in your favour.

Check whether you qualify for maturity exemption

Start with the exemption test. Did you subscribe at original issue as an eligible individual, and can you hold until scheduled maturity? If yes, the SGB redemption tax exemption may be central to your post-tax return. If you bought from the secondary market, inherited the bond, or plan to redeem early, model capital gains tax instead of assuming a clean tax-free exit.

Next, separate income from appreciation. SGB interest taxable income should be added to your slab income each year, while capital appreciation depends on the exit route. This distinction matters for HNIs because a 30% slab tax on the coupon is manageable, but losing exemption on a large gold-price gain can change the investment case.

Compare SGB, Gold FD, and bond allocation after tax

Use SGBs for gold exposure, not as a substitute for every fixed-income allocation. A Gold FD may be suitable when the starting point is idle physical gold. A bond or NCD may be more appropriate when the objective is predictable cash flow, defined tenor, and credit-risk selection.

Before allocating, compare three numbers: expected after-tax SGB value at maturity, realistic Gold FD proceeds after operational constraints, and available bond yields on EquiRize for the same holding period. That gives a better decision than comparing headline rates. For many high-income investors, SGB tax benefits justify a gold sleeve, while curated bonds and NCDs still do the core income-generation work.

Conclusion

The core takeaway is simple: SGB tax benefits beat Gold FDs on post-tax returns when the investor wants fresh financial gold exposure, buys at original issue, and can hold until maturity. Gold FDs remain useful for monetising idle physical gold, but they are less straightforward as a tool for fresh allocations. Before investing, check tranche availability, secondary-market premiums, and whether your route qualifies for the SGB tax benefits you are modelling.

For broader allocation, talk to a fixed-income expert on EquiRize and compare curated bond and NCD opportunities.