OBPP License in India: SEBI Rules for Safer Bond Investing

India's listed bond market has become easier to access online, but access alone is not the same as investor protection. A high coupon, familiar issuer name, or polished dashboard does not tell you whether the platform selling the bond operates inside a recognised regulatory framework. That is why the OBPP license matters. For investors comparing bonds, NCDs, and fixed deposits, understanding the OBPP framework helps separate regulated digital bond access from informal distribution.

This guide explains what the license means, how SEBI OBPP regulations work, what they do not protect against, and how to evaluate a SEBI-registered bond platform before investing.

OBPP License in India: Meaning, Full Form, and Scope

An OBPP license refers to the regulatory permission required to operate as an Online Bond Platform Provider in India. In practical terms, an online bond platform provider is a digital platform that enables investors to discover, compare, and transact in eligible debt securities through a regulated market route.

SEBI introduced the OBPP framework to bring structure to online bond distribution. Before this framework, bond access was often relationship-led, scattered across private networks, or presented through platforms where the investor could not easily identify the intermediary's role, regulatory status, or grievance route.

The OBPP framework changes that operating standard. A platform that acts as an OBPP must be linked to the recognised securities-market ecosystem, comply with applicable exchange and SEBI rules, and follow defined processes around disclosures, order handling, investor onboarding, and reporting.

For a fixed-income investor, the key point is this: an OBPP is not merely a website that displays yields. It is a regulated access layer for listed debt securities, including bonds and NCDs, where the platform's conduct is subject to oversight.

SEBI OBPP Regulations for Bond Safety

SEBI OBPP regulations matter because fixed-income products are often misunderstood as simple "interest products." In reality, bonds involve issuer credit risk, market risk, liquidity risk, documentation risk, and sometimes complex security or repayment structures.

When distribution happens informally, investors may see only the attractive parts: coupon rate, potential yield, brand name, or short maturity. What can get buried are the risk factors, rating rationale, liquidity limits, call features, security cover, debenture trustee details, and conflict-of-interest disclosures.

A regulated bond platform is expected to bring discipline to this process. It should display relevant bond information, support KYC and onboarding, route eligible orders through recognised market infrastructure, provide transaction records, and operate under defined compliance obligations.

This improves bond platform safety at the process level. It reduces the chance that an investor is dealing with an opaque distributor, unclear counterparty, or undocumented transaction path.

However, SEBI regulation does not turn a risky issuer into a safe issuer. The framework improves platform accountability; it does not remove the need to analyse the bond.

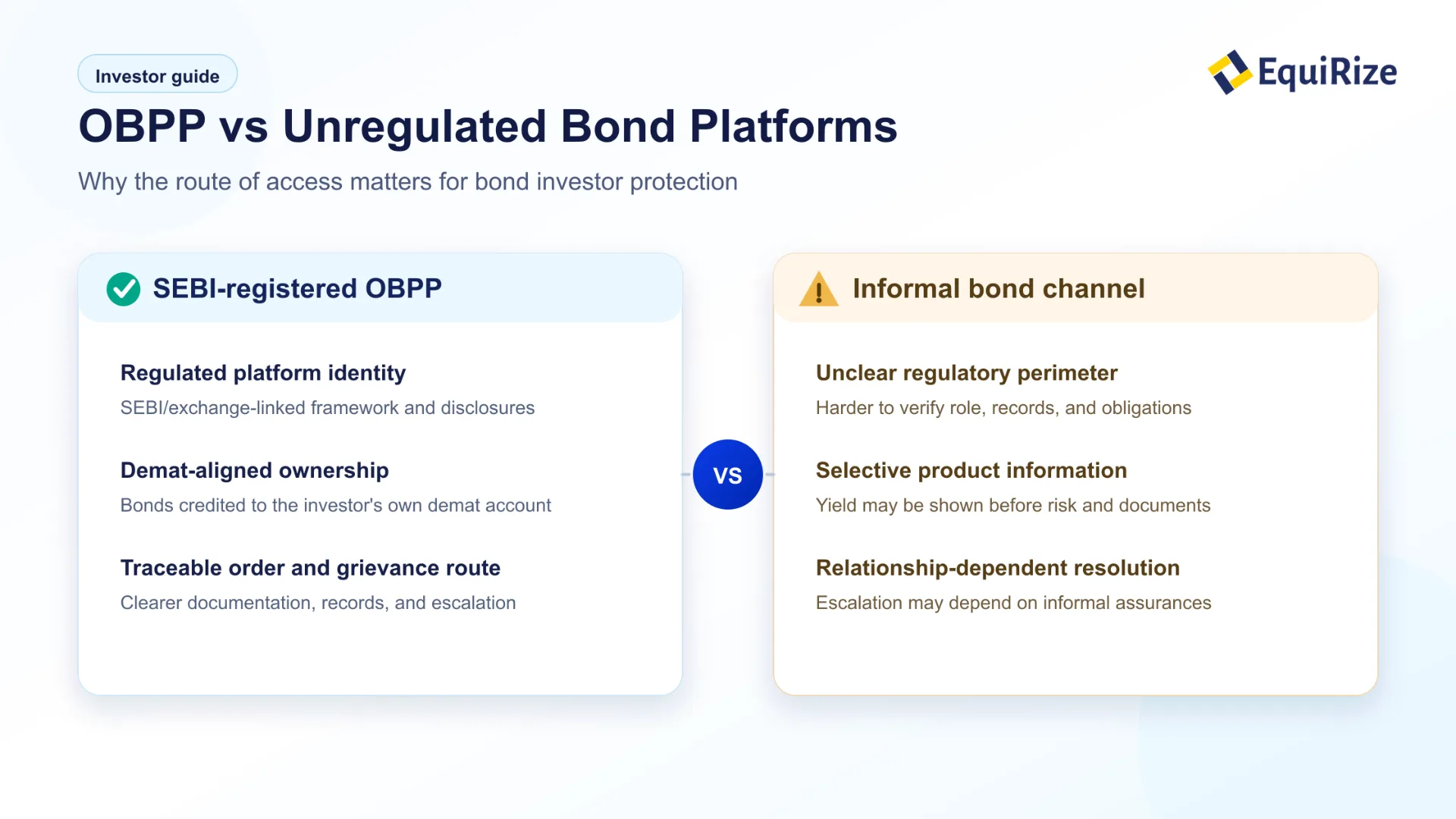

SEBI vs Unregulated Bond Platforms: Investor Protection

The easiest way to understand the OBPP license is to compare a SEBI-registered bond platform with an unregulated distribution channel.

| Factor | SEBI-registered OBPP | Unregulated or informal channel |

|---|---|---|

| Regulatory perimeter | Operates under SEBI and exchange-linked obligations | May operate outside a clear securities-market framework |

| Product display | Expected to show key instrument details and disclosures | Information may be selective or sales-led |

| Order route | Uses recognised market infrastructure for eligible securities | May rely on manual, private, or unclear transaction flows |

| Investor records | Transaction trail and platform-level records should exist | Documentation quality may vary materially |

| Custody | Bonds are held in the investor's demat account | Custody and ownership may be harder to verify |

| Grievance route | Defined platform and regulatory escalation channels | Often relationship-dependent |

| Risk reduction | Reduces process, disclosure, and platform conduct risk | Higher operational and information-asymmetry risk |

This comparison is important for HNIs, NRIs, salaried professionals, and IFAs because fixed-income mistakes are rarely dramatic on day one. They usually emerge later: unclear allotment, poor exit liquidity, missing documents, misunderstood risk, or difficulty escalating a complaint.

An OBPP license does not make every listed bond suitable. It makes the route of access more transparent and accountable.

How an Online Bond Platform Provider Works for Investors

An online bond platform provider brings bond discovery and transaction access into a digital workflow. The interface may feel simple, but the underlying process should be structured.

Step 1: KYC and Demat-Based Investor Onboarding

The investor completes onboarding requirements, including KYC and demat-linked details. This is important because listed bonds and NCDs are securities, not app-based deposits. The investor's legal identity, bank details, and demat account must align with the transaction.

Step 2: Bond, NCD and Yield Comparison

The investor can review available securities using parameters such as issuer name, credit rating, coupon rate, maturity date, face value, minimum investment amount, payment frequency, and indicative yield to maturity.

YTM is useful for comparison, but it is not a promised outcome. It assumes the investor buys at the displayed price, holds as assumed, and the issuer makes scheduled coupon and principal payments.

Step 3: Bond Order Placement and Execution

For eligible listed debt securities, the order should move through recognised market infrastructure rather than an undocumented private transfer. This creates a clearer audit trail and helps align the transaction with exchange and clearing processes.

Step 4: Settlement and Demat Credit of Bonds

Once executed and settled, the bond should be credited to the investor's own demat account. The platform does not become the owner of the security. This custody distinction is one of the most important investor safeguards under a regulated bond platform model.

Step 5: Coupon, Maturity and Rating Monitoring

After investing, the investor should monitor coupon dates, maturity date, credit rating changes, issuer announcements, and any corporate actions. A strong platform experience should help organise information, but the investor still needs to review portfolio concentration and issuer risk.

Demat Holding in OBPP Bond Investments

Yes, bonds bought through an OBPP route are typically held in the investor's demat account after settlement. This is a major difference between regulated securities-market access and informal distribution.

Demat holding matters for three reasons.

First, ownership is recorded through the depository system rather than relying only on platform screenshots or relationship-manager confirmations.

Second, the investor can independently view holdings through demat statements, subject to depository and broker reporting processes.

Third, the platform does not need to hold the investor's securities in its own name. That reduces custody confusion and makes the investor's relationship with the security clearer.

This does not remove credit risk. If the issuer defaults or delays payment, demat holding alone cannot solve that. But it does reduce operational ambiguity around whether the investor actually owns the bond.

What SEBI-Registered Bond Platforms Protect Against

SEBI OBPP regulations are best understood as guardrails around platform conduct and transaction processes. They are not insurance on the underlying bond.

The framework helps investors by improving:

- Regulatory accountability: the platform operates within a defined SEBI and exchange-linked structure.

- Disclosure discipline: key instrument details and risk information should be available before investing.

- Transaction traceability: order, deal, and settlement records are easier to document.

- Role clarity: the investor can better understand whether the platform is facilitating access rather than issuing the bond.

- Grievance escalation: complaints can move through platform processes and recognised investor redressal routes.

For investors used to bank FDs, this distinction can feel subtle but important. In a bank FD, the investor has a deposit relationship with the bank. In a listed bond, the investor owns a security issued by a borrower. The platform is the access route, not the repayment source.

That is why regulation of the platform is necessary but not sufficient. You still need issuer diligence.

OBPP License Limitations: Credit Risk and Liquidity

The most common error is assuming that a SEBI-registered bond platform makes the bond itself low-risk. That is not correct. An OBPP license does not:

- remove issuer credit risk;

- assure coupon or principal payment;

- create exit liquidity in the secondary market;

- prevent credit-rating downgrades;

- make a high-yield bond suitable for every investor;

- replace tax, legal, or investment advice;

- mean SEBI endorses a specific issuer or instrument.

This is where sophisticated investors should separate platform risk from instrument risk.

Platform risk asks: Is the route regulated, transparent, documented, and accountable?

Instrument risk asks: Is this issuer financially strong enough to pay on time, and does this bond fit my portfolio?

The OBPP framework helps with the first question. The second still requires analysis of credit rating, rating rationale, financials, maturity, security cover, cash-flow timing, sector risk, and liquidity.

OBPP Bonds vs Fixed Deposits: How Investors Should Compare

FD comparisons are natural because many investors discover bonds while searching for stable non-equity returns. But bonds and FDs are not the same product.

A bank FD is a deposit placed with a bank. A corporate FD is a deposit-like fixed-income product issued by a company or NBFC under its applicable framework. A bond or NCD is a debt security held in demat form, usually with tradable or listed characteristics depending on the issue.

When comparing a bond on a SEBI-registered bond platform with a fixed deposit, evaluate:

| Question | Fixed Deposit | Bond or NCD through OBPP |

|---|---|---|

| Return metric | Interest rate | Coupon and indicative YTM |

| Legal form | Deposit | Debt security |

| Holding format | Deposit account or receipt | Demat security |

| Liquidity | Premature withdrawal terms may apply | Secondary-market sale depends on liquidity and price |

| Risk driver | Issuer/bank strength and FD terms | Issuer credit, price, liquidity, and structure |

| Income timing | Usually chosen at booking | Defined by coupon schedule |

| Evaluation need | Rate, issuer, tenure, premature withdrawal | Rating, YTM, maturity, liquidity, covenants, security, documents |

For conservative investors, FDs may still fit short-term parking or operational simplicity. Bonds may fit investors seeking defined maturities, periodic coupon income, and potential yield above comparable deposits, subject to additional risk.

The right question is not "Are bonds better than FDs?" It is "What risk am I taking for the incremental potential yield, and is the platform route regulated?"

How to Choose a SEBI-Registered Bond Platform in India

Choosing a bond investment platform India investors can trust should involve more than comparing visible yields. A platform with high-quality bond discovery should help investors make better decisions, not just faster ones.

Verify SEBI Registration and Exchange Membership

Verify whether the platform or associated entity is SEBI-registered and appears in the relevant exchange or SEBI-linked OBPP records. The platform should clearly disclose its legal entity name, SEBI registration number, exchange membership details, compliance officer, and grievance process.

Compare Listed Bonds, NCDs and Fixed Deposits Separately

A credible platform should help you distinguish between listed bonds, NCDs, government securities, corporate fixed deposits, and other fixed-income products. It should not blur product structures merely because all of them sit under the broad "fixed income" label.

Check ISIN, Coupon, YTM, Rating and Maturity Data

Before investing, you should be able to view issuer name, ISIN, coupon rate, coupon frequency, maturity, credit rating, rating agency, price, accrued interest treatment, indicative YTM, minimum investment, security status, and offer documents.

Review Credit Risk and Liquidity Risk Disclosures

Good risk communication is specific. It does not simply say "fixed income is stable." It explains credit risk, liquidity risk, interest-rate risk, reinvestment risk, concentration risk, and the limits of indicative returns.

Assess Grievance Redressal and Post-Investment Support

For HNIs, NRIs, and IFAs, post-investment support matters. The platform should make it easy to track holdings, coupon dates, maturity timelines, documents, and escalation routes. A soft CTA such as "talk to a fixed-income expert" is useful only when the expertise is backed by transparent product information.

Bond Due Diligence Checklist for OBPP Investors

The OBPP license helps you assess the platform. The bond still deserves its own checklist.

Check Issuer Credit Rating and Rating Rationale

Start with the issuer's legal name, business model, ownership, sector, financial profile, leverage, and recent rating rationale. Do not stop at the rating symbol. Ratings are opinions, can change, and may not fully capture liquidity or event risk.

Compare Coupon Rate, YTM and Maturity Date

Compare coupon rate with indicative YTM. A bond may trade above or below face value, so coupon and YTM can differ. Check the maturity date, call or put features, coupon frequency, and whether the cash-flow schedule matches your needs.

Review Secured vs Unsecured Bond Structure

Review whether the bond is secured or unsecured, senior or subordinated, and whether there is a debenture trustee. Security cover can matter in recovery scenarios, but it does not make repayment automatic.

Understand Secondary-Market Liquidity and Exit Route

If you may need money before maturity, liquidity matters as much as yield. Listed status does not ensure an immediate buyer at your desired price. Thinly traded bonds may have wider bid-ask spreads.

Match the Bond to Portfolio Concentration Limits

If you may need money before maturity, liquidity matters as much as yield. Listed status does not ensure an immediate buyer at your desired price. Thinly traded bonds may have wider bid-ask spreads.

EquiRize as a SEBI-Registered Bond Platform for Fixed Income

EquiRize is positioned for investors who want access to fixed-income opportunities through a SEBI-registered platform rather than informal distribution. For the right investor, this can make bond discovery more organised, transparent, and comparable.

On EquiRize, the core value should not be framed as chasing the highest visible yield. The stronger proposition is regulated access, clearer product information, demat-aligned holding, and the ability to compare bonds, NCDs, and fixed deposits with a more disciplined fixed-income lens.

For salaried professionals, that may mean building a non-equity allocation beyond traditional FDs. For HNIs, it may mean matching maturity buckets with treasury needs. For NRIs, it may mean evaluating rupee fixed-income exposure with clearer documentation. For IFAs, it may mean using a regulated platform workflow while still applying suitability and risk analysis for clients.

Investors can explore curated bond deals, compare fixed-income options, or talk to a fixed-income expert before making an allocation decision.

OBPP Investor Red Flags Before Buying Bonds Online

Even when a platform is SEBI-registered, the investor's decision should not be reduced to the highest visible indicative yield. A strong article on OBPP bond safety should help readers recognise warning signs before they invest.

Red Flag 1: Yield Is Highlighted More Than Credit Risk

If the first thing you see is the potential yield and the last thing you see is the issuer's credit profile, pause. A bond's coupon rate or indicative YTM is meaningful only when read alongside issuer quality, rating rationale, security cover, repayment structure, liquidity, and maturity.

For fixed-income investors, higher yield is usually compensation for some combination of credit risk, liquidity risk, longer tenor, structural complexity, or weaker market demand. A SEBI-registered bond platform should make those trade-offs visible.

Red Flag 2: Product Labels Are Blurred Across Bonds and FDs

Bonds, NCDs, bank FDs, and corporate fixed deposits may all sit within fixed income, but they are not interchangeable. The legal form, holding format, liquidity route, risk driver, and investor protection framework can differ materially.

If a platform presents every product as a simple "fixed return" option without explaining these differences, the investor may underestimate risk. A better platform experience separates listed debt securities, corporate FDs, and bank FDs clearly.

Red Flag 3: Demat, ISIN and Documents Are Hard to Find

For listed bond investing, basic instrument data should be easy to review. Investors should be able to identify the issuer, ISIN, coupon schedule, maturity date, rating, offer document, debenture trustee details where applicable, and the demat-linked holding process.

If these details are missing, buried, or available only after a sales conversation, the platform experience is not supporting informed fixed-income decision-making.

Red Flag 4: Exit Liquidity Is Treated as Automatic

Listed bonds may have a secondary-market route, but that does not mean every bond can be sold instantly at a favourable price. Liquidity depends on demand, issue size, remaining maturity, issuer profile, market conditions, and bid-ask spread.

Investors who may need funds before maturity should evaluate exit assumptions before investing. In many cases, holding to maturity may be the cleaner plan, provided the issuer continues to meet payment obligations.

Red Flag 5: Suitability Is Ignored for HNIs, NRIs and IFAs

A bond that suits one investor may be unsuitable for another. HNIs may need issuer and sector diversification. NRIs may need additional attention to account structure, tax treatment, repatriation rules, and documentation. IFAs may need a clear suitability trail for client portfolios.

The OBPP license improves the platform route, but suitability still depends on the investor's time horizon, liquidity needs, risk tolerance, tax position, and portfolio concentration.

Conclusion: Use the OBPP License as a Starting Filter

The OBPP license is an important first filter when choosing a bond investment platform India investors can rely on. It tells you that the platform operates within a SEBI-linked framework, with clearer expectations around disclosures, records, transaction processes, and investor escalation. But the license is not a substitute for bond due diligence. Before investing, compare the bond with relevant FDs, understand coupon and indicative YTM, review issuer credit quality, and check whether the maturity fits your portfolio. To go deeper, explore curated bond deals on EquiRize or talk to a fixed-income expert.

This content is for informational purposes only and does not constitute investment advice. Please consult a SEBI-registered advisor before investing.