Monthly Income from Bonds: How to Build a Cash Flow Plan

Monthly Income from Bonds: How to Build a Cash Flow Plan

Monthly income from bonds is possible when the bonds you hold pay coupons every month, or when you build a ladder that staggers coupon dates and maturities across the year.

But a monthly income plan should not start with the highest displayed yield. It should start with a cash-flow need.

Ask three questions first: how much income do you need after tax, how stable does it need to be, and how much principal can you keep invested until maturity? Bonds can support regular income planning because many listed bonds have defined coupon dates and maturity dates. That visibility is useful for retirees, families with planned expenses, and investors building a fixed-income sleeve.

The trade-off is risk. Coupon schedules are not the same as certainty. Issuers can delay or default. Secondary-market liquidity can be thin. Tax can reduce the amount that reaches your bank account.

Use bonds as a planned cash-flow tool, not as a substitute for an emergency fund.

Monthly Income Bonds: How Coupon Cash Flows Work

Monthly income bonds are debt securities that pay interest at a defined frequency. Some pay monthly. Others pay quarterly, semi-annually, annually, or at maturity. The income experience depends on the actual coupon schedule written in the offer document, not only on the headline yield shown on a platform.

How monthly interest bonds work in India

When you buy a listed bond or NCD, you lend money to the issuer. In return, the issuer is expected to pay coupon interest as per the terms of the security and repay principal on the maturity date.

A monthly interest bond pays coupon every month, usually to the registered holder on the relevant record date. For an investor, this can create visible cash flow. For example, a bond with a face value of Rs 1,00,000 and an annual coupon of 10.20% may pay around Rs 850 per month before tax, subject to terms and payment schedule.

Monthly payout corporate bonds India: what to verify

Before treating a bond as a monthly income instrument, verify the exact coupon frequency, coupon date, record date, maturity date, secured or unsecured status, credit rating, and payout history where available.

Also check whether the displayed yield is yield to maturity, yield to call, current yield, or another metric. A bond may show an attractive indicative yield because of its price, tenure, credit profile, or liquidity conditions. Yield should be read with the term sheet.

Coupon frequency vs yield to maturity

Coupon frequency tells you when interest is expected to be paid. Yield to maturity estimates the annualised return if you buy at the current price, hold until maturity, and the issuer pays as scheduled.

Both matter. A high YTM with annual payout may not solve a monthly expense need. A monthly coupon bond with a lower post-tax yield may fit cash-flow timing better. Match the structure to the job.

| Term | What it tells you | Why it matters for monthly payouts |

| Coupon rate | Stated annual interest on face value | Helps estimate expected interest payouts |

| Coupon frequency | Monthly, quarterly, annual, or other schedule | Determines when cash may arrive |

| Yield to maturity | Indicative annualised return if held to maturity | Helps compare bonds bought at different prices |

| Maturity date | Scheduled principal repayment date | Helps plan reinvestment and liquidity |

Bonds for Monthly Income in India: Who Should Consider Them?

Bonds for monthly income in India may fit investors who want defined payout dates and can accept issuer-level risk. They are not only for retirees. They can also serve people who want fixed-income allocation for planned obligations, provided they do not depend on one issuer or one payout date.

Monthly income bonds for retirees

Retirees often look for regular cash flow without selling growth assets every month. Monthly income bonds can help supplement pensions, annuities, rental income, or fixed deposits.

The key word is supplement. Retirement cash flow should usually include a bank buffer, liquid assets, insurance planning, and diversification across instruments. A bond income plan should not depend entirely on lower-rated issuers or one maturity year.

Planned expenses that may fit a bond cash flow plan

Bond cash flows may fit expenses that are visible in advance: school fees, home maintenance, senior-care costs, loan EMIs, charitable commitments, or a monthly household top-up.

For these use cases, map the expense date first. Then choose securities with coupon dates or maturities that support that calendar. A cash-flow plan is stronger when it is built around real dates instead of abstract return targets.

When monthly income bonds may not suit you

Monthly income bonds may not suit investors who need instant liquidity, cannot review issuer risk, or may need to sell at short notice.

They may also be unsuitable if the investor is chasing yield without understanding rating, security cover, subordination, call options, taxation, or secondary-market depth. If the goal is emergency access, a savings account, sweep FD, or liquid fund may be more appropriate.

Bond Cash Flow Plan: Build Around Real Expenses

A bond cash flow plan starts with the amount you need each month and works backward. This is different from scanning a list of yields and choosing the largest number. Good planning connects income need, tax slab, investment amount, issuer mix, and liquidity buffer.

How much to invest in bonds for monthly income

The rough formula is simple:

Required investment = Annual income needed / Post-tax annual yield

Suppose you need Rs 25,000 per month. That is Rs 3,00,000 per year. If your post-tax yield assumption is 7.2%, the rough required capital is Rs 41.7 lakh.

If the post-tax yield assumption is 6.0%, the required capital rises to Rs 50 lakh. If it is 8.0%, it falls to Rs 37.5 lakh. These are illustrations only. Actual outcomes depend on available bonds, price, taxes, credit events, reinvestment, fees, and payment timing.

Monthly income from bonds example

Here is an illustrative, hypothetical cash-flow estimate for an investor targeting Rs 25,000 per month before tax.

| Portfolio sleeve | Illustrative capital | Indicative pre-tax yield | Expected annual income | Intended role |

| Higher-rated shorter-tenure bonds | Rs 12,00,000 | 8.0% | Rs 1,20,000 | Base stability |

| Monthly coupon corporate bonds | Rs 12,00,000 | 9.5% | Rs 1,14,000 | Monthly cash flow |

| Quarterly coupon bonds | Rs 8,00,000 | 9.0% | Rs 72,000 | Staggered income |

| Bank/liquid buffer | Rs 5,00,000 | Varies | Not primary income | Payment gap cushion |

This example produces about Rs 3,06,000 of expected annual pre-tax bond income, excluding buffer income. That is close to Rs 25,500 per month before tax if cash flows are averaged. Actual monthly receipts may still vary because coupon dates are uneven.

Why post-tax income matters more than coupon income

Bond interest is generally taxed as income at the investor's applicable slab rate. That means a 10% coupon does not usually mean 10% in hand.

If you are in a higher tax slab, your post-tax monthly income can be materially lower. Always calculate income after tax before deciding how much capital to allocate. For many investors, the post-tax cash-flow table is more useful than the headline yield table.

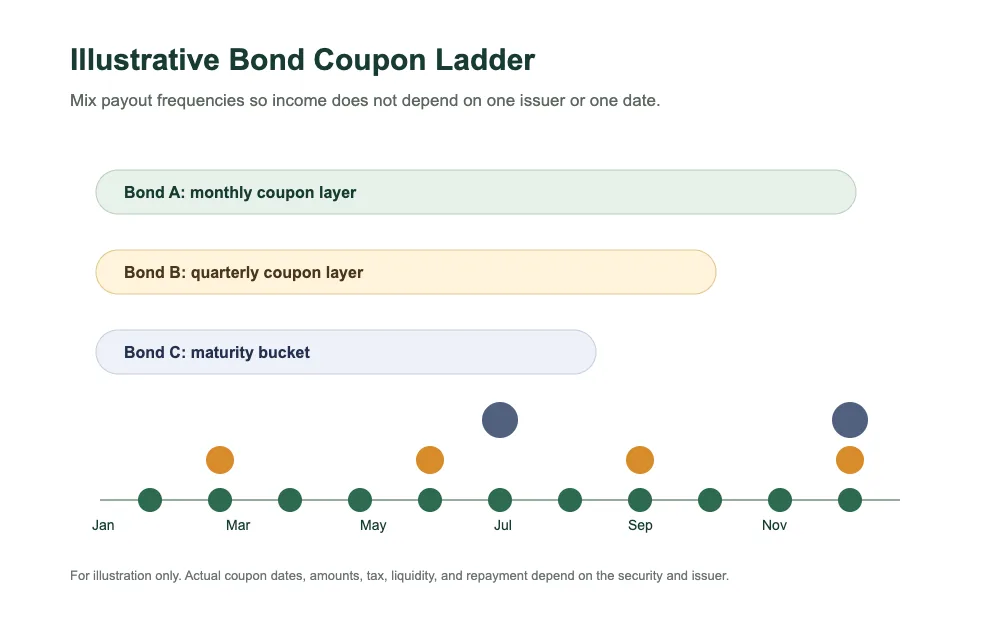

Bond Ladder for Monthly Income: Worked Example

A bond ladder for monthly income spreads investment across coupon dates, issuers, and maturities. It can include monthly coupon bonds, quarterly coupon bonds, and maturity buckets. The goal is not perfect income symmetry. The goal is to reduce dependence on one instrument while making cash flows easier to plan.

Bond ladder for regular income

A ladder can be built in three layers.

The first layer is monthly coupon bonds for recurring inflow. The second layer is quarterly or semi-annual coupon bonds staggered across different months. The third layer is maturity proceeds that can be used for reinvestment or large expenses.

For example, instead of putting Rs 30 lakh into one monthly payout bond, an investor may split across six to ten securities, subject to available lot sizes and suitability. This reduces single-issuer concentration. It also helps if one payout date is missed or one security becomes illiquid.

The ladder should be reviewed every few months. Check whether ratings changed, whether maturities are approaching, and whether reinvestment options still match your income need.

Quarterly coupon bonds monthly income plan

Quarterly coupon bonds can still support a monthly plan if you stagger them carefully.

| Bond | Coupon frequency | Expected payout months | Role in monthly plan |

| Bond A | Monthly | Every month | Base income |

| Bond B | Quarterly | Jan, Apr, Jul, Oct | Quarter-start support |

| Bond C | Quarterly | Feb, May, Aug, Nov | Quarter-middle support |

| Bond D | Quarterly | Mar, Jun, Sep, Dec | Quarter-end support |

This kind of structure can smooth cash flow without forcing the entire portfolio into monthly payout bonds. It may also widen the investible universe, because not every suitable bond pays monthly.

Reinvestment and maturity planning

Monthly income planning does not end after purchase. Bonds mature. Coupons may need to be reinvested. New bonds may be available at lower or higher yields than earlier assumptions.

This is reinvestment risk. If yields fall when your bond matures, the same capital may generate lower income. If yields rise, reinvestment may look better, but existing bonds could show lower secondary-market prices.

Keep a maturity calendar. Note principal repayment dates, coupon dates, and months where income may be lower. A simple spreadsheet can prevent surprises. The portfolio should have enough flexibility to handle delayed payments, tax outflows, and periods when suitable new bonds are unavailable.

Corporate Bonds Monthly Income: Risk Checks Before You Invest

Corporate bonds monthly income can look orderly on a spreadsheet. Real life is messier. Issuer quality, liquidity, structure, and market conditions can change after purchase. The higher the dependency on bond income, the more disciplined the risk review needs to be.

Credit rating, issuer risk, and offer documents

Credit rating is a useful starting point, not a final answer. Read the rating rationale, not just the rating symbol. Look for leverage, profitability, asset quality, repayment track record, sector exposure, security cover, and any recent rating action.

Then read the offer document or information memorandum. Check whether the bond is secured, what assets support it, whether there are covenants, and whether there are call or put options. If the structure is hard to understand, do not force the investment.

Liquidity risk if you sell before maturity

Listed bonds can be sold before maturity, but liquidity varies. Some securities may have regular secondary-market activity. Others may have limited buyers.

If you sell early, the sale price can be lower than your purchase price. Price can move because of interest rates, credit spreads, issuer news, and demand. For monthly income planning, assume you may need to hold bonds until maturity unless you have checked liquidity carefully.

Risks of monthly income bonds

The main risks are delay in payment, default in payment, downgrade risk, liquidity risk, reinvestment risk, interest-rate risk, and concentration risk.

Monthly payout does not reduce issuer risk. A lower-rated monthly coupon bond can still carry more risk than a higher-rated annual coupon bond. A diversified ladder can reduce concentration, but it cannot eliminate credit risk.

Use indicative returns and target yield language. Avoid treating any displayed yield as assured. The offer document is the source of truth for the security's terms.

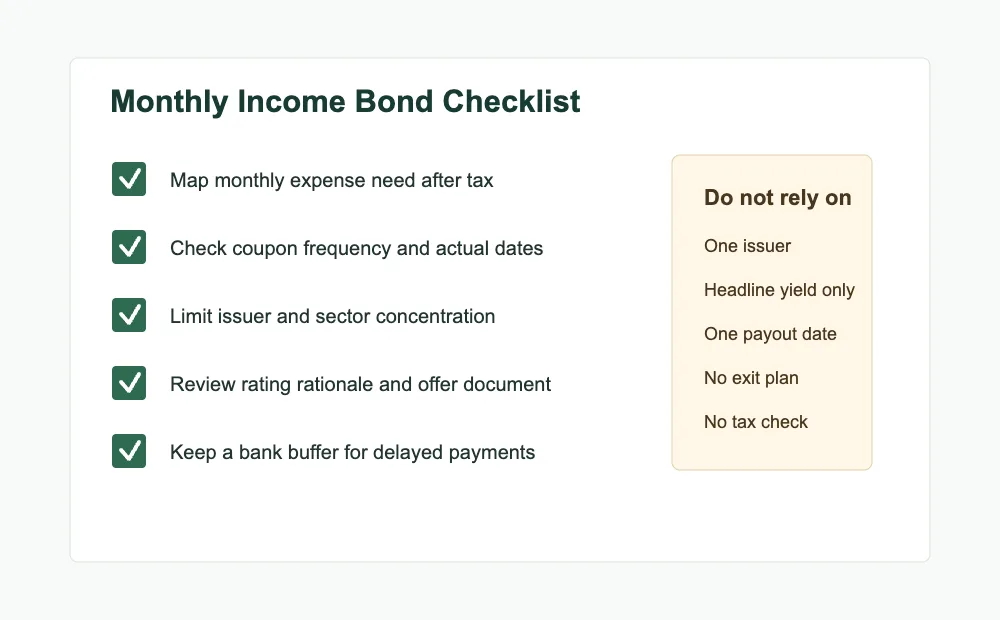

Monthly Income Bonds Checklist Before Investing

Before investing, move from "Does this pay monthly?" to "Does this fit my cash-flow plan after risk and tax?" The checklist below is designed for quick comparison. It works whether you are reviewing one bond or building a ladder.

Checklist for comparing monthly interest bonds

Use this checklist before shortlisting monthly interest bonds:

| Check | Question to Ask | Why it Matters |

| Cash-flow | What monthly amount do I need after tax? | Prevents overreliance on headline yield |

| Coupon schedule | Is payout monthly, quarterly, annual, or cumulative? | Aligns income with expenses |

| Issuer exposure | How much of my portfolio depends on one issuer? | Reduces concentration risk |

| Credit review | Have I read rating rationale and offer document? | Goes beyond rating symbol |

| Liquidity | Can I hold to maturity if secondary buyers are limited? | Avoids forced selling |

| Tax | What is my post-tax income? | Shows actual cash available |

| Buffer | Do I have 3-6 months of expenses outside bonds? | Handles payment gaps |

Summary table: what to check before investing

If a bond passes the income test but fails the risk test, pause. If it passes the yield test but fails the liquidity test, pause. If it looks attractive only before tax, recalculate. Monthly income planning is strongest when cash-flow timing, issuer quality, and exit assumptions all make sense together.

Monthly Income from Bonds: Final Take

Monthly income from bonds is a planning exercise first and a product choice second.

Start with the income you need after tax. Build a coupon and maturity calendar. Use monthly payout bonds where they fit, but do not ignore quarterly coupon bonds if they improve diversification. Check issuer risk, rating rationale, offer documents, liquidity, and concentration before investing.

EquiRize is a SEBI-registered OBPP and stock broker in the debt segment of BSE and NSE. Investors can use the platform to compare listed bonds, review key terms, and evaluate whether a bond fits their cash-flow plan.