Bonds vs Fixed Deposits India 2026: Returns, Tax & Safety

Fixed deposits have long been the default savings choice for Indian investors. But in 2026, with RBI rate cycles shifting and inflation eating into post-tax FD returns, more investors are asking a sharper question: should I stick with FDs, or is it time to add bonds to my portfolio?

This guide compares both options across the factors that matter most — returns, safety, taxation, and liquidity — so you can decide what fits your financial goals in 2026.

What Are Fixed Deposits? How They Work in 2026

Fixed Deposits (FDs) continue to be one of the most preferred fixed income investments in India, especially among conservative investors looking for predictable returns and capital stability. Unlike market-linked products, FDs offer a fixed interest rate for a predetermined tenure, making them a popular choice among investors seeking safe investments in India.

In a fixed deposit, investors park a lump sum amount with a bank or NBFC for a specific period ranging from a few days to several years. In return, the institution pays a fixed rate of interest, regardless of market fluctuations. This predictability makes FDs one of the most widely used low risk investment options in India.

There are different types of FDs available in 2026, including regular FDs, senior citizen FDs, tax-saving FDs, and cumulative or non-cumulative deposits. Interest rates may vary depending on the issuer, tenure, and prevailing RBI policy rates.

FD Interest Rates Across Major Banks in India (2026)

FD interest rates in India 2026 generally range between 6.5% and 8.5% annually, depending on the bank or NBFC. Senior citizens may receive slightly higher interest rates. While FDs are considered stable, returns may sometimes struggle to outperform inflation on a post-tax basis.

For example, an investor placing ₹5 lakh in a 3-year FD at 7.5% annually can earn stable returns without market volatility. However, after taxation and inflation adjustment, the effective real return may reduce significantly.

Types of FDs — Regular, Senior Citizen, Tax-saving

Investors can choose from different types of fixed deposits in India based on their financial goals, income needs, and investment horizon.

Regular Fixed Deposits are the most common type of FD, where investors deposit funds for a fixed tenure and earn predetermined interest. These are suitable for individuals seeking stable and predictable returns without market-linked risks.

Senior Citizen Fixed Deposits are designed specifically for investors above the eligible age limit, usually offering slightly higher FD interest rates compared to regular deposits. These FDs are widely preferred by retirees looking for stable income and relatively safe investments in India.

Tax-Saving Fixed Deposits come with a mandatory lock-in period of five years and may offer tax deduction benefits under applicable income tax provisions. However, premature withdrawal is generally not allowed before maturity.

Choosing the right type of FD depends on factors such as liquidity requirements, tax planning, and income expectations.

What Are Bonds? A Simple Guide for Indian Investors

As Indian investors look for alternatives beyond traditional fixed deposits, bonds have emerged as one of the most popular fixed income investments in India in 2026. A bond is essentially a loan given by an investor to a government entity, corporation, or financial institution in exchange for regular interest payments and repayment of principal at maturity.

Unlike equity investments, bonds are designed to offer relatively stable returns with lower volatility, making them attractive for investors seeking predictable income and portfolio diversification. Depending on the issuer, tenure, and credit rating, bond investments in India can often provide higher yields compared to conventional fixed deposits.

How Bond Interest (Coupon) Payments Work

When investors purchase a bond, they earn interest, commonly known as a coupon, at fixed intervals. At the end of the bond tenure, the invested principal amount is returned. Bond prices may also fluctuate in the secondary market depending on interest rates and market demand.

For example, if an investor buys a ₹1 lakh corporate bond offering 9% annual interest for 3 years, they may receive ₹9,000 annually as interest, along with repayment of the principal at maturity, subject to issuer terms.

Types of bonds — government, corporate, PSU, tax-free

Here is the table depicting the types of bonds:

| Type of Bond | Key Feature |

| Government Bonds | Backed by the Government of India with relatively lower risk |

| Corporate Bonds | Issued by companies and may offer higher returns |

| PSU Bonds | Issued by public sector undertakings |

| Tax-Free Bonds | Interest earned may be tax-exempt under applicable rules |

| AAA Rated Bonds | Highest credit-rated bonds with relatively lower default risk |

Among these, AAA rated bonds in India are widely preferred by conservative investors because they are issued by financially strong entities with high creditworthiness.

Why Bond Investments Are Growing in India

The growing popularity of high return bonds in India is driven by rising investor awareness, digital bond platforms, and the need for better post-tax returns. Many investors are now exploring corporate bonds vs FD options to diversify beyond traditional savings products.

Additionally, bonds offer flexibility across risk profiles, tenures, and return expectations, making them suitable for retirees, income-focused investors, and individuals seeking balanced investment portfolios.

Bonds vs Fixed Deposits: Key Differences Explained

When comparing bonds vs fixed deposits in India 2026, the right choice depends on an investor’s financial goals, risk appetite, liquidity needs, and return expectations. While both are considered fixed income investments in India, they differ significantly in terms of returns, taxation, flexibility, and risk exposure.

Fixed deposits are widely preferred for stability and predictable returns, especially among conservative investors. Bonds, on the other hand, can offer higher yields and portfolio diversification, particularly through corporate bonds and AAA rated bonds in India. As more investors evaluate where to invest in 2026 India, understanding these differences becomes essential for making informed financial decisions.

| Feature | Bonds | Fixed Deposits |

| Returns | Potentially higher yields depending on issuer and tenure | Fixed and predictable returns |

| Safety | Depends on issuer credit rating | Depends on bank or NBFC stability |

| Liquidity | Tradable in secondary market in many cases | Premature withdrawal may attract penalties |

| Taxation | Tax treatment varies by bond type and holding period | Interest taxed as per income slab |

| Tenure Flexibility | Available across short, medium, and long tenures | Fixed tenure selected at investment |

| Risk Level | Includes credit and interest rate risk | Comparatively lower risk |

| Inflation Impact | Better potential to beat inflation | Real returns may reduce after inflation |

| Suitable For | Investors seeking income and diversification | Investors prioritizing capital protection |

One of the biggest differences in the corporate bonds vs FD debate is return potential. For example, a high-quality corporate bond may offer yields between 8% and 10%, while many bank FDs in India 2026 may offer comparatively lower rates. However, higher returns in bonds may come with additional risks linked to issuer credit quality and market interest rate movements.

Another key consideration is taxation. In the fixed deposit vs bonds returns comparison, post-tax earnings can vary significantly depending on the investor’s tax slab and the type of bond investment chosen. This makes tax efficiency an important factor while evaluating bond vs FD taxation in India.

For investors seeking predictable income with low complexity, FDs may remain a suitable option. Meanwhile, investors looking for potentially higher income, diversification, and flexible investment opportunities may consider adding bonds to their portfolio.

Return Comparison: Bonds vs FD Returns in 2026

For most investors comparing bonds vs fixed deposits India 2026, returns remain one of the biggest deciding factors. While fixed deposits continue to offer stability and predictable income, many investors are now exploring bond investments in India for potentially higher yields and better post-tax returns.

In 2026, FD interest rates in India are expected to remain relatively stable, with leading banks and NBFCs offering returns in the range of approximately 6.5% to 8.5% annually depending on tenure and issuer profile. However, several high return bonds in India, particularly AAA rated bonds and quality corporate bonds, may offer yields ranging between 8% and 10% or more, depending on market conditions and credit risk.

The fixed deposit vs bonds returns comparison becomes more relevant when post-tax earnings and inflation-adjusted returns are considered. Since FD interest is fully taxable as per the investor’s income slab, actual returns may reduce significantly for individuals in higher tax brackets.

5 Lakh Investment Comparison

| Particulars | Fixed Deposit | AAA Rated Bonds |

| Investment Amount | ₹5,00,000 | ₹5,00,000 |

| Indicative Annual Return | 7.25% | 9% |

| Annual Interest Earned | ₹36,250 | ₹45,000 |

| Tax Impact* | Higher slab-based taxation | May vary depending on bond structure |

| Approximate Post-Tax Return | Lower effective yield | Potentially better post-tax income |

Another important factor is inflation. If inflation remains elevated, lower-yielding fixed deposits may generate limited real returns after taxes. In contrast, selected bond investments may offer better inflation-adjusted income potential, especially for long-term investors seeking stable cash flows.

That said, higher returns in bonds are not guaranteed and may involve risks linked to issuer quality, liquidity, and interest rate movements. Investors should evaluate credit ratings, issuer fundamentals, and investment horizon before making a decision.

For investors focused purely on safety and simplicity, FDs may still remain attractive. However, those seeking potentially higher income and portfolio diversification are increasingly considering corporate bonds vs FD investments as part of their fixed income allocation in 2026.

Are Bonds Safer Than Fixed Deposits?

Safety is often the first concern for investors comparing corporate bonds vs FD investments. While both are considered relatively stable fixed income investments in India, the level of safety depends on multiple factors such as issuer quality, credit ratings, insurance coverage, and investment tenure.

Fixed deposits are generally viewed as one of the most familiar safe investments in India because they offer fixed returns and lower volatility. However, bonds — especially AAA rated bonds in India — can also be considered relatively low risk investment options when issued by financially strong entities.

Understanding Credit Ratings

One of the key safety indicators in bond investing is the credit rating assigned by rating agencies. These ratings reflect the issuer’s ability to repay interest and principal obligations on time.

AAA - Highest level of safety and strongest repayment capacity

AA - High safety with slightly higher risk than AAA

A and Below - Higher risk with lower credit quality

AAA rated bonds are typically issued by well-established corporations, financial institutions, or government-backed entities. Although no investment is entirely risk-free, higher-rated bonds generally carry lower default risk compared to lower-rated debt instruments.

FD Insurance Limits in India

Bank fixed deposits in India are covered under DICGC insurance up to ₹5 lakh per depositor per bank, including principal and interest. This provides an additional layer of protection for small depositors. However, amounts exceeding this limit may not be fully protected in case of bank failure.

For example, an investor holding a long-term bond may see temporary price fluctuations if interest rates rise. However, if the issuer remains financially stable and the bond is held till maturity, scheduled interest payments may continue as per the bond terms.

Rather than choosing one product over the other, many investors diversify between bonds and FDs to balance stability, liquidity, and return potential in their portfolios.

Bonds vs FD Taxation in India 2026

Taxation plays a major role in determining actual investment returns, especially for investors comparing bonds vs fixed deposits India 2026. While both options generate fixed income, the way returns are taxed can significantly impact post-tax earnings, particularly for individuals in higher income tax brackets.

Understanding bond vs FD taxation in India is essential before choosing between traditional fixed deposits and bond investments in India.

How FD Interest is Taxed

Interest earned from fixed deposits is fully taxable as “Income from Other Sources” and is added to the investor’s total annual income. The tax liability depends on the individual’s applicable income tax slab.

Banks may also deduct TDS (Tax Deducted at Source) once the annual interest earned crosses the prescribed threshold under prevailing tax rules.

For example, if an investor in the 30% tax bracket earns ₹50,000 annually from FDs, the effective post-tax income may reduce considerably after taxes.

How Bond Income is Taxed

Bond taxation depends on the type of bond, holding period, and nature of income earned. Interest received from taxable corporate bonds is generally taxed according to the investor’s income slab, similar to FDs.

However, certain bond categories may offer better tax efficiency. Additionally, if bonds are sold before maturity, capital gains taxation may apply depending on the holding period and applicable tax regulations.

In some cases, listed bonds held for longer durations may receive more favorable tax treatment compared to traditional FD interest income. This is one reason why many investors evaluating corporate bonds vs FD investments also consider post-tax returns rather than only headline yields.

Which Investment is More Tax Efficient?

For investors in lower tax brackets, the difference in taxation may be less significant. However, high-income investors often compare fixed deposit vs bonds returns on a post-tax basis, where selected bond investments may offer relatively better tax efficiency and higher effective yields.

Since taxation rules may change over time, investors should evaluate investment structures carefully and consult qualified tax professionals before making financial decisions.

Who Should Invest in Bonds?

Not every investor has the same financial goals, and that is exactly why bond investments in India are gaining attention in 2026. Bonds are no longer viewed only as institutional products. Today, retail investors are increasingly exploring corporate bonds and AAA rated bonds as part of a balanced fixed income investment strategy.

For investors looking beyond traditional fixed deposits, bonds can offer a combination of predictable income, diversification, and potentially higher yields. However, the suitability of bonds depends on factors such as risk appetite, investment horizon, and income requirements.

For example, a retiree looking for regular monthly or quarterly income may consider investing in carefully selected AAA rated bonds in India to generate relatively predictable cash flows while reducing excessive exposure to equity market fluctuations.

Similarly, investors evaluating where to invest in 2026 India may use bonds as a diversification tool alongside equities, mutual funds, and fixed deposits. Diversification across asset classes can help balance risk and return over the long term.

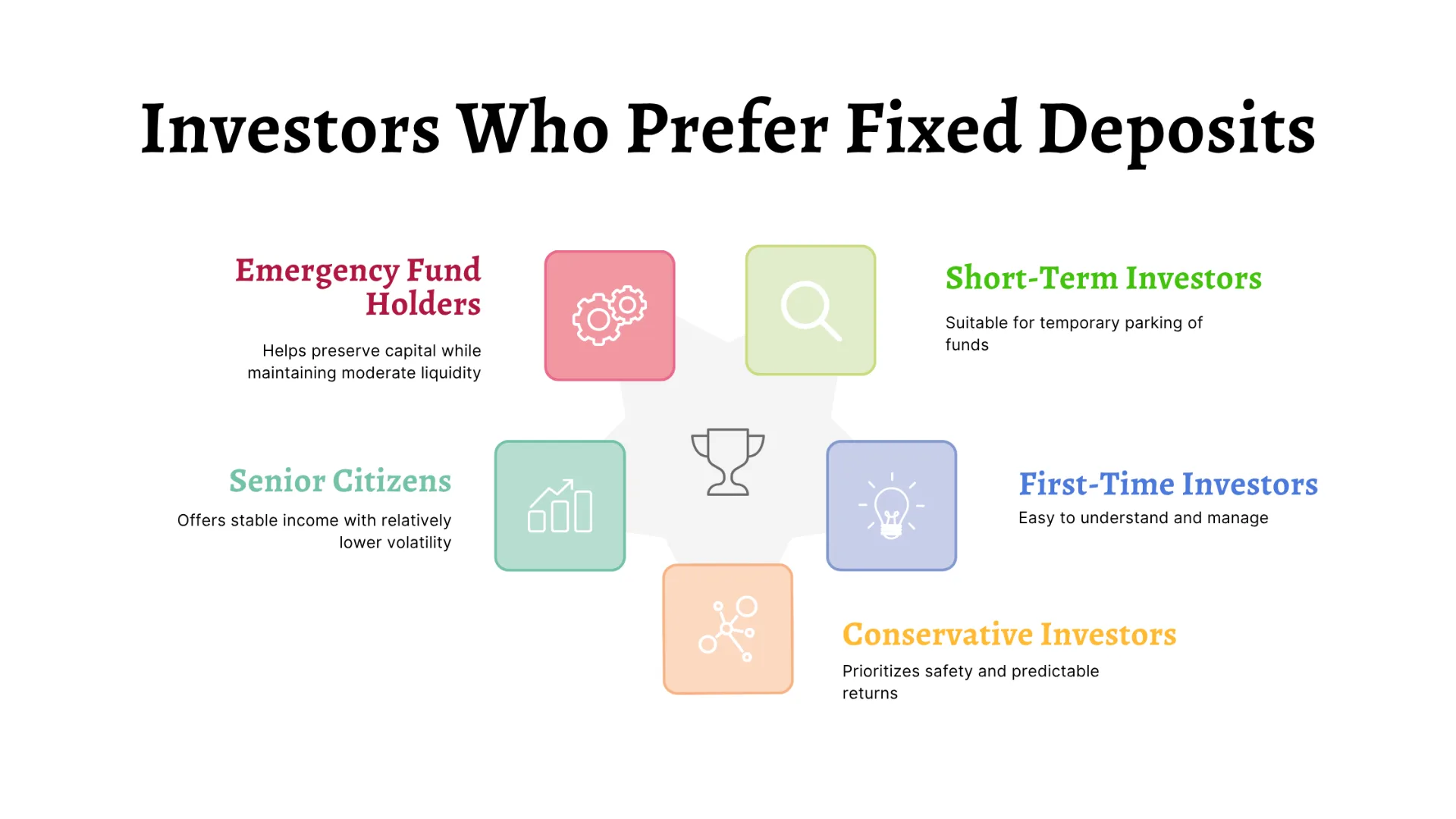

Who Should Choose Fixed Deposits?

Even as investors explore newer fixed income investments in India, fixed deposits continue to remain one of the most trusted savings options for individuals prioritizing stability and simplicity. In the ongoing bonds vs fixed deposits India 2026 discussion, FDs still hold strong relevance for investors who value capital protection over aggressive return potential.

Fixed deposits are particularly suitable for individuals who prefer predictable returns without exposure to market fluctuations. Since the interest rate is locked in at the time of investment, investors know exactly how much they are likely to receive at maturity, making financial planning easier.

One of the biggest advantages of fixed deposits is their simplicity. Unlike bonds, FDs do not require investors to evaluate credit ratings, issuer quality, or secondary market movements. This makes them particularly attractive for individuals who are new to investing or prefer straightforward financial products.

For example, an investor planning a near-term financial goal such as education expenses, travel, or emergency reserves may choose a short-duration FD to avoid market-linked uncertainties while earning fixed interest income.

Senior citizens also continue to prefer fixed deposits because many banks offer higher FD interest rates for senior investors. Regular interest payout options can help create stable cash flow for retirement planning.

Bonds vs Fixed Deposits: Which One to Prefer in 2026?

The answer to the bonds vs fixed deposits India 2026 debate depends less on which product is “better” and more on what the investor is trying to achieve. In 2026, Indian investors are balancing safety, returns, liquidity, and tax efficiency more carefully than ever before. As a result, both bonds and fixed deposits continue to play important roles in fixed income portfolios.

Fixed deposits remain a preferred choice for investors who value certainty and simplicity. Bonds, especially AAA rated bonds and high-quality corporate bonds, are increasingly attracting investors looking for potentially higher returns and better diversification.

For example, an investor nearing retirement may choose fixed deposits for stability and monthly cash flow needs, while allocating a portion of their portfolio to carefully selected bond investments in India for potentially higher income generation.

Similarly, younger investors with a moderate risk appetite may use corporate bonds vs FD strategies to diversify beyond traditional savings products while maintaining relatively stable fixed income exposure.

When Bonds May Be More Suitable

Bonds may work better for investors who:

- are comfortable evaluating credit quality

- seek potentially better post-tax returns

- want portfolio diversification

- are investing with medium to long-term goals

- can tolerate limited market-linked fluctuations

When Fixed Deposits May Be More Suitable

FDs may be ideal for investors who:

- prioritize capital protection

- prefer guaranteed returns

- have short investment horizons

- want a simple investment product

- do not want exposure to market risks

Rather than treating it as a direct competition between fixed deposit vs bonds returns, many financial experts suggest combining both products strategically. A balanced allocation between FDs and high-quality bonds can help investors create stable income while improving overall portfolio efficiency.

In 2026, the smarter approach may not be choosing bonds or fixed deposits exclusively — but understanding how each investment fits into your broader financial goals and risk profile.

Wrapping Up

Choosing between bonds and fixed deposits in India in 2026 ultimately comes down to your financial goals, risk appetite, liquidity needs, and return expectations. While fixed deposits continue to offer stability, predictable income, and simplicity, bonds are increasingly becoming a preferred choice for investors looking for potentially higher yields, portfolio diversification, and better post-tax return opportunities.

The bonds vs fixed deposits India 2026 comparison is no longer just about safety versus returns. Investors today are also considering inflation impact, taxation, flexibility, and long-term wealth preservation while selecting fixed income investments in India.

Instead of viewing corporate bonds vs FD investments as competing products, many investors are now using both strategically within the same portfolio. Fixed deposits can provide stability and emergency liquidity, while bonds may enhance overall yield potential and income generation.

As interest rates and market conditions evolve in 2026, building a balanced fixed income portfolio becomes increasingly important. Investors should evaluate factors such as credit quality, tenure, taxation, and financial objectives before making investment decisions.

A well-planned combination of bonds and fixed deposits may help investors create a more stable, diversified, and goal-oriented investment strategy over the long term.