Bonds for Senior Citizens: Income, Risk and Liquidity

Bonds for Senior Citizens: Income, Risk and Liquidity

Bonds for senior citizens should be evaluated differently from bonds for a 35-year-old salaried investor.

The question is not only: "What yield does this bond offer?"

A better question is: "Will this investment support income needs without creating avoidable risk or liquidity pressure?"

For many senior citizens, fixed-income investing has three jobs. It may need to provide scheduled cash flow. It may need to reduce exposure to equity-market volatility. It may also need to leave enough money accessible for healthcare, household expenses, and family requirements.

Bonds can play a role in that plan. But they are not one uniform product. A Government of India security, an RBI Floating Rate Savings Bond, a tax-free PSU bond, and a listed corporate bond do not carry the same risk, liquidity, tax treatment, or exit route.

This guide explains how senior citizens can think about bonds through three lenses: income, risk, and liquidity.

Bonds for Senior Citizens: The Short Answer

There is no single formal product category called "senior citizen bonds" in India.

The phrase usually refers to bonds that senior citizens may consider for retirement income or fixed-income allocation. These may include government securities, RBI Floating Rate Savings Bonds, tax-free bonds, listed corporate bonds, public-sector bonds, and other debt securities.

Some of these instruments carry sovereign credit support. Some depend on a corporate issuer's ability to pay. Some may be listed and tradable. Others may have lock-in conditions or limited exit options.

This is why senior citizens should not evaluate bonds only by coupon or yield. Coupon tells you the interest rate stated on the bond. Yield to maturity, or YTM, estimates the annualised return if the bond is bought at a given price and held until maturity, assuming payments happen as scheduled. Neither number, by itself, tells you whether the bond fits your income calendar, risk tolerance, tax position, or liquidity needs.

A sensible bond allocation for a retired investor starts with practical questions:

- How much monthly or quarterly income is needed after tax?

- How much money should remain instantly accessible?

- Can the investor hold the bond until maturity?

- What credit risk is acceptable?

- Is the investor comfortable reviewing offer documents and holding securities in demat form?

Investors can use Equirize to compare listed bonds on Equirize, review key terms, and evaluate whether a bond fits their cash-flow plan. Equirize does not provide investment advice.

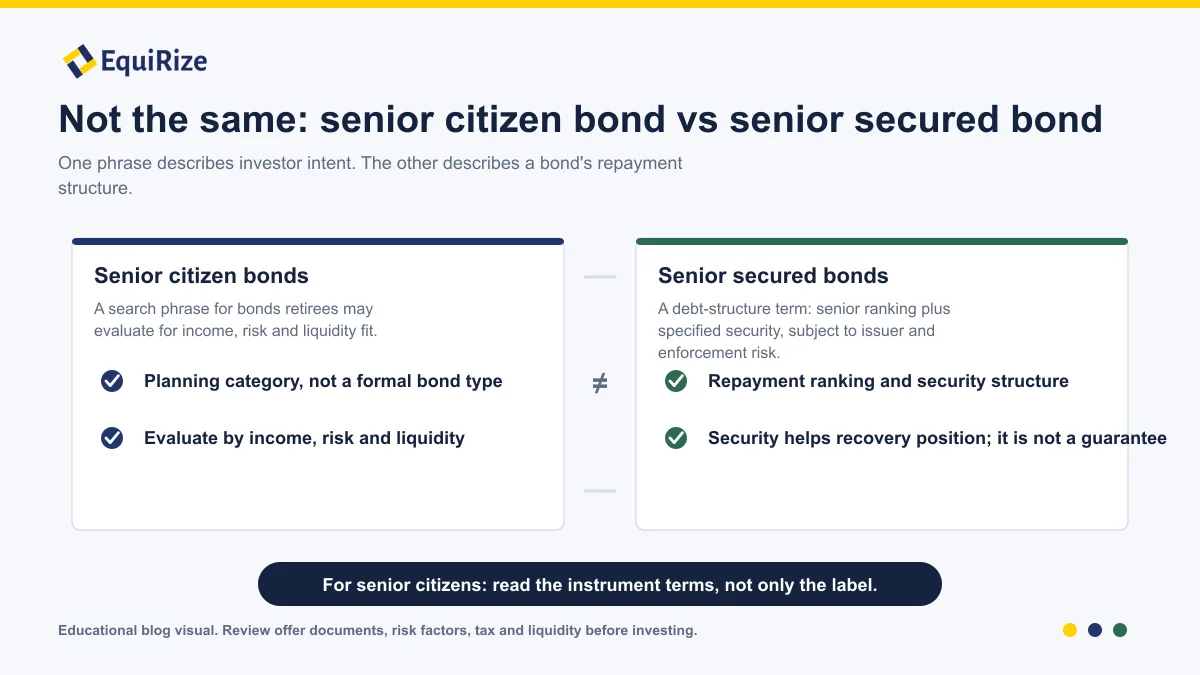

Are Senior Citizen Bonds a Separate Product?

"Senior citizen bond" is a useful search phrase, but it can be misleading.

In India, some investment products are specifically designed for senior citizens. The Senior Citizens Savings Scheme (SCSS), for example, is a government small-savings scheme for eligible senior citizens. Bonds are different. Most bonds are issued by governments, public-sector entities, financial institutions, NBFCs, municipalities, or companies for a wider investor base.

A senior citizen may choose a bond because its cash-flow pattern, credit profile, tenure, or tax treatment fits their plan. That does not make the bond a senior-citizen-specific product.

There is another phrase that needs care: "senior secured bond."

In a bond context, "senior secured" is not about the investor's age. It describes the bond's position in the issuer's repayment structure and the presence of security or collateral. A senior secured bond may have priority over subordinated debt in certain recovery situations, and it may be backed by specified assets. That still does not remove issuer risk, valuation risk, enforcement risk, or liquidity risk.

For senior citizens, the practical task is to understand what kind of bond is being considered:

| Bond / product type | What it generally means | Senior-citizen relevance |

| Government securities | Debt issued by the Government of India or state governments | Sovereign or state-linked credit profile; market price can still move |

| RBI Floating Rate Savings Bonds | Government of India taxable bonds with floating coupon linked to the NSC rate plus a spread | Semi-annual income, 7-year tenure, specific premature-redemption rules |

| Tax-free bonds | Listed bonds where interest may be exempt from tax under relevant provisions | Useful to evaluate for higher tax slabs, but liquidity and price matter |

| Listed corporate bonds | Debt issued by companies and listed on exchanges | Scheduled coupons, issuer credit risk, secondary-market liquidity risk |

| Senior secured corporate bonds | Corporate bonds with senior ranking and identified security | Security helps recovery position but does not make the bond risk-free |

| Bank / corporate FDs | Deposits, not listed bonds | Useful comparison point for income, tax, liquidity, and credit support |

The label matters less than the terms. Read the instrument.

Income: What Kind of Cash Flow Do Bonds Provide?

Bonds can help create scheduled cash flows because many of them have defined coupon dates and maturity dates. That visibility is useful for senior citizens who plan expenses around pensions, rent, annuities, FDs, dividends, or family support.

But a coupon schedule is not the same as certainty. Corporate bond payments depend on the issuer's ability to meet obligations. If a bond is sold before maturity, the investor's realized price can differ from the expected maturity value.

Monthly, quarterly and semi-annual payouts

Some bonds pay interest monthly. Others pay quarterly, semi-annually, annually, or only at maturity.

This matters because many retirement expenses are monthly, while several fixed-income instruments pay quarterly or semi-annually. SCSS pays interest quarterly. RBI Floating Rate Savings Bonds pay interest semi-annually. Many listed corporate bonds may pay monthly or quarterly coupons, depending on the issue terms.

Instead of asking whether a bond "gives income", ask when the income is scheduled to arrive.

For example, a retired investor with monthly household expenses may still use quarterly coupon bonds if they keep a bank buffer and plan withdrawals. Another investor may prefer monthly payout bonds but should not ignore issuer risk simply because the payout frequency looks convenient.

For a deeper cash-flow framework, see Equirize's guide to monthly income from bonds.

Coupon rate vs yield to maturity

Coupon and YTM answer different questions.

The coupon rate is the stated annual interest rate on the bond's face value. YTM estimates the annualised return from the bond if bought at the current price and held until maturity, assuming scheduled payments happen.

For senior citizens, coupon frequency affects cash-flow timing. YTM affects comparison.

A bond with a higher YTM may not be a better fit if it has a longer maturity, lower liquidity, a lower credit rating, a call option, or a coupon schedule that does not match the investor's expenses. Conversely, a bond with a lower YTM may still fit a specific income plan if the credit profile, maturity, and liquidity terms are more suitable.

For the mechanics, read Equirize's guide to yield to maturity.

Matching bond cash flows to retirement expenses

A retirement cash-flow plan should start with expenses, not products.

Separate expenses into three buckets:

| Expense bucket | Examples | Bond-planning implication |

| Monthly essentials | Groceries, utilities, medicines, staff salaries | Keep a liquid bank buffer; use bond coupons only as one support |

| Scheduled obligations | Insurance premiums, maintenance, school support for family, charitable commitments | Match coupon or maturity dates where possible |

| Unplanned needs | Healthcare, travel for family support, home repair | Do not lock this money into illiquid long-tenure instruments |

This distinction is important. Bonds may be useful for scheduled income, but emergency liquidity should usually sit outside long-tenure bonds.

Risk: What Can Go Wrong Even in Fixed Income?

Fixed income does not mean fixed outcome.

A bond may have a fixed coupon, a maturity date, and a stated payment schedule. The investor still faces risks. For senior citizens, these risks need to be understood before the money is committed, because recovery from an avoidable mistake may be harder after retirement than during earning years.

Credit rating is a starting point, not a guarantee

A credit rating is an opinion from a credit rating agency on the issuer's or instrument's ability to meet debt obligations. It helps investors compare credit quality. It does not guarantee repayment.

Higher-rated bonds are generally assessed as carrying lower credit risk within the rating agency's scale. But even highly rated instruments should be reviewed for rating outlook, rating watch, issuer financials, sector exposure, maturity, and security structure.

Do not stop at the symbol. Read the rating rationale.

If comparing rating buckets, Equirize's guide to AAA vs AA bonds explains why the gap between ratings affects risk, yield, and due diligence.

Secured does not mean risk-free

A secured bond is backed by identified assets or receivables. This can improve the investor's recovery position relative to unsecured debt, depending on the structure.

But security does not remove risk.

The value of the security can change. Enforcement can take time. The asset may be difficult to sell. Other creditors may have competing claims. Documentation quality matters.

For a senior citizen, "secured" should trigger further review, not instant comfort. Check the security cover, debenture trustee details, charge creation, asset quality, and whether the instrument is senior or subordinated.

Interest-rate risk if you sell before maturity

Bond prices move when market yields change.

If interest rates rise after an investor buys a fixed-coupon bond, the market price of that bond may fall. If the investor holds until maturity and the issuer pays as scheduled, price fluctuation may matter less. If the investor needs to sell early, it can matter a lot.

This is interest-rate risk. It is especially relevant for long-tenure bonds.

For senior citizens, the implication is simple: do not put near-term expense money into a bond that may need to be sold in unfavorable market conditions.

Concentration risk in retirement portfolios

Concentration risk often hides behind yield.

If too much money is placed with one issuer, one sector, one rating category, or one maturity year, a single adverse event can affect the retirement plan more than expected.

This is why a bond portfolio should be reviewed at the household level. Include FDs, SCSS, annuities, pensions, mutual funds, bank balances, insurance needs, and family obligations in the same view. A bond that looks reasonable alone may become too large when seen as part of the full portfolio.

Tax risk and post-tax income

Interest income from many bonds is taxable according to the investor's applicable tax slab. Tax-free bonds are different, but their market price and yield should still be reviewed carefully.

Senior citizens should compare post-tax cash flow, not only pre-tax coupon or YTM. TDS, Form 121 eligibility, capital gains treatment, and tax regime selection can all affect the final result.

Tax treatment depends on individual circumstances and may change. Please consult a qualified tax advisor.

Liquidity: Can Senior Citizens Exit Bonds Before Maturity?

Liquidity is not a small detail for senior citizens. It is central to the decision.

A bond may be listed, but listed does not always mean easily sold at the desired price. A government small-savings product may have sovereign credit support, but it may carry lock-in or premature-withdrawal conditions. A corporate bond may show a useful YTM, but the secondary market may have limited buyers.

The right question is not "Can this be sold?" It is: "Can this be sold when I need money, at a price I can accept?"

Listed corporate bonds and secondary-market liquidity

Listed corporate bonds can be bought or sold on recognized exchanges or through exchange-linked platforms, subject to available counterparties and market conditions.

The exit price depends on factors such as issuer credit quality, remaining maturity, coupon, market yields, issue size, traded volume, and investor demand. A bond with low trading activity may require the seller to accept a wider bid-ask spread.

For senior citizens, early exit should be treated as possible but not assured. If there is a known expense within the next few months, that money should generally remain in more liquid instruments.

RBI FRSB and scheme-specific lock-ins

RBI Floating Rate Savings Bonds, 2020 (Taxable) have a 7-year maturity and semi-annual interest payments. The coupon is linked to the prevailing National Savings Certificate rate with a 0.35% spread, and the rate resets half-yearly. Premature redemption is available only for specified categories of senior citizens, subject to scheme rules. The bonds are not tradable in the secondary market.

That structure can suit some investors and not others. The credit profile is linked to the Government of India, but liquidity is more constrained than an instrument that can be actively sold in a secondary market.

Always check the current operational guidelines before investing.

Why a healthcare and emergency buffer should sit outside bonds

Senior citizens should separate investment income from emergency liquidity.

Healthcare expenses do not wait for a coupon date. Nor do sudden family needs, relocation expenses, or home repairs. A practical plan usually keeps a cash or near-cash reserve outside long-tenure bonds.

The size of this reserve depends on the household. A retired couple with health insurance, pension income, adult children nearby, and low rent may need a different buffer from someone living alone with higher medical exposure.

The point is not to avoid bonds. The point is to avoid being forced to sell them at the wrong time.

Liquidity questions to ask before buying

Before investing, ask:

- Is the bond listed?

- How often does it trade?

- What is the likely exit route?

- Is there a lock-in or call option?

- What happens if I need money before maturity?

- Are there penalties, price risks, or non-transferability conditions?

- Is the emergency fund separate from this investment?

If the answer is unclear, pause before investing.

Bonds vs SCSS vs FDs for Senior Citizens

Senior citizens often compare bonds with SCSS and FDs because all three can sit inside a fixed-income plan. They are not interchangeable.

As of the latest National Savings Institute rate table accessed on July 16, 2026, the 5-year Senior Citizens Savings Scheme rate is listed at 8.2% and the 5-year Monthly Income Account rate at 7.4%. These rates are reviewed by the government and can change over time. Investors should verify the current rate before making decisions.

The table below is a decision aid, not a recommendation.

| Intrument | Income pattern | Credit support / risk | Liquidity | Tax treatment | Watchout |

| SCSS | Quarterly interest | Government small-savings scheme | 5-year tenure; premature closure subject to rules | Interest taxable; Section 80C treatment may apply to eligible investment | Investment limit, eligibility, tax, and early-closure rules |

| RBI Floating Rate Savings Bonds | Semi-annual interest | Government of India taxable bond | 7-year maturity; not tradable; premature redemption only for specified senior categories | Interest taxable | Coupon resets; no cumulative option; limited liquidity |

| Tax-free bonds | Usually periodic interest depending on issue terms | Depends on issuer; many historical issuers are public-sector entities | Listed, but trading liquidity varies | Interest may be tax-exempt under relevant provisions | Market price, yield, long tenure, and liquidity |

| Listed corporate bonds | Monthly, quarterly, semi-annual, annual, or maturity payout depending on issue | Issuer credit risk; rating and structure matter | May be sold in secondary market if there is demand | Interest generally taxable; capital gains depend on facts | Default risk, downgrade risk, liquidity risk, concentration |

| Bank FDs | Interest monthly, quarterly, cumulative, or at maturity | Bank credit risk; DICGC insurance up to applicable limit per depositor per bank | Premature withdrawal usually allowed with terms | Interest taxable | Reinvestment risk, tax, premature-withdrawal penalty |

| Corporate / NBFC FDs | Interest based on issuer terms | Issuer credit risk; not DICGC-insured | Premature withdrawal depends on issuer terms | Interest taxable | Credit risk, no DICGC insurance, TDS |

For many senior citizens, the answer may not be one instrument. It may be a layered structure:

- A bank balance or liquid reserve for emergencies.

- SCSS or similar schemes for eligible government-backed income.

- FDs for defined liquidity and tenure needs.

- Listed bonds for additional fixed-income exposure, after issuer and liquidity review.

- Tax-free bonds where post-tax yield and liquidity make sense.

The exact mix depends on the investor's situation. The article does not provide investment advice or a model allocation.

How EquiRize Fits Into the Evaluation Process

Equirize is a SEBI-registered Online Bond Platform Provider (OBPP) and a stock broker in the debt segment of BSE and NSE.

SEBI formalised the registration and regulatory framework for Online Bond Platform Providers through its November 14, 2022 circular. The framework was introduced to bring online bond platforms within a clearer regulatory perimeter, with requirements around registration, disclosures, operations, advertisements, and investor grievance redressal.

For investors, the useful role of an OBPP is information access and execution support. It should not be confused with investment advice.

On Equirize, investors can review listed bond opportunities, compare issue terms, see payout frequency, check rating details, and review documents before making their own decision. This can help senior citizens and their families ask better questions:

- What is the issuer?

- What is the rating and who assigned it?

- What is the maturity date?

- What is the payout frequency?

- What is the YTM and how does it differ from coupon?

- Is the bond secured or unsecured?

- What risks are disclosed?

- Can I hold this until maturity?

The platform can make information easier to access. The decision still needs suitability, tax, and liquidity judgement.

Final Take: Income is Useful, Liquidity is Essential

Bonds for senior citizens should be evaluated with a retirement lens.

Income matters, but it is only one part of the decision. A scheduled coupon is useful only if the issuer pays as expected, the post-tax amount fits the household plan, and the investor is not forced to sell at an unfavorable time.

Risk matters too. A credit rating, secured structure, or familiar issuer name can help with evaluation, but none of these should replace reading the offer document and understanding the instrument.

Liquidity may matter most of all. Senior citizens should keep emergency and healthcare money outside long-tenure or hard-to-exit instruments. Bonds can support a retirement income plan, but they should not carry the entire burden of day-to-day liquidity.

The better approach is calm and practical: map expenses, preserve accessible reserves, compare post-tax income, check credit and liquidity risk, diversify carefully, and invest only in instruments whose terms are clear.