Investing in Bonds in India With ₹10,000: Starter Guide

For many Indian professionals, the first fixed-income decision is automatic: renew the fixed deposit, compare two bank rates, and move on. Bonds used to feel like a product for institutions or private-bank portfolios. That is changing. With smaller ticket sizes becoming more visible in listed debt, investing in bonds in India can now start with ₹10,000 in eligible issues, subject to the offer terms and allotment. This guide explains how access works, what a SEBI-registered platform does, how bonds compare with FDs, and what a serious investor should check before subscribing.

Can I Start Investing in Bonds in India with ₹10,000?

Yes, but the phrase needs careful handling. ₹10,000 is an entry point only where the issue structure, face value, lot size, and platform inventory allow it.

₹10,000 is an access point, not a universal minimum

A listed corporate bond is issued under defined terms. Some issues may be accessible at smaller denominations, while others may require a higher subscription amount. Before assuming entry is possible, check the minimum subscription, face value, coupon schedule, maturity date, and offer document.

For a salaried professional or NRI investor testing direct fixed income, ₹10,000 can be a learning-sized allocation. It should not be treated as a shortcut around due diligence.

Why smaller ticket sizes matter for fixed-income investors

The real shift is access. Earlier, direct bond opportunities were often routed through institutional desks, brokers, or relationship managers. Today, a SEBI-registered Online Bond Platform Provider (OBPP) can facilitate access to listed debt securities through a more transparent digital process.

That access is useful because it lets an investor learn with proportion, not because it makes the decision casual. The same questions still apply: who issued the bond, what are the terms, and what can go wrong?

How to Invest in Corporate Bonds in India

The mechanics are closer to equity-market infrastructure than many first-time bond investors expect. The journey is digital, but the decision still requires issuer-level review.

Documents and accounts you usually need

To subscribe to listed corporate bonds, an investor generally needs PAN, completed KYC, a demat account, and a bank account that can be verified for settlement. The bond, if allotted, is held in the investor's own demat account.

This matters because the investor is not placing money with the platform. The investor is subscribing to a listed debt security issued by an issuer, under the terms of that security.

What happens on a SEBI-registered bond platform

A SEBI-registered bond platform helps the investor review available listed corporate bonds, read issue details, check rating and tenure, access documents, complete onboarding, and subscribe through the platform flow.

Equirize is a SEBI-registered Online Bond Platform Provider. It facilitates access to listed corporate bonds and other listed debt securities. It is not the issuer and does not provide investment advice.

Bonds vs Fixed Deposits: What Changes for the Investor?

The bonds vs fixed deposits comparison is useful because both sit in the fixed-income conversation. But they solve different jobs and carry different risk structures.

Bank FDs are deposits; bonds are securities

A bank FD is a deposit with a bank. Bank fixed deposits up to ₹5 lakh per depositor per bank are insured by DICGC. Amounts above this are subject to bank credit risk. Premature withdrawal terms vary by issuer.

A listed corporate bond is a market security issued by a company or eligible institution. It may pay a defined coupon, but the investor is exposed to the issuer's ability to meet scheduled obligations.

Compare tenure, tax, credit risk, and liquidity

A bond may show an indicative pre-tax yield that differs from an FD rate, but that number is not enough. The investor should compare tenure, tax treatment, issuer credit quality, liquidity, and exit options.

The better question is not whether bonds are superior to FDs. It is whether a specific bond fits the role the investor wants fixed income to play.

How a SEBI-registered bond platform works

A SEBI-registered bond platform operates within the OBPP framework. This framework brings digital bond access into a defined regulatory perimeter, without removing issuer-level risk.

What the platform should show you

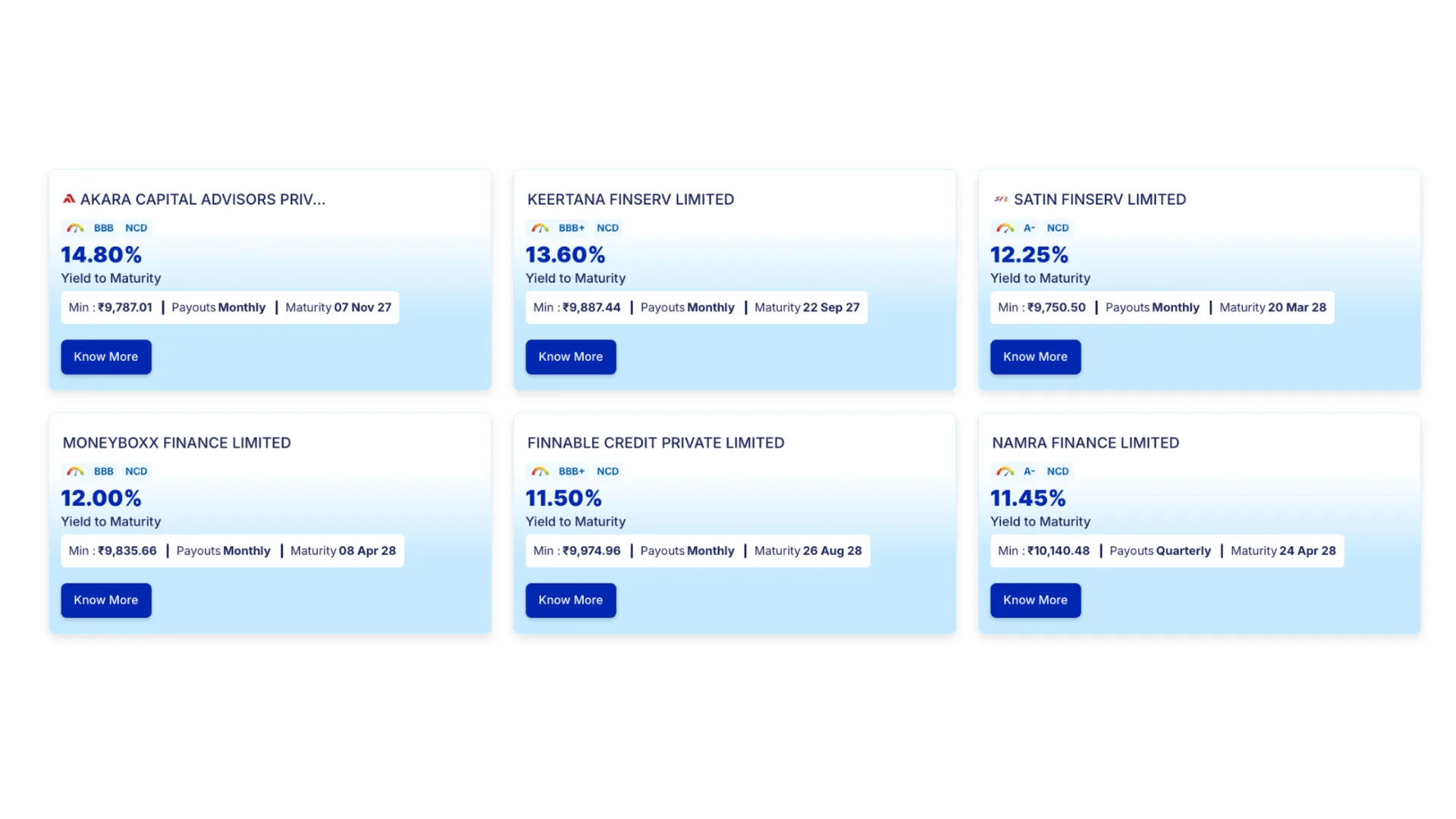

In a good bond-access flow, the investor should be able to see the issuer name, instrument type, coupon rate, maturity date, credit rating and agency, minimum subscription amount, risk factors, and offer document. These are not decorative details. They are the facts that allow comparison.

What SEBI registration does and does not mean

"Registered with SEBI as an OBPP" does not mean SEBI approves or endorses any specific security listed on the platform. The registration defines the platform's operating perimeter. The bond's risk still belongs to the issuer, the instrument terms, and the investor's decision.

Equirize's role is access and facilitation. It can help organise discovery, onboarding, and subscription. It does not remove credit risk, interest-rate risk, liquidity risk, or concentration risk.

What Should I Check Before Investing in Bonds in India?

Before subscribing, a financially literate investor should run a short but disciplined checklist. The goal is not to eliminate risk; it is to understand what risk is being taken.

Check issuer, rating, and offer document

Start with the issuer. Read the legal name, business profile, rating rationale, and offer document. A familiar brand name is not a substitute for credit review.

Then check the credit rating and agency. Ratings from agencies such as CRISIL, ICRA, CARE, or India Ratings help investors understand relative credit opinion, but ratings can change. They are inputs, not guarantees.

Check YTM, maturity, liquidity, and concentration

Know the coupon rate, coupon frequency, maturity date, redemption terms, and whether the quoted yield is pre-tax. Yield to maturity assumes the bond is held until maturity and all scheduled payments are made. For a deeper explainer, refer to Equirize's guide on how yield to maturity works once the final slug is live.

Also check liquidity and concentration. Listing does not mean instantly liquid at the price you want. Secondary-market exits depend on demand, bid-ask spreads, and prevailing rates.

Bond Investing for NRIs and Salaried Professionals

For salaried professionals and NRIs, the first bond allocation should fit a larger financial plan. The same ₹10,000 investment can mean very different things depending on income, residency, tax status, and liquidity needs.

How salaried professionals may use listed bonds

For a salaried professional, direct bonds may play a role in the non-equity part of a portfolio: defined maturity dates, scheduled coupon cash flows, and diversification away from equity-market volatility. The role is usually complementary, not all-or-nothing.

What should NRI investors verify first?

For NRIs, eligibility depends on the specific security, account type, KYC status, bank account structure, and applicable FEMA and tax rules. An NRI investor should check whether the bond is available for NRI subscription and whether the platform supports the required onboarding route.

Tax deserves early attention. Coupon income and capital gains may be treated differently depending on holding period, investor status, and current law.

How to Build a First ₹10,000 Bond Allocation

A first allocation should be designed to teach the investor how the product behaves. It should not be built around the largest visible yield alone.

Start with the job of the money

Is the money meant for a one-year parking need, a three-year goal, or the first rung of a longer fixed-income portfolio? The answer changes the maturity you should consider.

Then compare eligible issues on the same basis. Do not compare a two-year AA rated bond with a five-year lower-rated bond only by headline yield. Compare rating, maturity, coupon frequency, issuer profile, liquidity, and tax impact.

Use maturity staggering as the portfolio grows

If the investor intends to build over time, maturity staggering can reduce reinvestment concentration. Equirize's guide to bond laddering for cashflow planning explains that approach in more detail.

A first transaction should create clarity. Over time, the portfolio should be shaped by goals, cash-flow needs, issuer diversification, and risk capacity.

Common Mistakes to Avoid when investing in bonds in India

Many first-time bond investors do the hard part correctly: they look beyond equity and start studying fixed income. The avoidable mistakes usually happen after that.

Looking only at coupon or indicative yield

Coupon is not the same as yield to maturity. Indicative pre-tax YTM depends on price, coupon, maturity, and hold-to-maturity assumptions. It should always be read with issuer risk, tax treatment, and liquidity in mind.

Ignoring exit and tax before subscribing

An investor who may need money early should not treat a listed bond like a bank FD with predictable premature withdrawal terms. Secondary-market exits depend on available buyers and market price.

Tax treatment can also change the post-tax outcome meaningfully, especially for HNIs and NRIs. The sensible sequence is simple: understand the instrument first, compare it with alternatives second, and subscribe only after the risk-return trade-off is clear.

Conclusion

Starting with ₹10,000 can make direct bonds easier to study, but the better measure of readiness is not ticket size. It is whether the investor understands the instrument.

Investing in bonds in India with ₹10,000 should be viewed as a more accessible entry point into listed fixed income, not as a shortcut around risk. The right first step is to understand the issuer, rating, maturity, coupon schedule, liquidity, tax impact, and offer document.

For salaried professionals, HNIs, and NRIs, bonds may play a useful role in the non-equity side of a portfolio when selected with care. A SEBI-registered OBPP such as Equirize can help investors explore curated listed bond opportunities within a regulated access framework. This content is for informational purposes only and does not constitute investment advice. Please consult a SEBI-registered advisor before investing.