RBI Repo Rate and Bond Yields: What Investors Should Know

RBI Repo Rate and Bond Yields: What Investors Should Know

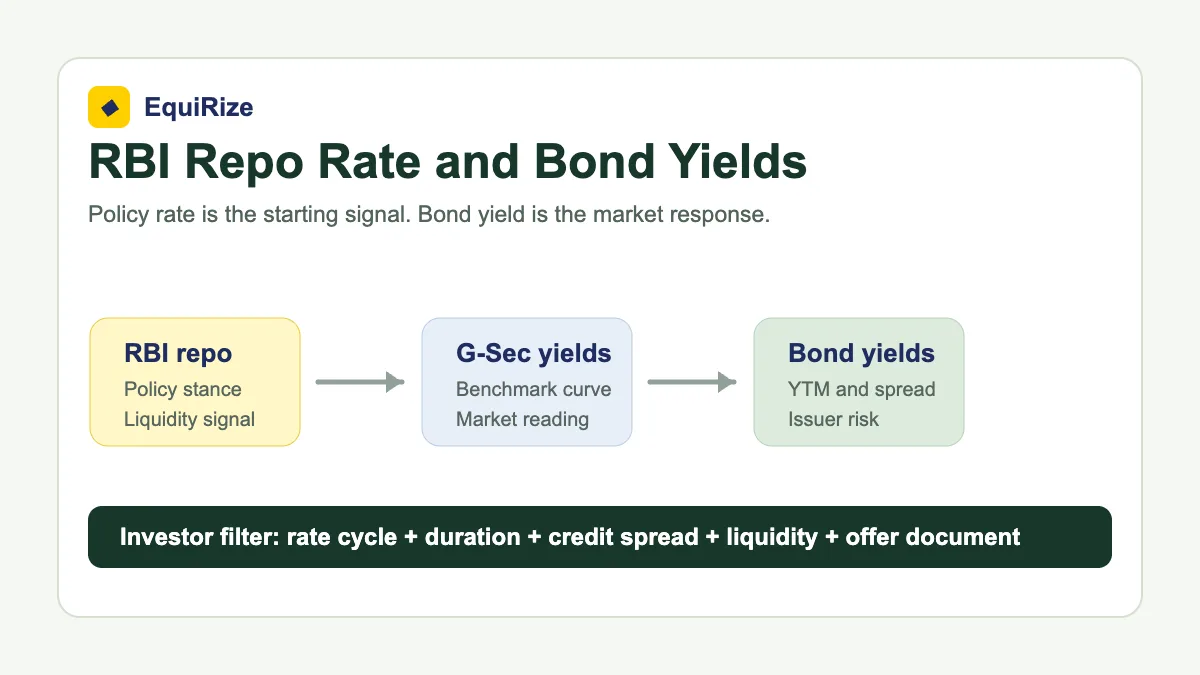

RBI repo rate and bond yields are connected, but they do not move like a light switch. The repo rate is the policy rate at which the Reserve Bank of India lends short-term funds to banks against securities. Bond yields are market prices expressed as returns.

That distinction matters.

When the RBI changes or pauses the repo rate, the bond market reads more than the number. It reads inflation, liquidity, growth signals, government borrowing, global rates, currency pressure, and what the Monetary Policy Committee may do next. At the time of drafting, the latest reported June 2026 policy decision kept the repo rate unchanged at 5.25% with a neutral stance, which makes investor interpretation especially important.

For retail investors comparing listed bonds, the question is not simply: "Will yields rise or fall?"

The better question is: "What part of this yield comes from the interest-rate cycle, and what part comes from issuer risk, tenure, liquidity, or structure?"

RBI Repo Rate Meaning for Bond Investors

The repo rate is a policy signal. It influences borrowing costs and liquidity across the economy, but it does not directly set the yield of every bond. Bond yields are formed in the market through demand, supply, credit perception, maturity, liquidity, and expected future rates.

Repo rate vs bond yield difference

The repo rate is an overnight policy rate used by the RBI in its liquidity framework. It is a short-term anchor.

A bond yield is the return an investor may earn from a bond at a given market price, assuming scheduled payments are made. For listed bonds, yield to maturity is often more useful than coupon because it reflects price, coupon, redemption value, and time left to maturity.

So, the repo rate is a policy input. Bond yield is a market output.

Why bond yields move after RBI policy

Bond yields may move after RBI policy because investors update expectations.

If the policy sounds inflation-worried, long-term yields may rise even when the repo rate is unchanged. If the policy sounds growth-supportive and inflation looks contained, yields may soften. Liquidity measures, government borrowing expectations, crude oil prices, rupee movement, and global bond yields can also affect Indian bond yields.

This is why a repo pause can still be followed by movement in G-Sec yields.

How investors should read RBI monetary policy

Do not read only the headline repo rate.

Read the stance, inflation commentary, liquidity guidance, growth outlook, and voting pattern. A neutral stance can mean the RBI wants flexibility. A pause after cuts can mean the market has already priced part of the easing cycle. A hike can signal inflation pressure or liquidity tightening.

For bond investors, tone often matters as much as the rate.

Repo Rate Impact on Bond Yields in India

The usual direction is simple: higher expected policy rates tend to push yields up, and lower expected policy rates tend to pull yields down. But the real market is messier. Different maturities react differently, and corporate bonds add issuer-specific risk on top of the rate cycle.

How repo rate affects bond yields in India

When the RBI raises the repo rate, banks and market participants often expect borrowing costs to rise. New bonds may need to offer higher yields to attract investors. Existing bonds with lower coupons may become less attractive in the secondary market.

When the RBI cuts the repo rate, market yields may soften if investors believe inflation is under control and liquidity is supportive. Existing bonds with relatively higher coupons may then become more attractive.

The word "may" is doing real work here. Bond yields also respond to fiscal supply, liquidity, foreign flows, inflation expectations, and global rates.

What happens to bond prices when repo rate rises

If market yields rise after a repo hike or a hawkish policy signal, prices of existing fixed-rate bonds generally fall.

Why? A bond paying an older, lower coupon has to trade at a lower price so that its yield becomes competitive with newer bonds. This impact is usually larger for long-duration bonds because investors are locked into the fixed coupon for longer.

If you plan to sell before maturity, this mark-to-market movement matters. If you hold until scheduled redemption, interim price changes may matter less, but issuer repayment risk remains.

What happens to bond prices when repo rate falls

If market yields fall after a repo cut or dovish signal, existing fixed-rate bonds with higher coupons may rise in price.

The older bond becomes attractive because new issuances may offer lower coupons or lower yields. Investors may be willing to pay more for the existing cash flows.

This is the classic bond price and yield relationship. Falling yields can support existing bond prices. Rising yields can pressure them.

Repo rate impact on government bond yields

Government bond yields are often the first layer of transmission. They reflect policy expectations, inflation, liquidity, and supply of government securities. Corporate bond pricing usually builds from this benchmark.

Bond Price and Yield Relationship: The Core Rule

Once you understand price and yield, the repo rate conversation becomes easier. A bond is not only an interest-paying instrument. It is also a tradable security whose market price can move before maturity.

Why bond prices and yields move opposite ways

Most plain fixed-rate bonds pay a set coupon on face value. If market yields rise, the fixed coupon looks less attractive. The bond price must fall for the effective yield to adjust upward.

If market yields fall, the fixed coupon looks more attractive. The bond price may rise because investors accept a lower yield for the same cash flows.

This inverse relationship is central to bond investing. It does not remove credit risk. It explains interest-rate sensitivity.

Coupon rate vs yield to maturity

Coupon rate is the stated interest rate on the bond's face value.

Yield to maturity is the estimated annualised return if the investor buys at the current price, holds until maturity, and scheduled payments happen. A bond can have a 9% coupon and a different YTM if it trades above or below face value.

When comparing listed bonds online, read YTM, maturity, price, coupon frequency, and redemption terms together.

Bond duration and interest rate risk

Duration measures a bond's sensitivity to interest-rate changes. Longer-duration bonds generally move more when yields change.

A short-maturity bond may see limited price movement from a rate change. A long-maturity bond can see a larger price move because its fixed cash flows stretch further into the future.

If you may need liquidity before maturity, duration is not academic. It affects your exit price.

Corporate Bond Yields and Repo Rate: What Changes for NCDs

Corporate bond yields and NCD yields are usually built from two broad parts: the benchmark rate environment and a credit spread. The repo rate can influence the benchmark layer. The issuer spread reflects credit quality, structure, liquidity, and investor appetite.

RBI repo rate impact on corporate bonds

When benchmark yields rise, corporate bonds often need to offer higher yields too. New NCDs may come with higher coupons or be priced at yields that reflect the new rate environment.

For existing corporate bonds, market prices may adjust if comparable new bonds offer better yields. The impact can be stronger when the bond has longer maturity, lower liquidity, or a coupon that looks less attractive after rate changes.

But repo rate is only one part of corporate bond pricing.

Credit spread can offset repo rate moves

A corporate bond yield can rise even if the repo rate is unchanged. That may happen if the issuer's credit spread widens due to weaker financials, sector stress, rating action, or low liquidity.

The reverse is also possible. A benchmark yield may rise, but a strong issuer's spread may narrow if demand improves.

This is why investors should not assume every high yield is simply a rate-cycle opportunity. Sometimes it is compensation for additional credit or liquidity risk.

Liquidity and rating still matter

Credit rating, rating rationale, secured or unsecured status, covenants, seniority, liquidity, call options, and repayment schedule can all affect a bond's risk-return profile.

Two bonds with the same coupon can carry different risk. Two bonds with the same rating can trade at different yields. A higher displayed yield may be explained by weaker liquidity, longer tenure, lower rating, or more complex structure.

Read the bond term sheet and offer document before treating yield as the main decision point.

Worked Example: Repo Rate, Yield and Bond Price

The following is an illustrative, hypothetical example. It is not a recommendation, endorsement, or reference to any live issuance.

What happens to an existing bond when market yields rise

Assume an investor holds a 5-year fixed-rate bond with a 9.00% annual coupon and face value of Rs 1,00,000.

Now assume market yields for similar bonds move from 9.00% to 10.00% after a hawkish rate environment. A new investor can find comparable bonds yielding 10.00%. The older 9.00% coupon bond must usually trade below face value to offer a competitive yield.

The investor still receives the scheduled coupon if the issuer pays as promised. But if the investor sells before maturity, the market price may be lower.

What happens when yields soften later

Now assume market yields soften from 9.00% to 8.25%.

The same 9.00% coupon becomes more attractive. Investors may be willing to pay above face value because the bond offers higher cash flow than the new market yield.

That does not make the bond risk-free. It only shows how rate movement can affect price.

Why holding period changes the answer

If you hold until maturity and the issuer pays on schedule, the path of market price may not affect your expected cash flows.

If you sell before maturity, market yield at the sale date matters. Repo rate changes, yield curve shifts, credit spread changes, and liquidity can all affect the exit price.

Investor Checklist for Reading Bond Yields in India

Use RBI policy as context, not as a single buy-or-wait signal. A cleaner bond review starts with your time horizon and then checks whether the yield is paying you enough for the risks you are accepting.

Should I buy bonds when repo rate is high?

A higher repo-rate environment may offer higher yields on new bonds, but timing the rate cycle is difficult. If yields fall later, existing bonds may benefit through price appreciation. If yields rise further, existing prices may face pressure.

The practical approach is to match maturity with your financial goal, diversify across issuers where suitable, and avoid over-concentrating in one high-yield instrument.

Checks before comparing listed bonds online

Before investing, check:

- Yield to maturity, not only coupon rate

- Remaining maturity and duration

- Coupon frequency and record dates

- Credit rating and rating rationale

- Secured or unsecured structure

- Seniority, covenants, and call or put options

- Liquidity and likely exit route before maturity

- Tax treatment based on your situation

- Offer document, term sheet, and risk factors

- Whether the platform is a SEBI-registered OBPP

On EquiRize, investors can compare listed bond opportunities with issuer details, ratings, maturities, coupon schedules, indicative yields, and offer documents in one flow.

Rate-Cycle Decision Table for Bond Investors

| Market Situation | What it May Mean | Investor Check |

| Repo rate rises | Borrowing costs and market yields may move higher | Check duration risk before buying long-maturity bonds |

| Repo rat falls | Existing higher-coupon bonds may become more valuable | Check whether future reinvestment yields may be lower |

| Repo rate paused | Market looks for clues in inflation and liquidity commentary | Read the RBI stance, not just the headline rate |

| G-sec yields rise while repo is unchanged | Market may be pricing inflation, supply, liquidity, or global risks | Separate benchmark move from issuer risk |

| Corporate yield rises sharply | Credit spread or liquidity premium may be widening | Review rating rationale, financials, security, and offer document |

| Very high yield vs peers | Extra yield may signal extra risk | Avoid relying on yield alone |

This table is a practical filter. It does not replace due diligence. It simply keeps the rate-cycle question in the right place: useful, but not sufficient.

RBI Repo Rate and Bond Yields: Final Take

RBI repo rate and bond yields should be read together, but never treated as the same thing. Repo rate is the policy anchor. Bond yield is the market's price for money, time, inflation, liquidity, and credit risk.

For investors, the useful habit is simple: look beyond the headline yield. Ask what is driving it. Is it the rate cycle? Duration? Issuer credit? Liquidity? Structure? Tax? The answer tells you whether the yield fits your portfolio or only looks attractive on the screen.