NCD vs Corporate Bond: How Indian Investors Should Pick

Many Indian investors first encounter corporate debt through a public NCD issue advertised by a finance company, then later see "corporate bonds" on a bond platform and assume these are separate products. The NCD vs corporate bond question is useful, but only if framed correctly. An NCD, or non-convertible debenture, is usually one form of corporate bond; not every corporate bond is marketed as an NCD. By the end, you'll know how the terms overlap, what actually changes your risk, and how to use the NCD vs corporate bond frame to compare yield, rating, security, liquidity, and tax before choosing an instrument.

NCD vs Corporate Bond: Non-Convertible Debentures Explained

The first decision is semantic, but it has practical consequences. If you treat NCD vs corporate bond as two unrelated products, you may compare the wrong features and miss the real drivers of return and risk.

What is the difference between NCD and corporate bond?

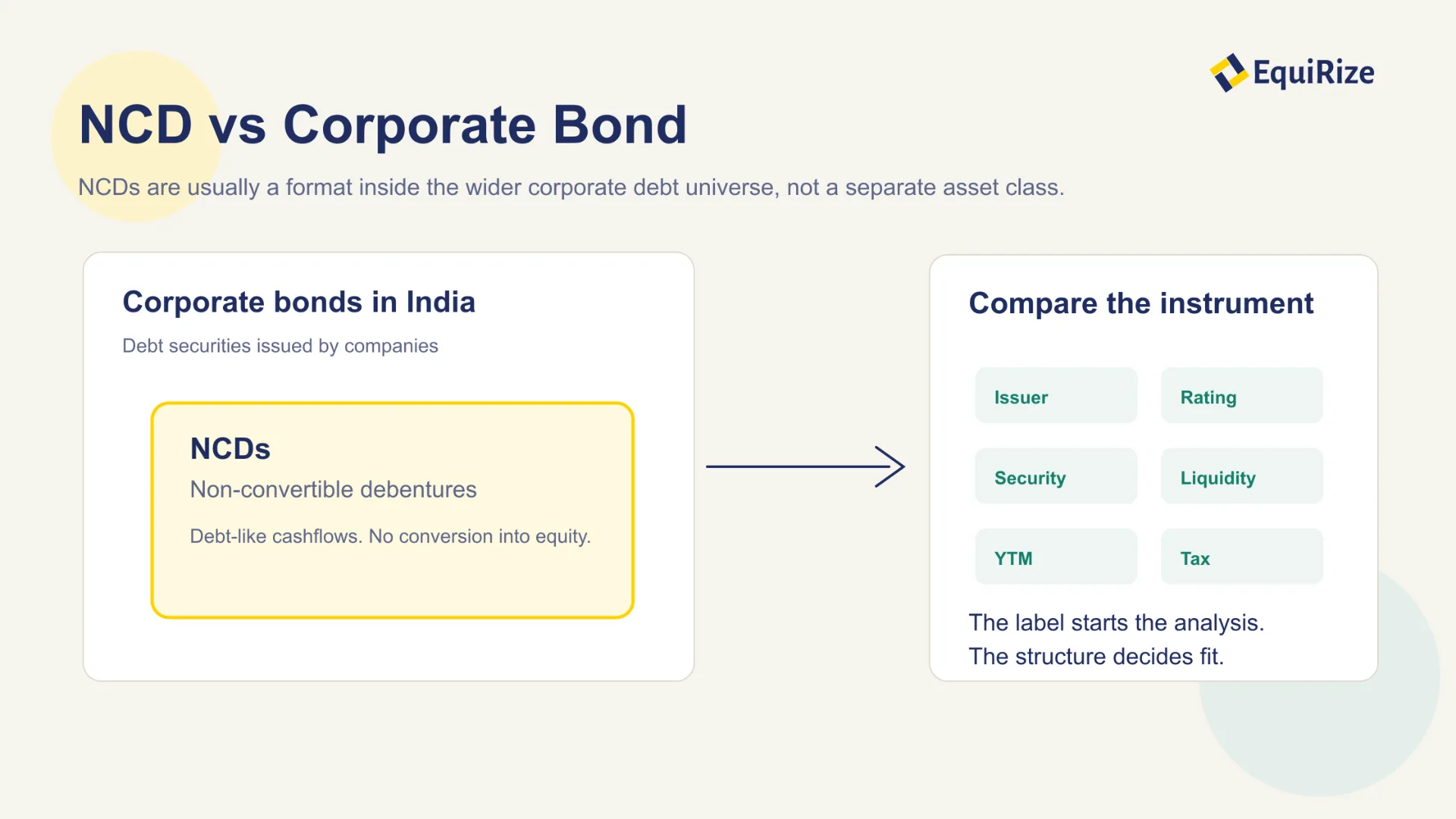

A corporate bond is a debt security issued by a company, while an NCD is a non-convertible debenture issued by a company or eligible institution. In common Indian usage, many listed NCDs sit inside the wider corporate bond universe. The issuer borrows money, promises coupon payments where applicable, and repays principal on the maturity date, subject to issuer performance.

The word "non-convertible" means the debenture does not convert into equity shares. That matters because the investor's economics are debt-like, not ownership-like. You are assessing the issuer's ability to service debt, not betting on future share conversion.

Think of it like asking whether a Mumbai local first-class pass is different from rail travel. It is a specific format within the broader category. NCD vs corporate bond works the same way in many cases.

Why this comparison is often a category error

The NCD vs corporate bond comparison becomes misleading when it assumes the label alone determines risk. A AAA-rated secured NCD issued by a large housing finance company and an unsecured lower-rated bond issued by a stressed issuer should not be compared just because both are debt securities.

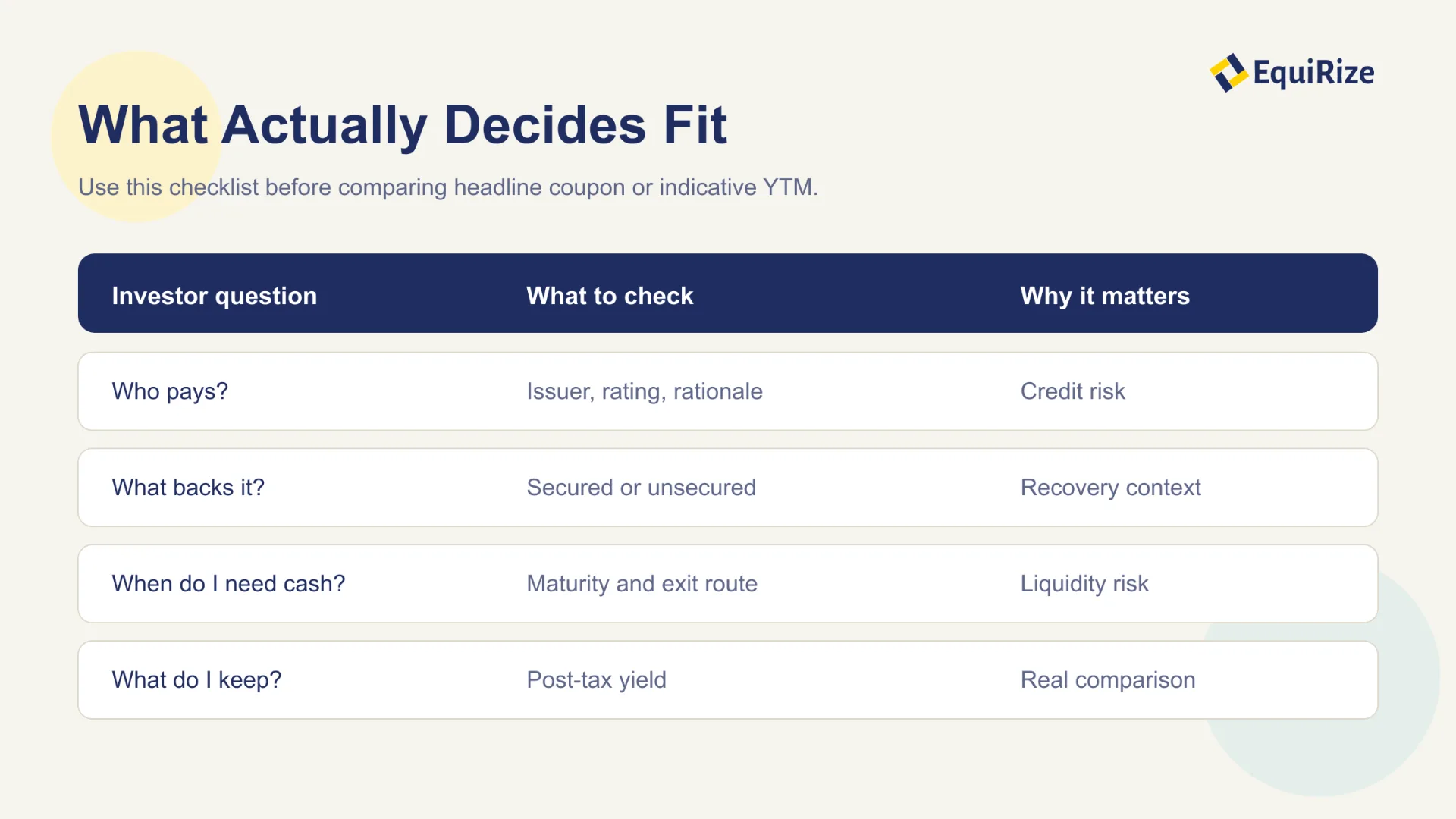

Investors should ask sharper questions. Who is the issuer? What is the credit rating and agency? Is the instrument secured or unsecured? Is it listed? What is the coupon rate, yield to maturity, maturity date, and available liquidity?

Once those questions are asked, the NCD vs corporate bond decision becomes a proper fixed-income comparison. A cleaner NCD vs corporate bond review starts with risk and cashflows, then moves to price. The label tells you what family the instrument belongs to; structure, issuer quality, documentation, and market price tell you whether it fits your portfolio.

NCD vs Corporate Bond in Corporate Bonds in India

Corporate bonds in India reach investors through public issues, private placements, and secondary-market transactions. The path through which you access the instrument can affect minimum investment size, available information, settlement, and exit expectations.

Public NCD issues, private placements, and secondary-market bonds

A public NCD issue is open for subscription during an issue window, much like an IPO process, though the instrument is debt rather than equity. Investors apply during the offer period, review the offer document, and receive allotment if the issue terms are met. Public issues usually make the NCD label visible because that is how the offer is marketed.

Private placements are different. Companies often raise debt from institutional or eligible investors, and those securities may later be available in the secondary market if listed. On a SEBI-registered Online Bond Platform Provider (OBPP), investors may see listed corporate bonds that include NCDs, municipal debt securities, securitised debt instruments, government securities, or other permitted listed debt products.

This is why NCD vs corporate bond should include access route. The NCD vs corporate bond route also affects settlement expectations and available documentation. A new issue and a secondary-market bond can have different prices, accrued interest, yields, and available quantities.

How coupon rate, face value, and maturity date shape the comparison

Coupon rate is the contractual interest rate on the face value. Yield to maturity, or YTM, is the indicative annualised pre-tax yield based on the price you pay, coupons expected, face value repaid, and time left until maturity. Two instruments with the same coupon can show different YTMs because one trades at a discount and another at a premium.

For example, assume a ₹1,00,000 face value NCD has an 8.5% annual coupon and three years to maturity. If it trades near ₹1,00,000, the yield may sit close to the coupon. If it trades at ₹97,000, the discount can raise the indicative YTM. If it trades at ₹1,03,000, the premium can lower the YTM.

The NCD vs corporate bond choice should therefore compare cashflow dates, purchase price, accrued interest, and maturity, not coupon alone. In any NCD vs corporate bond comparison, YTM is useful only when read with tenure and credit context.

Secured NCDs Show Why Structure Matters More than the Label

Secured NCDs attract attention because they sound stronger than unsecured instruments. Security matters, but it is only one layer of protection; investors still need to understand asset cover, enforcement, rating movement, and issuer cashflows.

Bond credit ratings are the first filter, not the final answer

Bond credit ratings condense an agency's view of the issuer's capacity to meet debt obligations. A higher rating typically signals lower assessed credit risk than a lower rating, but ratings are opinions, not repayment promises. They can change after the investment is made.

A serious investor reads the rating rationale, not only the symbol. The rationale often discusses leverage, profitability, asset quality, liquidity profile, sector pressures, security cover, and rating sensitivities. Those paragraphs can be more useful than the one-line rating badge on a product card.

In the NCD vs corporate bond decision, a lower-rated NCD may offer a higher indicative yield because the market is pricing greater credit risk, longer tenure, weaker liquidity, or sector uncertainty. A good NCD vs corporate bond screen therefore asks whether the extra yield compensates you for risks you understand.

Secured vs unsecured NCD which is better for capital protection?

A secured NCD is backed by identified assets or security cover. An unsecured NCD does not have that specific asset backing, so investors rely more directly on the issuer's overall ability to pay. This distinction matters if the issuer faces financial stress.

Still, "secured" should not be read as automatic capital protection. The quality of collateral, ranking of claims, debenture trustee role, enforcement process, and recovery timeline all matter. In real distress, asset recovery can take time and may not fully cover investor claims.

For a ₹25 lakh allocation, a sophisticated investor might prefer a slightly lower indicative yield from a stronger issuer over a higher-yield secured instrument with weaker financials. That is not conservatism for its own sake. It is recognising that fixed income has limited upside, so avoiding uncompensated downside is central to portfolio construction.

Listed Debt Securities: Liquidity, Taxation, and Exit Routes

Listed debt securities give investors a regulated market framework and demat holding, but listing is not the same as instant exit. Liquidity depends on demand, issue size, issuer profile, tenure, and the bid-ask spread available when you want to sell.

Listed NCD vs unlisted NCD liquidity

Listed NCD vs unlisted NCD liquidity is one of the most practical differences for individuals. A listed NCD can be sold on an exchange or through permitted market mechanisms, subject to available buyers and price. An unlisted NCD may be harder to exit and can require more negotiation, documentation, or eligible counterparty access.

Even within listed debt, liquidity is uneven. A widely held AAA-rated instrument from a frequent issuer may trade more often than a small issue from a lesser-known company. If you may need cash within 12 months, do not assume a five-year listed NCD can be sold at a neat calculator price.

The NCD vs corporate bond decision should start with the intended holding period. For NCD vs corporate bond decisions where cash needs are known, matching maturity is usually cleaner than depending on a secondary-market exit.

Tax on NCD and corporate bond interest

Tax on NCD and corporate bond interest is usually straightforward at the first layer: interest income is generally taxed as per the investor's applicable slab. For someone in the 30% slab, an 8.5% coupon does not translate into 8.5% post-tax income. The post-tax number can be materially lower.

Capital gains may arise if you sell before maturity at a price different from your purchase cost. The Income Tax Department's capital-gains guidance states that long-term capital gains are generally taxed at 12.5% without indexation, while short-term capital gains are generally taxed at applicable rates, subject to asset-specific rules and exceptions. Tax treatment depends on individual facts, residency, holding period, and changes in law.

For NRI investors, tax residency, withholding, repatriation, and foreign reporting rules may also matter. In an NCD vs corporate bond shortlist, taxes can change the ranking after headline yield is adjusted. A qualified tax advisor should review the specific transaction before large allocations.

Real-world Scenarios: How Fixed Income Investments India Decisions Use This Comparison

Fixed income investments India decisions are rarely made in abstract. The right choice depends on whether the investor wants scheduled income, maturity matching, diversification, or a temporary parking option for capital.

Rohan, 39, wants predictable coupon dates without equity volatility

Rohan earns ₹32 lakh CTC in Bengaluru and has accumulated ₹18 lakh outside his emergency fund. He wants part of the money away from equity volatility for three years, because he may use it for a home down payment in 2029.

For him, NCD vs corporate bond is not a hunt for the highest visible yield. He shortlists listed debt securities maturing in 24 to 40 months, compares indicative YTM after tax, and avoids instruments where the exit depends on thin secondary-market liquidity. A bond maturing close to his target date is more useful than a seven-year NCD with a slightly higher coupon.

Meera, 52, is an NRI building rupee income for Indian expenses

Meera lives in Dubai and sends money to support her parents in Kochi. She wants ₹40,000 to ₹50,000 of periodic rupee cashflow every quarter without moving more capital into Indian equities.

For Meera, the NCD vs corporate bond question starts with eligibility, account structure, taxation, and repatriation. She reviews whether the instrument is available to NRIs, whether the coupons align with her parents' expense cycle, and whether the issuer concentration is acceptable. A ladder of three maturities may suit her better than one large exposure to a single issuer.

Arvind, 67, wants to stagger maturities after retirement

Arvind retired in Pune with ₹1.2 crore across FDs, debt funds, and listed bonds. He is not trying to maximise yield; he wants fewer surprises and clear maturity dates.

For Arvind, NCD vs corporate bond is a cashflow planning exercise. He may allocate ₹10 lakh each across instruments maturing in 2027, 2028, and 2029, while keeping enough bank liquidity for medical expenses. He reads the offer document, checks the debenture trustee, and avoids taking a large position just because one NCD offers 50 bps more than a comparable bond.

Conclusion

The key takeaway is simple: NCD vs corporate bond is not a choice between two unrelated assets; it is a disciplined way to compare issuer risk, structure, price, liquidity, tax, and maturity fit within corporate debt. Before investing, shortlist only instruments that match your time horizon, then compare credit rating, security, YTM, offer document disclosures, and post-tax outcome.

On EquiRize, you can compare curated listed bond opportunities and review key fixed-income details before taking the next step.