Bonds vs P2P Lending India: Returns, Risks & How to Choose

For Indian investors looking beyond fixed deposits, the bonds vs P2P lending India comparison has become more relevant in 2026. Both can offer income potential above traditional bank deposits, but they are not the same kind of credit exposure. Bonds are debt securities issued by governments, public sector entities, financial institutions, or companies. P2P lending is lender-to-borrower credit facilitated by an NBFC-P2P platform.

This guide compares returns, risk, liquidity, regulation, tax treatment, minimum investment, and portfolio fit so retail investors, HNIs, NRIs, and IFAs can make a clearer decision.

Quick Comparison: Bonds vs P2P Lending at a Glance

| Factor | Bonds in India | P2P Lending in India |

|---|---|---|

| Basic structure | Debt security issued by a government or corporate issuer | Loan exposure to borrowers through an NBFC-P2P platform |

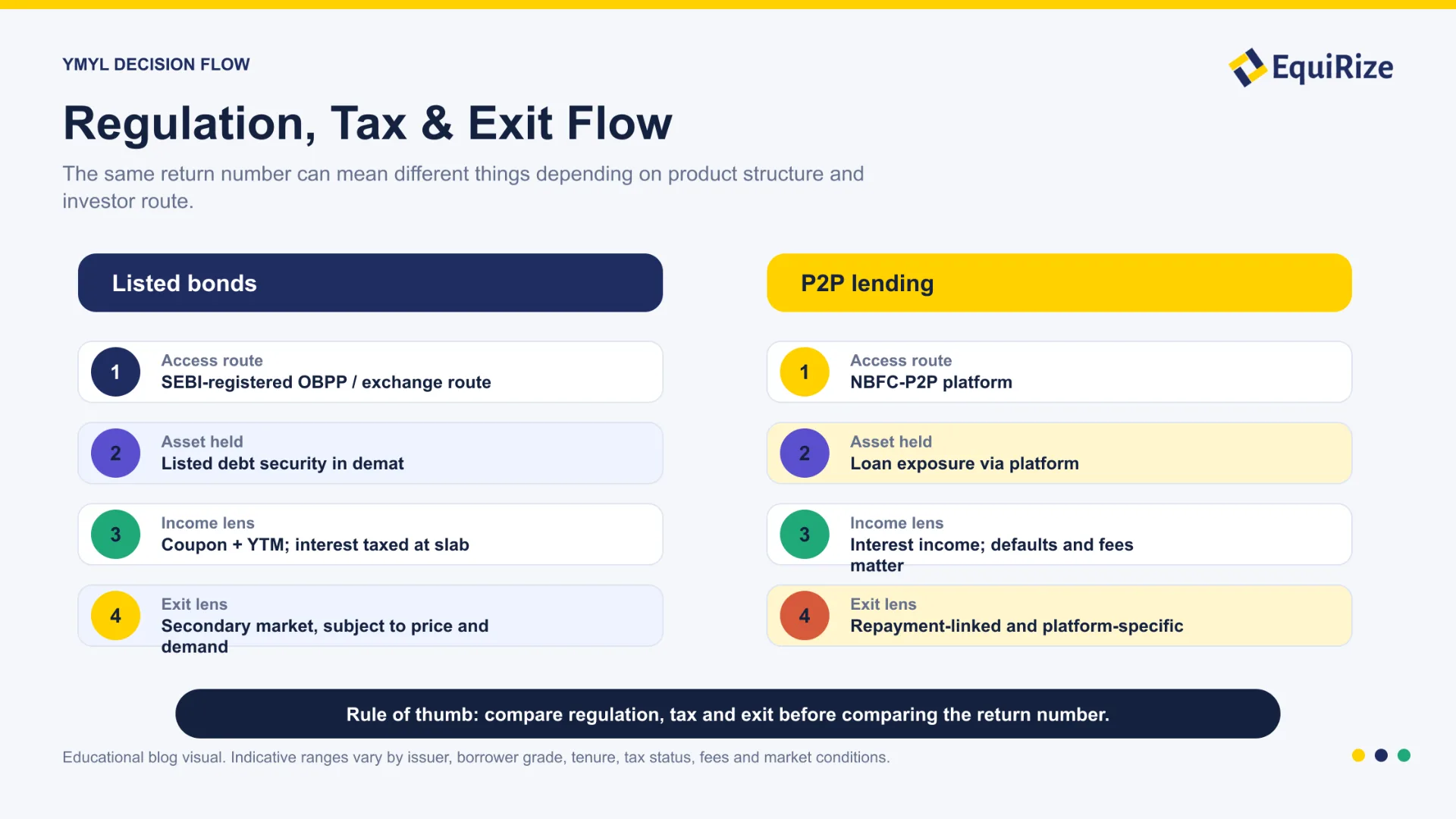

| Regulator/framework | SEBI framework for listed securities and OBPPs | RBI NBFC-P2P framework |

| Typical return metric | Coupon rate and yield to maturity (YTM) | Target yield or realised lending return |

| Indicative return range | Often around 7-12% p.a., depending on issuer, rating, tenure, and market pricing | Often marketed around 10-18% p.a., depending on borrower risk grade and platform methodology |

| Main risk | Issuer credit risk, interest-rate risk, and liquidity risk | Borrower default risk, platform risk, and lower liquidity |

| Holding format | Usually held in demat form for listed bonds | Platform-facilitated lending exposure |

| Exit route | Secondary market on NSE/BSE, subject to buyers and price | Usually linked to borrower repayments and platform terms |

| Tax treatment | Interest taxed at slab rate; capital gains may apply on sale | Interest income generally taxed at slab rate |

| Accessibility | Some listed debt securities now have face value as low as ₹10,000 where eligible | Platform minimums may be lower, often ₹500-₹1,000 per borrower depending on the platform |

| Best-fit role | Core fixed-income allocation, income planning, maturity matching | Limited higher-risk credit allocation, if suitable |

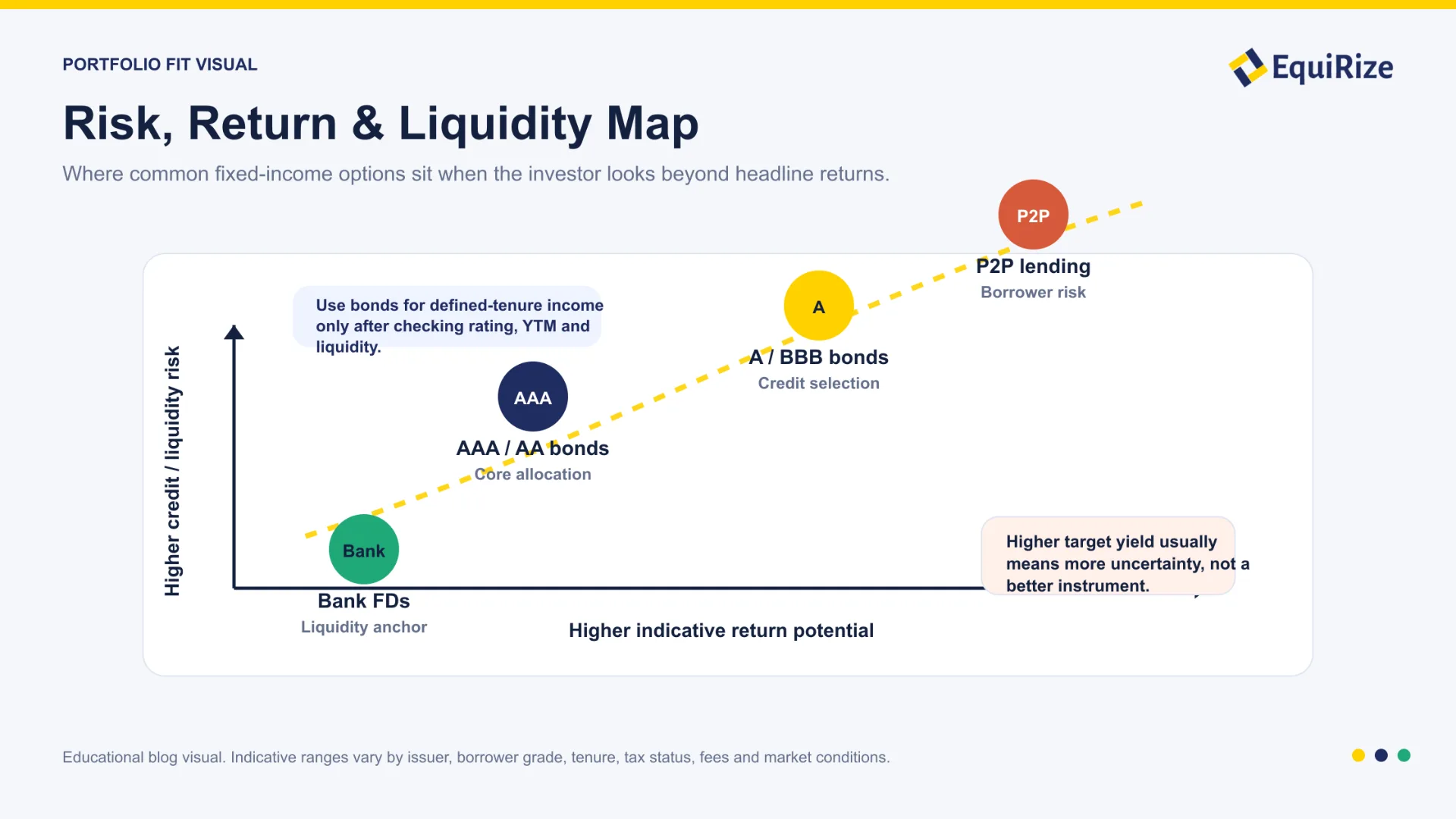

The table is useful, but it should not be read as a ranking. A 10% bond YTM and a 10% P2P target yield do not carry the same risk, liquidity, tax, or regulatory context.

What Are Bonds in India? How They Work for Retail Investors

Bonds are debt instruments. When you buy a bond, you are effectively lending money to an issuer. In return, the issuer agrees to pay a coupon at stated intervals and repay the face value at maturity, subject to its ability to meet those obligations.

For retail investors, the most important terms are:

- Coupon rate: the stated interest rate on the bond's face value.

- Yield to maturity (YTM): the annualised pre-tax return if the bond is bought at the quoted price, all payments are received as scheduled, and the bond is held until maturity.

- Credit rating: an agency assessment of the issuer's ability to meet debt obligations.

- Maturity: the date on which principal is due to be repaid.

- Secondary market: the market where listed bonds may be sold before maturity, subject to demand and price.

For investors comparing corporate bonds India retail investors can now access with P2P lending, the key distinction is that listed bonds are securities. They carry issuer-level risk, but they also come with instrument-level information: issuer, rating, coupon, maturity, repayment structure, and offer document.

Types of Bonds Available in India

Indian investors can choose from several bond categories.

- Government securities (G-Secs) are issued by the Government of India and are generally considered the lowest credit-risk rupee debt instruments.

- State Development Loans (SDLs) are issued by state governments.

- PSU bonds are issued by public sector undertakings.

- Corporate bonds and NCDs are issued by companies and financial institutions.

- Tax-free bonds, where available in the secondary market, have interest that is exempt from income tax under specified conditions.

The risk-return profile changes across categories. G-Secs typically carry lower credit risk and lower yields. Lower-rated corporate bonds may offer higher indicative yields, but investors take more issuer credit risk. That is why the phrase high yield fixed income India 2026 should always be read with credit rating, tenure, liquidity, and tax in the same frame.

How to Buy Bonds: Exchanges, OBPPs, and Demat

Retail investors can access listed bonds through recognised exchanges, brokers, and SEBI-registered Online Bond Platform Providers (OBPPs). SEBI introduced the OBPP framework to bring online bond distribution into a defined regulatory perimeter and require platforms to operate through the recognised stock exchange debt segment.

EquiRize is a SEBI-registered OBPP that facilitates access to listed bonds. The bond, once bought, is held in the investor's demat account. EquiRize is a facilitator, not the issuer, custodian, or investment advisor.

This matters because a SEBI OBPP online bond platform India investor uses should provide structured information such as issuer name, credit rating, coupon, maturity, YTM, payment schedule, and offer documents. SEBI registration does not mean SEBI has approved any specific bond or return. Investors still need to evaluate risk.

What is P2P Lending in India? How the RBI Framework Works

RBI's NBFC-P2P directions set rules for eligibility, disclosure, fund movement, escrow accounts, exposure limits, and operating conduct. Funds must flow through bank accounts and escrow mechanisms, not through cash. RBI also requires fund transfers in the escrow accounts to be completed within the T+1 bank-working-day framework, effective from November 15, 2024.

Exposure limits are central. A lender's aggregate exposure across P2P platforms is capped under RBI rules, and exposure to a single borrower is also capped. Higher aggregate exposure may require additional net-worth certification. These limits exist because P2P lending is credit exposure, not a deposit.

The language also matters. In this section, the user is a lender, not an investor. The product is lending, not investing. That distinction is not cosmetic; it reflects how RBI frames the activity.

What Happened After the 2024 RBI Enforcement Actions?

In 2024, RBI tightened and clarified the P2P lending framework after concerns around product presentation, fund flow, and the way some platforms were positioning returns. The regulatory direction became clearer: NBFC-P2P platforms should act as intermediaries, not as balance-sheet lenders, deposit substitutes, or products promising principal recovery.

For lenders, the practical change was sharper risk disclosure. P2P platforms cannot present borrower credit exposure as principal-protected income. The lender must understand that repayment depends on borrowers and that the platform does not eliminate default risk.

This is one reason bond investment vs P2P lending risk should be evaluated through structure first and returns second.

Returns Compared: What Can You Realistically Earn?

Returns vary across both products. The ranges below are indicative and market-dependent, not promised outcomes.

| Instrument/risk tier | Indicative annual return range | What drives the range |

|---|---|---|

| G-Secs / SDLs | ~7-8% p.a. | Sovereign or state-backed credit, maturity, rate cycle |

| AAA / AA listed bonds | ~7.5-10% p.a. | Issuer quality, tenure, liquidity, market pricing |

| A / BBB listed bonds | ~10-12%+ p.a. | Higher issuer credit risk and lower liquidity |

| P2P lower-risk borrower grades | ~9-12% p.a. target yield | Borrower profile, platform methodology, defaults |

| P2P higher-risk borrower grades | ~13-18% p.a. target yield | Higher borrower credit risk and recovery uncertainty |

The point is not that one number is larger. The point is whether the yield compensates for the risk and liquidity. In credit products, higher yield usually means the investor or lender is accepting more uncertainty.

Bond Yields in India: What to Expect by Rating Category

Bond yields in India usually rise as credit quality falls, tenure increases, or liquidity reduces. A AAA-rated issuer may offer lower YTM than a BBB-rated issuer because the market views the credit risk differently. A longer-tenure bond may also have more interest-rate sensitivity than a shorter-tenure bond.

The right way to compare bond opportunities is not only coupon. Use YTM, credit rating, issuer financials, maturity, security structure, and liquidity together. A higher YTM without credit context is not a complete investment case.

P2P Lending Returns: Indicative Range and Risk Grade Impact

P2P lending returns India per annum are usually presented as target or expected ranges. These depend heavily on borrower grade. Lower-risk borrower grades may offer lower target yields. Higher-risk borrower grades may show higher target yields, but they carry greater default probability and recovery uncertainty.

The lender's realised return can differ from the displayed range because of borrower delays, defaults, fees, taxes, and reinvestment gaps. For this reason, P2P lending should be treated as borrower credit exposure, not as a fixed-income substitute with a certain outcome.

Risk Profile: What Can Go Wrong with Bonds and P2P Lending?

This is the section to read slowly. Returns are visible upfront; risk shows up later.

With bonds, the risk is usually concentrated around the issuer and the instrument. With P2P lending, the risk is spread across borrowers but depends on borrower repayment behaviour and platform servicing.

Neither product should be judged only by headline yield. A higher yield may compensate for higher credit risk, but it can also signal risk that the investor has not fully understood.

Risks Specific to Bonds

The first risk is credit risk: the issuer may delay or miss coupon or principal payments. Ratings help, but they are not permanent.

The second is interest-rate risk. If market rates rise, the market price of an existing bond may fall. This matters if the investor exits before maturity.

The third is liquidity risk. A bond may be listed on NSE or BSE and still trade infrequently. Exit price can differ from theoretical value.

The fourth is concentration risk. Holding too much of one issuer, sector, or rating category can weaken portfolio resilience.

Risks Specific to P2P Lending

The main risk is borrower default. If borrowers do not repay, the lender's realised return falls and principal recovery may be partial or delayed.

The second is platform risk. The platform facilitates matching, disclosures, servicing, and collections. Operational weakness can affect the lender experience.

The third is liquidity risk. P2P lending exposure is usually linked to borrower repayment schedules. Early exit may be limited or unavailable.

The fourth is presentation risk. If a lender looks only at target yield and ignores default behaviour, the risk is understated.

Liquidity: Can You Exit Before the Tenure Ends?

Listed bonds may offer an exit through the secondary market. If there is demand, the investor can sell before maturity through the relevant market route. But this does not mean exit is certain or that the price will be favourable. Bond prices move with interest rates, credit perception, and liquidity.

P2P lending is generally less liquid. The lender's cash flows usually come back as borrowers repay. If the loan tenure is 12, 24, or 36 months, the lender should assume the money may be tied to that repayment schedule, subject to platform-specific terms.

For near-term needs, FDs or liquid instruments may still be more suitable. For defined income goals, listed bonds can work if maturity and liquidity assumptions are realistic. For P2P lending, the allocation should be sized with the assumption that early exit may not be available.

Minimum Investment and Accessibility in 2026

Bond access has improved materially for retail investors. SEBI's 2024 denomination circular reduced the face value for certain debt securities and non-convertible redeemable preference shares to ₹10,000, subject to specified conditions. This made parts of the listed bond market more accessible than the older ₹1 lakh or ₹10 lakh denominations.

P2P lending platforms may allow smaller lender allocations, often around ₹500-₹1,000 per borrower depending on platform policy. Smaller ticket size can help diversify across borrowers, but it does not eliminate default risk.

Minimum investment bonds vs P2P lending India comparisons should therefore look beyond ticket size. A lower entry amount improves access, but the real question is whether the product fits the investor's liquidity need, risk capacity, tax position, and monitoring ability.

Tax Treatment: How Bonds and P2P Lending Income is Taxed in India

Interest income from bonds is generally taxed at the investor's applicable slab rate. If a listed bond is sold before maturity, capital gains treatment may apply depending on the holding period, listing status, and prevailing tax rules. Investors should also account for accrued interest and transaction price when calculating post-tax outcomes.

FD interest is also generally taxed at slab rate, with TDS rules depending on the depositor and issuer. Corporate FDs may require closer credit and tax review because issuer quality and premature withdrawal terms vary.

Tax on P2P lending interest income India is generally evaluated as interest income. Lenders should review platform statements, fees, defaults, recoveries, and TDS treatment where applicable. The tax result can be messy if some borrower repayments are delayed or unrecovered.

For HNIs and NRIs, post-tax yield matters more than headline yield. A higher pre-tax number may not remain attractive after slab tax, fees, defaults, and liquidity cost.

Who Should Choose Bonds, and Who Should Choose P2P Lending?

Conservative investors may prefer high-quality listed bonds and bank FDs because the structure, documentation, and maturity profile are easier to evaluate. They should still understand credit risk and liquidity risk before buying bonds.

Yield-seeking investors may consider lower-rated bonds or P2P lending, but only as part of a clearly sized risk allocation. The higher the target yield, the more important it becomes to understand default risk, recovery process, and exit limitations.

NRIs should check eligibility, demat setup, NRE/NRO funding routes, taxation, and repatriation before using either route. P2P rules and platform eligibility may differ from bond access, so assumptions should be verified before allocating.

IFAs should map the product to the client role: FDs for simple liquidity, listed bonds for structured income and maturity planning, and P2P lending only where the client understands borrower default risk.

Can You Hold Bonds and P2P Lending Together?

Yes, but they should not do the same job in a portfolio.

A sensible structure may keep FDs for emergency needs, use listed bonds for planned fixed-income allocation, and place P2P lending, if used, in a limited higher-risk credit bucket. Investors can explore curated bond deals on EquiRize to compare issuer, rating, YTM, maturity, and documentation before making a decision.