What Credit Spread in Bonds Tells Investors

What Credit Spread in Bonds Tells Investors

A higher bond yield can look attractive at first glance. But in debt investing, yield is rarely just a number. It is often a message.

Credit spread in bonds is one way to read that message. It tells you how much extra yield a corporate bond or NCD offers over a comparable government security. That extra yield is the market's way of pricing risks such as issuer default, liquidity, structure, and uncertainty.

For Indian investors comparing listed bonds, credit spread can be a useful first filter. It helps you ask sharper questions: Why is this bond offering more? Is the extra yield enough for the risk? Is the spread because of credit quality, longer tenure, low liquidity, or a feature hidden in the term sheet?

This guide explains credit spread meaning, formula, examples, investor signals, and the limits of the metric.

Credit Spread Meaning in Bonds

Start with the core idea before comparing products. Whether you are looking at NCDs and corporate bonds or other listed debt securities, spread helps separate headline yield from the extra risk premium built into that yield.

What is credit spread in bonds?

Credit spread is the difference between the yield of a non-government bond and the yield of a comparable government security with a similar maturity.

In simple terms:

Credit spread = Corporate bond yield - Comparable G-Sec yield

Government securities are usually treated as the benchmark because they carry sovereign backing. Corporate bonds do not. So investors generally expect corporate issuers to offer additional yield for taking issuer-specific risk.

That additional yield is the spread. It is usually expressed in basis points. One basis point equals 0.01%. So a spread of 2.00 percentage points is 200 basis points.

Credit spread vs yield spread in bonds

The terms credit spread and yield spread are often used together, but they are not always identical.

A yield spread can refer to any yield difference between two debt instruments. For example, the spread between a 3-year bond and a 10-year bond, or between two government securities.

A credit spread is more specific. It focuses on the extra yield linked to credit risk when comparing a corporate bond or NCD with a government benchmark of similar maturity.

Why basis points matter when comparing bonds

Bond investors use basis points because small percentage differences can matter on larger ticket sizes.

A 75 basis point spread may sound small. But on Rs. 5,00,000, that is Rs. 3,750 a year before tax, assuming scheduled payments happen. Basis points make spreads easier to compare across issuers, ratings, and maturities without rounding away meaningful differences.

Credit Spread Formula and Worked Example

The formula is simple, but the inputs matter. Use comparable maturities, use market yield rather than only coupon, and remember that spread is usually read alongside yield to maturity, rating, liquidity, and issue structure.

How to calculate credit spread in bonds

The basic credit spread formula is straightforward:

Credit spread = Yield to maturity of corporate bond - Yield of comparable G-Sec

Use yield to maturity, not just coupon rate. Coupon tells you the stated interest rate on face value. YTM reflects price, coupon, redemption value, and time left to maturity.

Also match maturity as closely as possible. Comparing a 2-year corporate bond with a 10-year G-Sec will mix credit risk with tenure risk. A cleaner comparison uses a benchmark G-Sec or yield curve point close to the bond's remaining maturity.

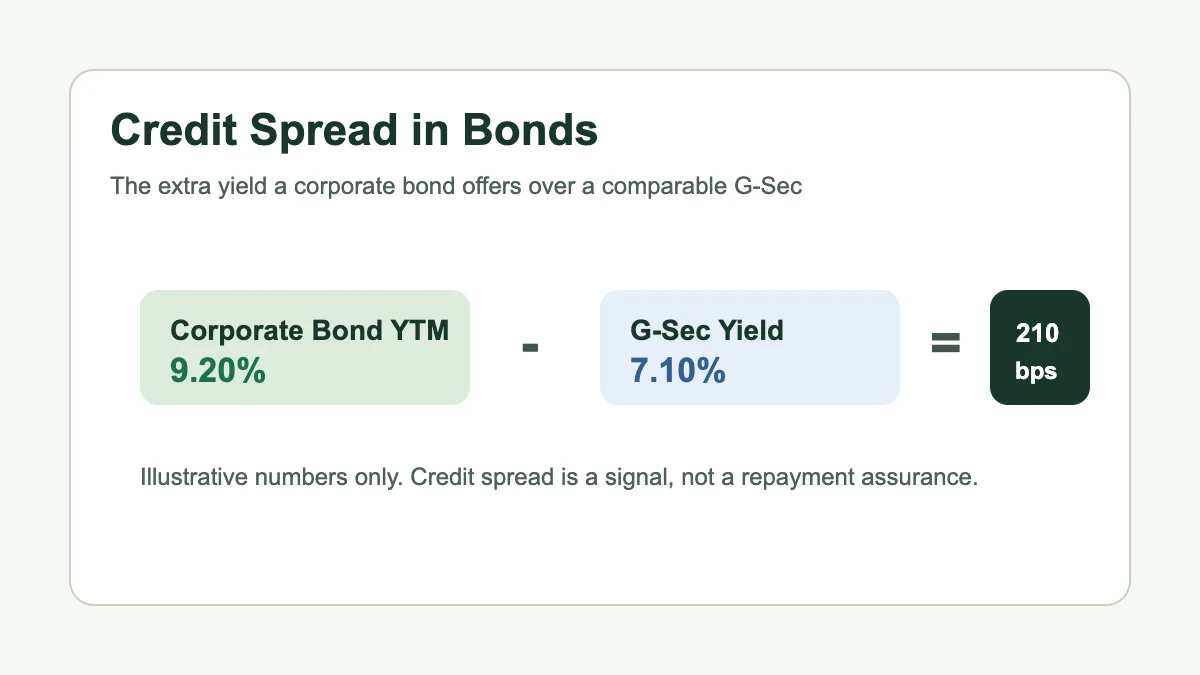

Credit spread example for Indian bonds

Assume this is an illustrative, hypothetical example:

- A 3-year corporate bond has an indicative YTM of 9.20%.

- A comparable 3-year G-Sec yield is 7.10%.

- Credit spread = 9.20% - 7.10% = 2.10%.

That means the corporate bond offers 210 basis points over the government benchmark.

The next question is not "Is 210 bps good?" The better question is: what is that 210 bps compensating you for?

It may reflect lower credit rating, issuer leverage, sector risk, low secondary market liquidity, secured or unsecured structure, or weaker investor appetite for that issuer.

What the spread does not tell you

Credit spread does not guarantee repayment. It does not replace credit analysis, rating rationale, security cover, covenants, or offer documents. It is a signal, not a complete due diligence report.

Corporate Bond Credit Spread Signals Investors Should Read

For corporate bonds in India, spread movement can act like a market mood check. It does not tell the whole story, but it can point you toward the questions worth asking first.

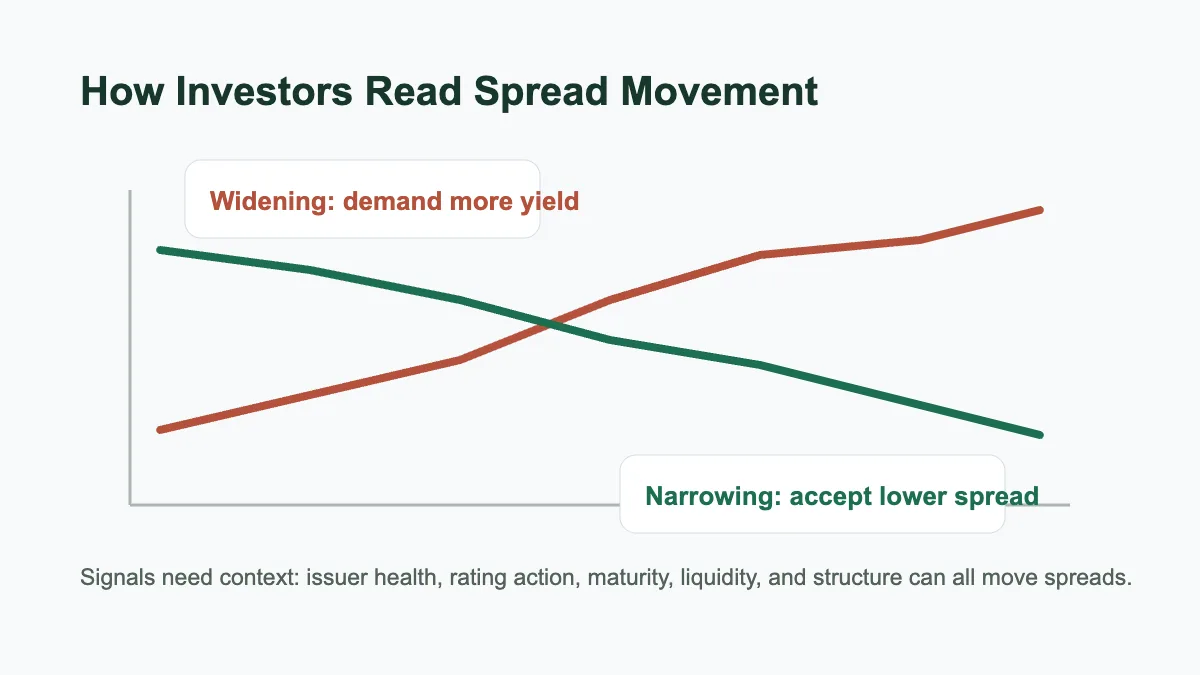

Why credit spreads widen in bond markets

Credit spreads widen when investors demand more yield for taking corporate bond risk.

This can happen because of issuer-specific concerns, weaker sector outlook, lower liquidity, market stress, rising default expectations, or heavy supply of similar bonds. In simple words, the market is asking to be paid more for risk.

For a bond you already hold, widening spreads may also affect market price. If newer bonds from similar issuers offer higher yields, older bonds with lower yields may trade at lower prices in the secondary market.

What does narrowing credit spread mean?

A narrowing spread means the extra yield over the benchmark has reduced.

This may suggest improving market confidence, stronger demand for corporate bonds, better perceived credit conditions, or reduced liquidity premium. It can also happen when investors are willing to accept lower incremental yield for a given issuer or rating category.

Narrower spreads are not automatically good or bad. They can indicate comfort. They can also indicate that investors are being paid less for the risk they are accepting.

Credit spread and bond price relationship

Bond prices and yields move in opposite directions. When required yield rises, bond price generally falls. When required yield falls, bond price generally rises.

Credit spread is one part of that yield movement.

If the benchmark G-Sec yield is stable but a corporate bond's spread widens, the corporate bond's yield may rise and its price may fall. If spreads narrow, its yield may fall and price may improve, assuming other factors remain unchanged.

This matters most if you plan to sell before maturity. If you intend to hold until scheduled redemption, interim price movement may matter less, but issuer repayment risk still matters.

Credit spread vs credit rating

Credit rating and credit spread answer related but different questions.

A rating is an opinion from a credit rating agency on timely repayment ability. A credit spread is the market's pricing of additional yield over a benchmark.

Two bonds with the same rating can trade at different spreads because of maturity, liquidity, security, issuer reputation, group support, structure, or recent news. This is why rating alone is not enough. Spread adds market context.

Bond Credit Spread Checklist Investing

Once the spread looks interesting, move from comparison to diligence. A bond can offer a higher indicative yield for several reasons, and not all of them are visible from the yield number alone.

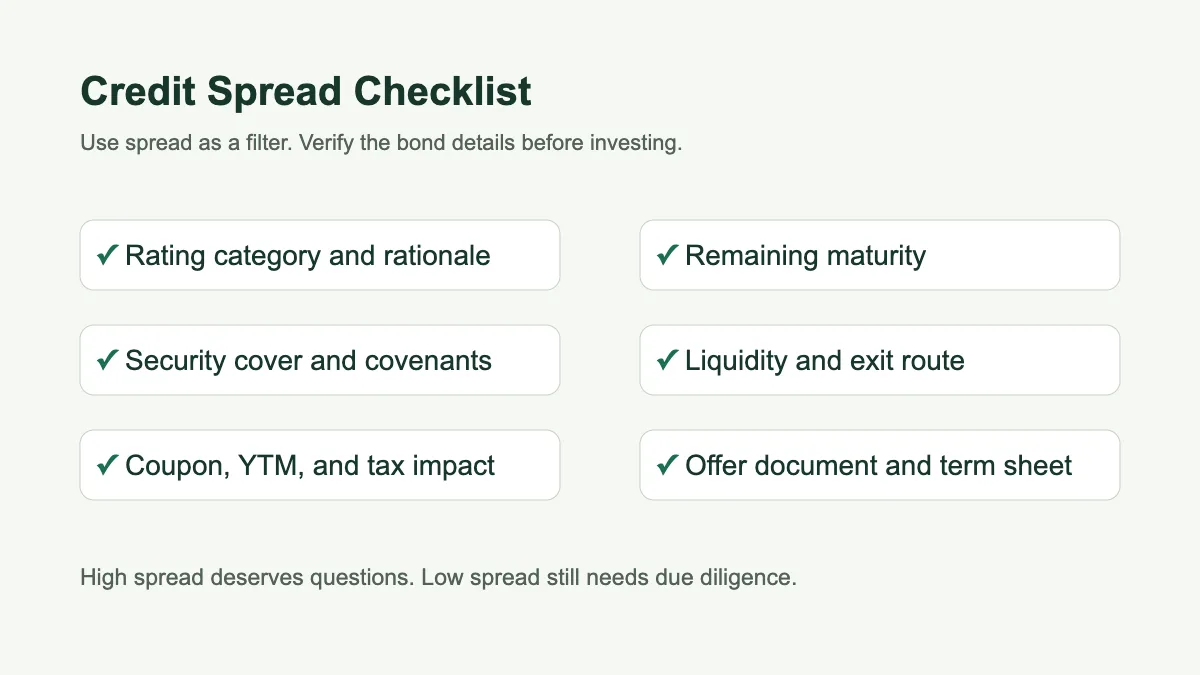

How investors use credit spread in corporate bonds

Use credit spread as a comparison tool, not as a buy signal. Before investing, compare the bond's spread against similar bonds by:

- Rating category

- Remaining maturity

- Issuer sector

- Security cover

- Coupon frequency

- Call or put options

- Listing and liquidity

- Tax impact

- Minimum investment size

If one bond offers a much higher spread than peers, slow down. The market may be pricing a risk you have not yet spotted.

If one bond offers a much lower spread than peers, check whether the issuer quality, security, liquidity, or structure explains it.

Red flags when a bond spread looks too high

A very high spread may point to genuine risk. Check whether the issuer has high leverage, weak profitability, recent rating actions, promoter stress, sector pressure, delayed payments elsewhere, or low trading volumes.

Also inspect the term sheet. A high headline YTM may come from call features, step-up structures, amortisation, lower liquidity, or a price that assumes you can hold until maturity.

When a low spread may still be reasonable

A low spread is not always unattractive. It may reflect stronger credit quality, better liquidity, shorter tenure, secured structure, or wider investor demand.

For conservative investors, a lower spread may still fit if the bond aligns with cashflow needs, time horizon, and risk appetite.

Credit Spread Risk: Limits of the Metric

Credit spread is useful because it compresses market pricing into one number. Its weakness is the same: one number cannot carry every detail inside the bond term sheet.

Liquidity, tenure, and structure can distort spreads

Credit spread works cleanly when comparisons are clean. In real markets, they often are not.

A bond may show a higher spread because it is less liquid, not only because its issuer is riskier. A longer-maturity bond may carry more interest rate sensitivity. A callable bond may behave differently from a plain-vanilla bond. A secured bond and an unsecured bond from the same issuer may deserve different spreads.

So, compare like with like. Same rating is not enough.

Why offer documents still matter

The spread tells you what the market is asking today. The offer document tells you what you are actually buying.

Read issuer financials, risk factors, security details, covenants, repayment schedule, trustee disclosures, rating rationale, and taxation notes. On a SEBI-registered Online Bond Platform Provider, use platform disclosures as a starting point, then verify the core terms in the offer documents.

Quick Summary: Credit Spread Investor Signals

Use this quick read:

- Wider spread: higher perceived risk, lower liquidity, weaker demand, or issuer-specific concern may be present.

- Narrower spread: stronger demand or improved market comfort may be present.

- Very high spread: investigate before chasing yield.

- Very low spread: check whether the risk-reward still works after tax and liquidity.

- Same rating, different spread: maturity, structure, liquidity, and issuer perception may explain the gap.

- Spread is useful, but not final. Always read the term sheet and offer documents.

Conclusion: Use Credit Spread as a Filter, Not a Verdict

Credit spread in bonds helps investors move beyond the headline yield. It shows how much extra yield a corporate bond offers over a comparable government benchmark, and it can highlight what the market may be pricing in.

But spread is only one lens. A smart bond review also checks rating rationale, issuer financials, security, maturity, liquidity, tax impact, and the offer document. If you are still building the basics, start with this guide on investing in bonds in India with Rs. 10,000.

For investors using EquiRize, a SEBI-registered OBPP and debt-segment broker on BSE and NSE, credit spread can be part of a clearer comparison process. Use it to shortlist bonds, frame better questions, and avoid judging yield without context.

Disclaimer: This content is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Please consult a SEBI-registered investment adviser before investing. Investments in debt securities are subject to risks including delay in payment and default in payment. Please read all the offer documents carefully before investing.