Form 121 for Investors: TDS-Free Interest in India

Form 121 for Bond Investors: TDS-Free Interest Guide

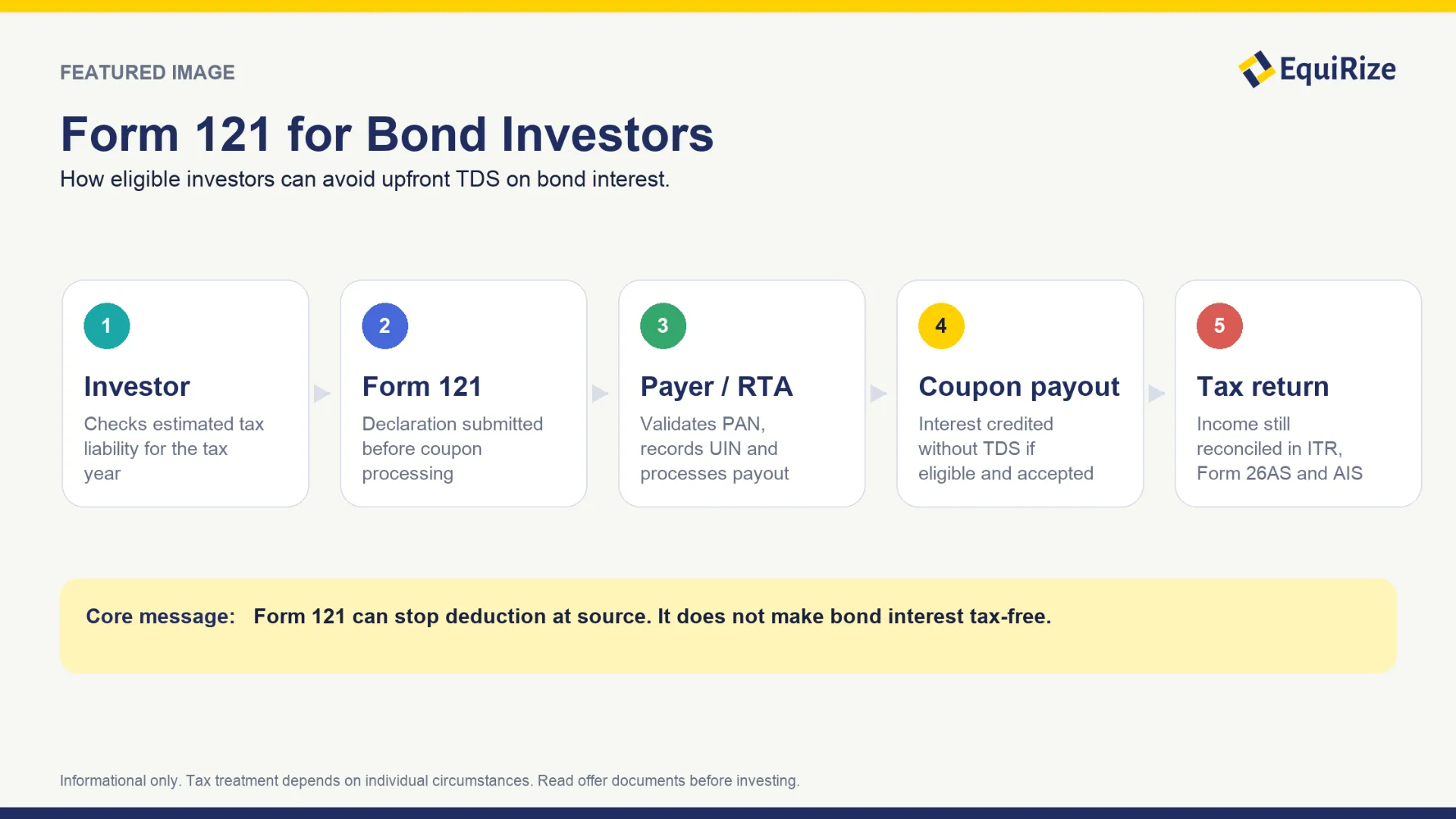

Bond investors like clean cash flows. Coupon date arrives, interest is credited, and the income can be planned around. TDS can interrupt that rhythm. Form 121 for bond investors is the new declaration route for eligible taxpayers who want certain income, including interest on securities, paid without tax deduction at source. It is useful, but only if used correctly. It does not make bond interest tax-free. It simply helps eligible investors avoid unnecessary TDS when their estimated tax liability for the tax year is nil.

Introduction: Form 121 for Bond Investors in Plain English

Form 121 is a self-declaration given to the payer before income is credited or paid. In listed bonds and NCDs, that income is usually coupon interest. If your declaration is valid and accepted, the payer may credit interest without TDS.

The catch is eligibility. You cannot file Form 121 just because you dislike TDS or want higher cash flow. You file it only when your estimated tax liability for the tax year is nil. For many retirees, low-income investors, or investors with deductions and rebates, this can reduce refund paperwork.

What is Form 121 for Bond Investors?

Form 121 is the declaration prescribed under Rule 211 of the Income-tax Rules, 2026 for receipt of specified income without deduction of tax under Section 393(6) of the Income-tax Act, 2025. The Income Tax Department's official Form 121 guidance lists "interest on securities" as one of the covered income categories, which is why bond investors need to understand it.

Form 121 meaning for interest on securities

For bond investors, the relevant phrase is interest on securities. Listed corporate bonds, NCDs, and other debt securities may pay coupon interest. Where TDS would otherwise apply, an eligible investor can use Form 121 to declare nil tax on estimated total income for the tax year.

The payer then has compliance duties too. Rule 211 requires the payer to allot a unique identification number to each Form 121 declaration received and report the declaration in the relevant TDS statement.

TDS-free interest is not tax-free income

This is the most important distinction. TDS-free means tax is not deducted at the time of payment. It does not mean the income is outside taxation.

If your final tax liability is not nil, the income must still be reported in your return and taxed according to your facts. Form 121 is meant to prevent unnecessary deduction for taxpayers whose tax liability is nil. It is not a shortcut for reducing taxable income.

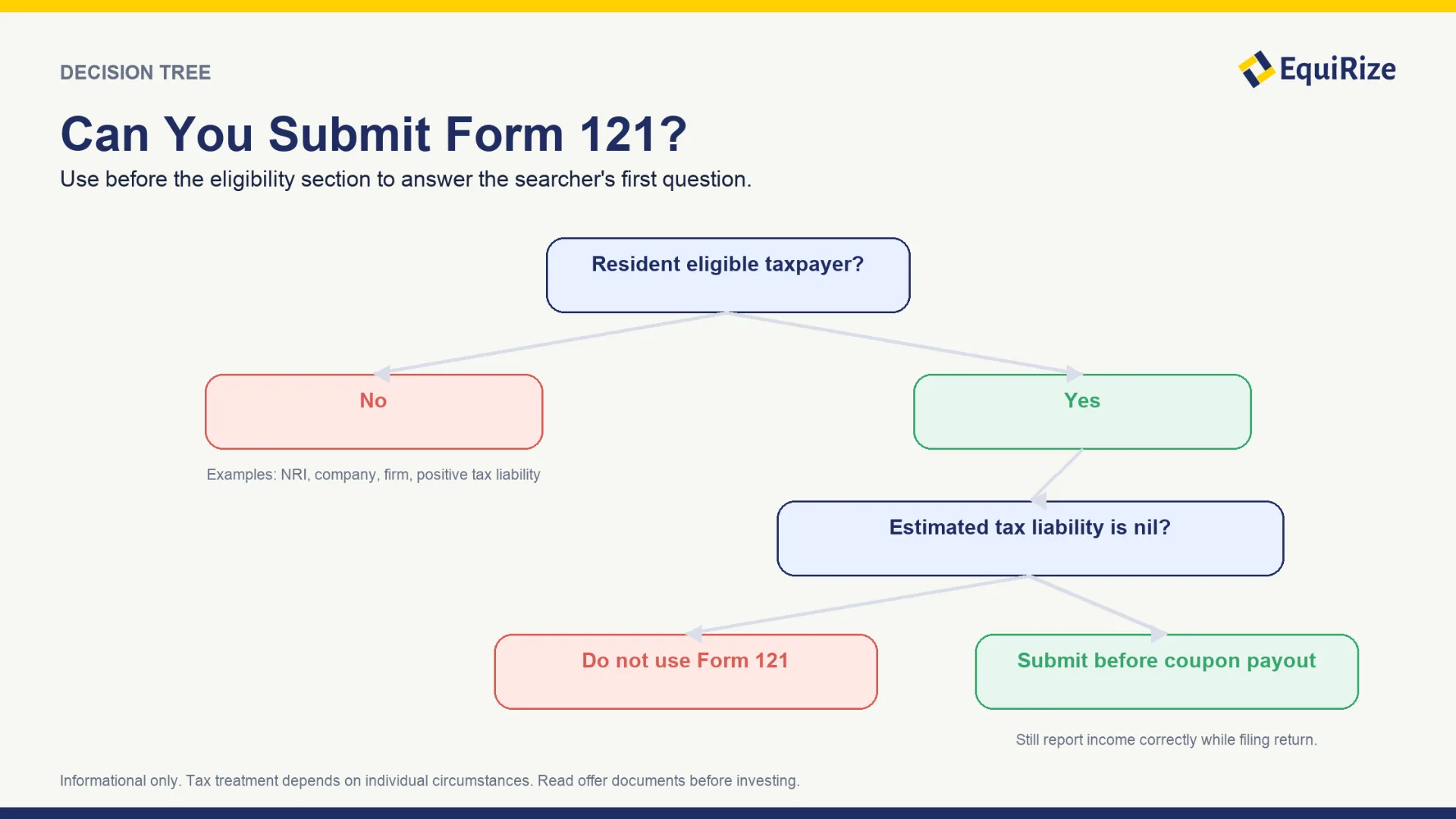

Form 121 Eligibility for Bond Interest TDS

Form 121 eligibility depends on your residential status, taxpayer category, age, estimated total income, and final tax liability. You should test eligibility before every tax year because income, deductions, and rebate positions can change.

Who can submit Form 121 for bond interest

Resident individuals and other eligible resident persons such as HUFs may submit Form 121 if they meet the conditions in the form and rules. For persons below 60 years and other eligible persons, the Income Tax Department FAQ states two key tests: tax liability on estimated total income must be nil, and the aggregate of specified incomes on which TDS applies should not exceed the maximum amount not chargeable to tax.

For bond investors, this means you cannot look only at one coupon. Add salary, pension, business income, FD interest, bond interest, rent, capital gains where applicable, and other expected income.

Form 121 eligibility for senior citizens

The official FAQ states that individuals aged 60 years or more have a relaxed condition: they can submit Form 121 if the tax on estimated total income is nil.

That can be useful for senior citizens who earn coupon income from bonds but remain within a nil-tax outcome after deductions and rebates. Still, the declaration should match the actual estimate for the tax year. If income changes later, speak to a tax advisor.

Is Form 121 applicable to NRIs, companies, and firms?

Form 121 is not a universal no-TDS form. The Income Tax Department's table for covered income repeatedly identifies eligible payees as resident individuals and other resident persons not being a company or a firm for several covered categories, including interest on securities.

NRIs, companies, firms, and LLPs should not assume they can use Form 121 for bond interest. Their TDS rules may differ. If you are an NRI bond investor, check the applicable withholding, treaty, and return-filing position with a qualified tax professional.

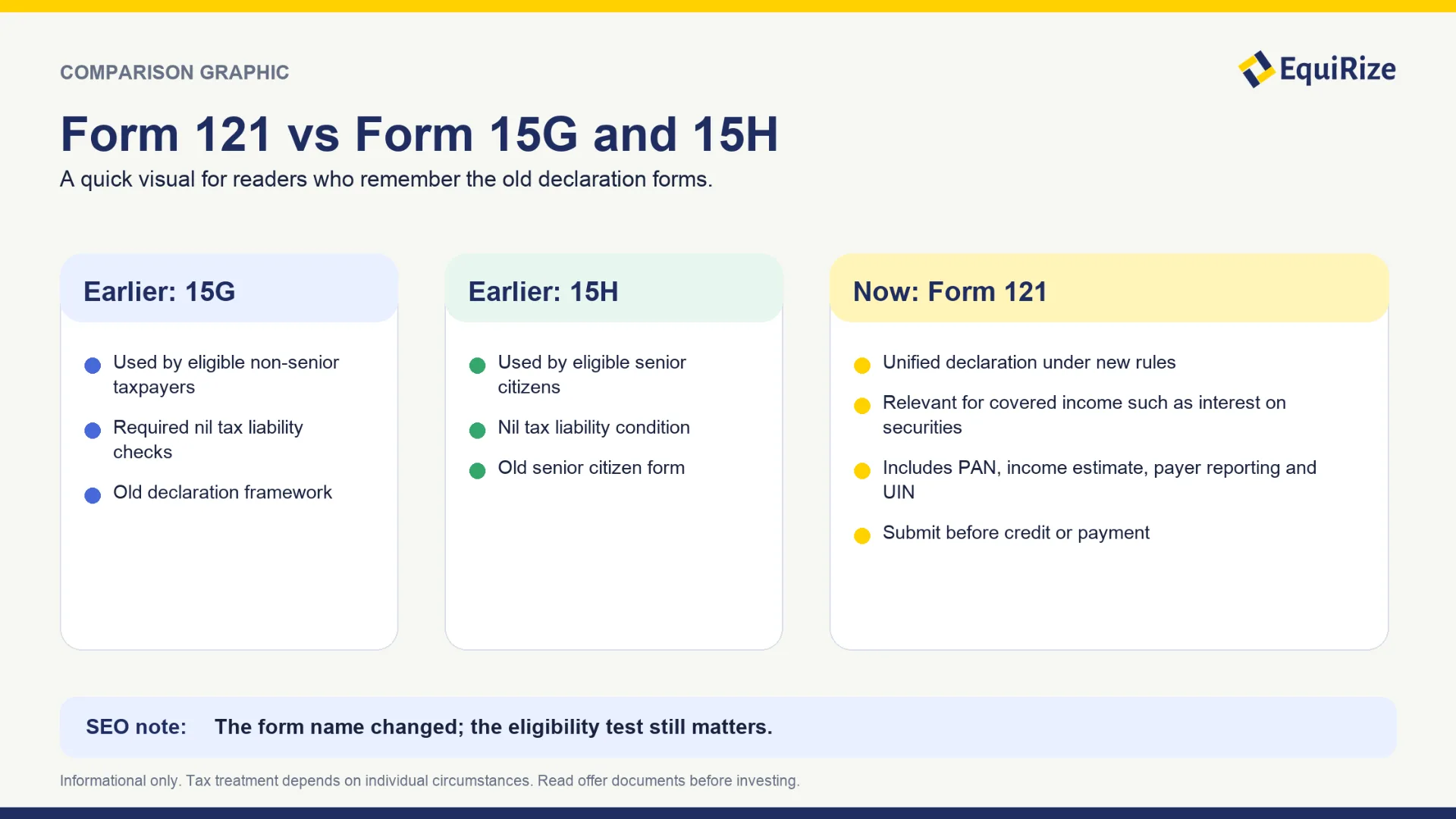

Form 121 Replaces 15G and 15H for Bonds

Form 121 is the successor to the familiar Form 15G and Form 15H framework. The Income Tax Department FAQ says Form 121 was introduced to simplify tax compliance, align with the Income-tax Act, 2025, and merge the earlier forms into one declaration.

Form 121 vs Form 15G and 15H

Earlier, Form 15G was commonly used by eligible individuals below 60 and certain other eligible persons, while Form 15H was used by eligible senior citizens. Form 121 creates one consolidated format.

For investors, the shift is not only the form name. The new format uses "Tax Year" terminology, improved field structure, and electronic compatibility. That matters because bond interest may flow through issuers, registrars, depositories, and reporting systems.

PAN, Part A, Part B, and UIN reporting

Form 121 has two sides. Part A is filled by the declarant, meaning the investor. Part B is for the payer or deductor, who verifies that the declaration has been received and relied on for making payment without deduction.

A valid PAN is mandatory. The payer also has to allot a UIN to each declaration and report it. This reporting layer is why investors should avoid casual or inaccurate declarations. A Form 121 submission creates a compliance record.

How to Submit Form 121 for Bond Interest Payouts

Think about Form 121 before the coupon date, not after the bank credit arrives. Once TDS is deducted, the path usually shifts from prevention to refund claim through the return-filing process.

When to submit Form 121 for bond interest payouts

The Income Tax Department FAQ says Form 121 should ideally be submitted before income is credited or paid, preferably at the start of the tax year. Delayed submission may result in tax deduction and a later refund process.

For bond investors, a useful habit is to check upcoming coupon dates at the start of April, then review tax-year eligibility. If you hold multiple bonds, do this issuer-wise and payout-wise.

Documents required for Form 121

Keep the basics ready:

- Valid and operative PAN

- Name, address, and contact details

- Estimated total income for the tax year

- Details of bond interest or other covered income

- Payer or deductor details, including TAN where required

- Bank account details for interest-bearing instruments

- Age proof if claiming senior citizen status

Do not guess the income figure. Use coupon schedules, FD interest estimates, pension slips, salary estimates, and other expected income to create a reasonable tax-year view.

Where bond investors may need to submit Form 121

Depending on the bond and payout process, Form 121 may need to be submitted to the issuer, registrar and transfer agent, payer, deductor, or through an electronic process. From April 1, 2027, official guidance also notes that declarations may be furnished electronically to a depository in specified cases involving listed securities held with the depository.

Because operational processes can differ by issuer and RTA, check instructions early. Do not wait until the week of the coupon date.

Worked Example: Form 121 for Bond Interest TDS

Let us use a hypothetical example. This is only for explanation and is not a live issuance or investment recommendation.

Hypothetical bond interest example

Assume Meera, a resident senior citizen, holds listed NCDs with a face value of Rs 3,00,000. The coupon is 8% annually, paid once a year. Her expected bond interest is Rs 24,000.

Meera also has pension income and FD interest. After estimating all income, deductions, and rebate eligibility for the tax year, her tax advisor concludes that her final tax liability should be nil. She submits Form 121 before the coupon date to the relevant payer with correct PAN, income estimate, bond details, and bank details.

If the declaration is accepted, the Rs 24,000 coupon may be paid without TDS. Meera still tracks the income and reports it correctly while filing her return, if she is required to file.

What happens if TDS is deducted anyway?

Suppose Meera submits the declaration late, after the coupon has already been processed. TDS may already have been deducted. In that case, Form 121 may not reverse the deduction instantly.

Her route is usually to reconcile the deducted amount through Form 26AS or AIS and claim credit while filing her income tax return. If her final tax liability is nil, the excess TDS may be refunded through the tax return process. This is exactly the inconvenience Form 121 is designed to reduce when submitted on time.

Form 121 Checklist for Bond Investors

Use Form 121 as a compliance document, not as a casual payout preference.

Quick pre-submission checklist

Before submitting, confirm:

- You are eligible under the taxpayer category and residential status rules.

- Your estimated total income for the tax year leads to nil tax liability.

- You have included all income, not only bond coupon income.

- You know the coupon date and have submitted before credit or payment.

- Your PAN is valid and operative.

- Bond details and payer details are correct.

- You have retained an acknowledgement or proof of submission.

- You understand that Form 121 does not apply to capital gains on bond sale.

- You will still reconcile Form 26AS and AIS during return filing.

Scannable summary: Use Form 121 only when these are true

Use Form 121 when you are eligible, tax liability is nil, income is covered, and the payer accepts the declaration before payment. Do not use it if your tax liability is positive, you are not an eligible resident taxpayer, or you are trying to avoid tax on bond capital gains.

Common Mistakes with Form 121 and TDS on Bond Interest

Most errors come from treating Form 121 like a formality. It is not. It is a declaration about your estimated tax position.

Do not use Form 121 for capital gains on bonds

Bond interest and bond capital gains are different tax events. Form 121 is relevant for specified income where TDS may otherwise be deducted, such as interest on securities. It is not a tool to avoid tax on gains from selling a bond above your purchase price.

Do not submit after the coupon date and expect reversal

The timing matters. If the payer has already processed interest and deducted TDS, a late declaration may not undo the deduction. You may need to claim credit or refund through the return-filing process.

Do not ignore total estimated income

Eligibility is not based on one bond. It is based on estimated total income and tax liability for the tax year. If you earn salary, pension, rent, business income, FD interest, mutual fund income, or capital gains, include it.

Form 121, TDS Refunds, and Post-tax Bond Income Planning

Form 121 is part of cash-flow planning. The practical question: prevent TDS before the coupon date, or accept deduction and claim credit later?

Form 121 vs refund after TDS on bond interest

If you are eligible and submit Form 121 on time, the payer may credit bond interest without TDS. That can help retirees, low-income investors, and investors with nil tax liability avoid waiting for a refund.

If TDS is already deducted, the money is not lost. It should appear in Form 26AS or AIS, subject to correct reporting. You can claim credit while filing your return. The issue is timing. Refunds may take time, and reconciliation errors create work. For planned cash flows, prevention is cleaner.

How Form 121 affects post-tax bond income planning

Bond yields are usually discussed before tax. Your real outcome depends on coupon, purchase price, holding period, credit risk, and personal tax position. Form 121 does not improve target yield or reduce issuer risk. It only changes whether tax is deducted upfront.

That matters when comparing fixed deposits, listed NCDs, and other income products. A periodic coupon can look attractive on screen, but bank credit may differ if TDS applies. If you qualify for Form 121, coupon cash flow may track gross interest more closely during the year, while final tax is settled through your return.

Where EquiRize investors use Form 121 information

Use Form 121 thinking at three points. Before investing, check the coupon schedule against your tax-year income estimate. After purchase, note coupon dates and submission deadlines. During return filing, reconcile credited interest, deducted TDS, and declared income.

EquiRize can help with the investing side by showing listed bond details such as issuer, rating, maturity, coupon schedule, and offer documents. The tax declaration remains your responsibility. Treat Form 121 as one input in bond income planning, alongside credit risk, liquidity, maturity, and concentration.

Conclusion: Use Form 121 for Bond Investors Carefully

Form 121 for bond investors can make coupon cash flows cleaner for taxpayers with nil tax liability. Used properly, it prevents unnecessary TDS and reduces refund delays. Used casually, it can create inaccurate declarations and compliance trouble.

Before submitting the form, check your full tax-year income, coupon schedule, PAN status, issuer or RTA process, and submission deadline. Then keep proof of submission and reconcile your tax records later.

EquiRize Securities Private Limited is a SEBI-registered Online Bond Platform Provider and a stock broker in the debt segment of BSE and NSE. Investors can use EquiRize to review listed bond opportunities, issuer details, ratings, maturity dates, coupon schedules, and offer documents before investing.