What is a Bond IPO in India - A Retail Investor's Guide

A bond IPO in India is a public issue of debt securities, usually structured as a non-convertible debenture or NCD public issue. Instead of buying shares in a company, you lend money to an issuer for a defined coupon, tenure, repayment schedule, and set of risks.

The term "bond IPO" is market shorthand. The regulatory language is usually "public issue of NCDs" or "public issue of debt securities". For retail investors, the important point is simple: these issues are part of the regulated securities market, and applications can be made through brokers, banks, exchange platforms, and eligible SEBI-registered online bond platform providers.

This guide explains what a bond IPO is, how it differs from an equity IPO, who can invest, how allotment works, what risks to check, and how to apply through EquiRize.

What is a Bond IPO? NCD Public Issue Explained

A bond IPO is a public issue through which a company, NBFC, financial institution, or eligible issuer raises debt capital from investors. In India, most retail-facing bond IPOs are issued as NCDs, or non-convertible debentures.

"Non-convertible" means the debenture does not convert into equity shares. You do not become a shareholder. You become a lender to the issuer and receive interest as per the terms of the issue, subject to issuer performance.

Bond IPO India searches often use terms like NCD IPO India, NCD public issue, non-convertible debenture public issue, and public bond issue interchangeably.

Every public debt issue should be read through its offer document. It explains the issuer, objects of the issue, coupon options, tenure, credit rating, security cover, debenture trustee, investor categories, allotment basis, taxation notes, and risk factors.

Many NCD public issues use first-come-first-serve allotment within investor categories. That is why investors often apply early when an issue has an attractive rating, yield, and tenure combination.

Bond IPO vs Equity IPO: Key Differences

Bond IPOs and equity IPOs both happen in the primary market, but the instrument, return expectation, risk profile, and allotment logic are different.

| Factor | Bond IPO/NCD public issue | Equity IPO |

|---|---|---|

| What you buy | Debt security issued by the borrower | Equity shares of the company |

| Investor role | Lender | Shareholder / part owner |

| Return source | Coupon, redemption amount, and market price if sold | Share price movement and dividends, if any |

| Upside | Usually limited to stated coupon and price movement | Potentially high, but uncertain |

| Main risk | Credit risk, liquidity risk, interest-rate risk | Business risk, valuation risk, market risk |

| Allotment | Often first-come-first-serve within categories, subject to issue terms | Usually lottery or proportionate basis depending on category and demand |

| Holding format | Demat | Demat |

| Tax treatment | Interest taxed as income; capital gains may apply on sale | Capital gains and dividend tax rules apply |

In short, an equity IPO is about ownership and growth; a bond IPO is about credit, cashflows, and repayment capacity.

Who Can Invest in a Bond IPO?

Bond IPO eligibility depends on the offer document. Most public NCD issues define investor categories and quotas.

Retail Individual Investors

Retail Individual Investors generally include resident individuals and Hindu Undivided Families applying up to the retail limit specified in the issue. In many public NCD issues, the retail threshold is up to Rs. 10 lakh, but investors should verify the exact limit.

High Net-worth Individuals

HNIs or non-institutional investors typically apply above the retail threshold. Their allotment quota and oversubscription treatment can differ from the retail category.

Qualified Institutional Buyers

QIBs include eligible institutional investors such as mutual funds, banks, insurance companies, and other regulated institutions.

NRIs and Other Eligible Investors

Can NRIs invest in a bond IPO in India? Sometimes yes, but not always. NRI eligibility depends on RBI conditions, issuer terms, account type, repatriation status, and the offer document. Some NCD public issues allow NRI participation; others restrict it.

HUFs, trusts, companies, and other entities may also be eligible depending on the issue.

How Does the Bond IPO Application Process Work?

The process is straightforward, but investors should slow down at the document-review stage.

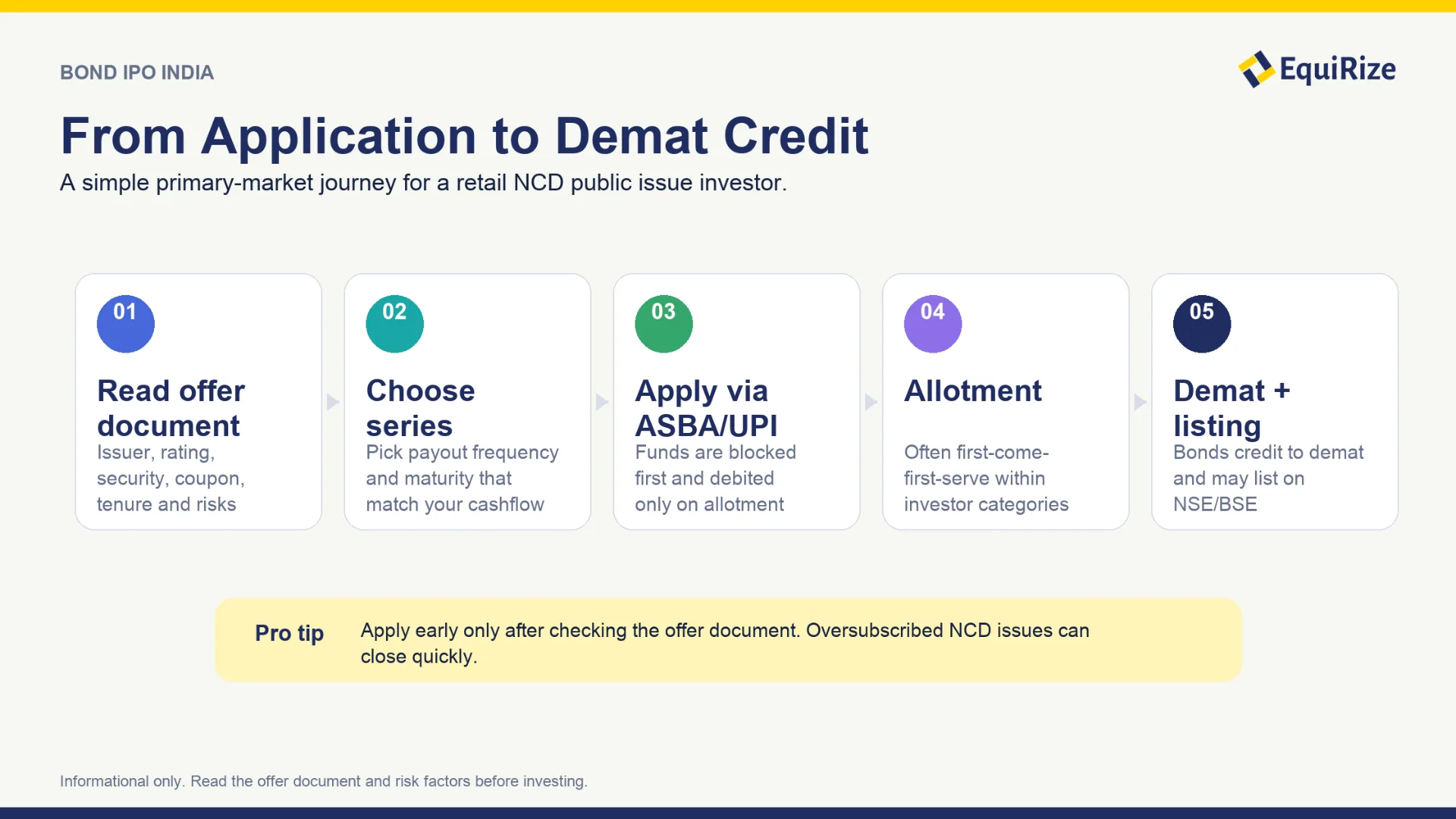

1. Check the Offer Document

Start with the offer document, shelf prospectus, tranche prospectus, or term sheet, as applicable. Review issuer profile, use of funds, coupon options, tenure, rating, security status, debenture trustee, minimum application, redemption schedule, and risk factors.

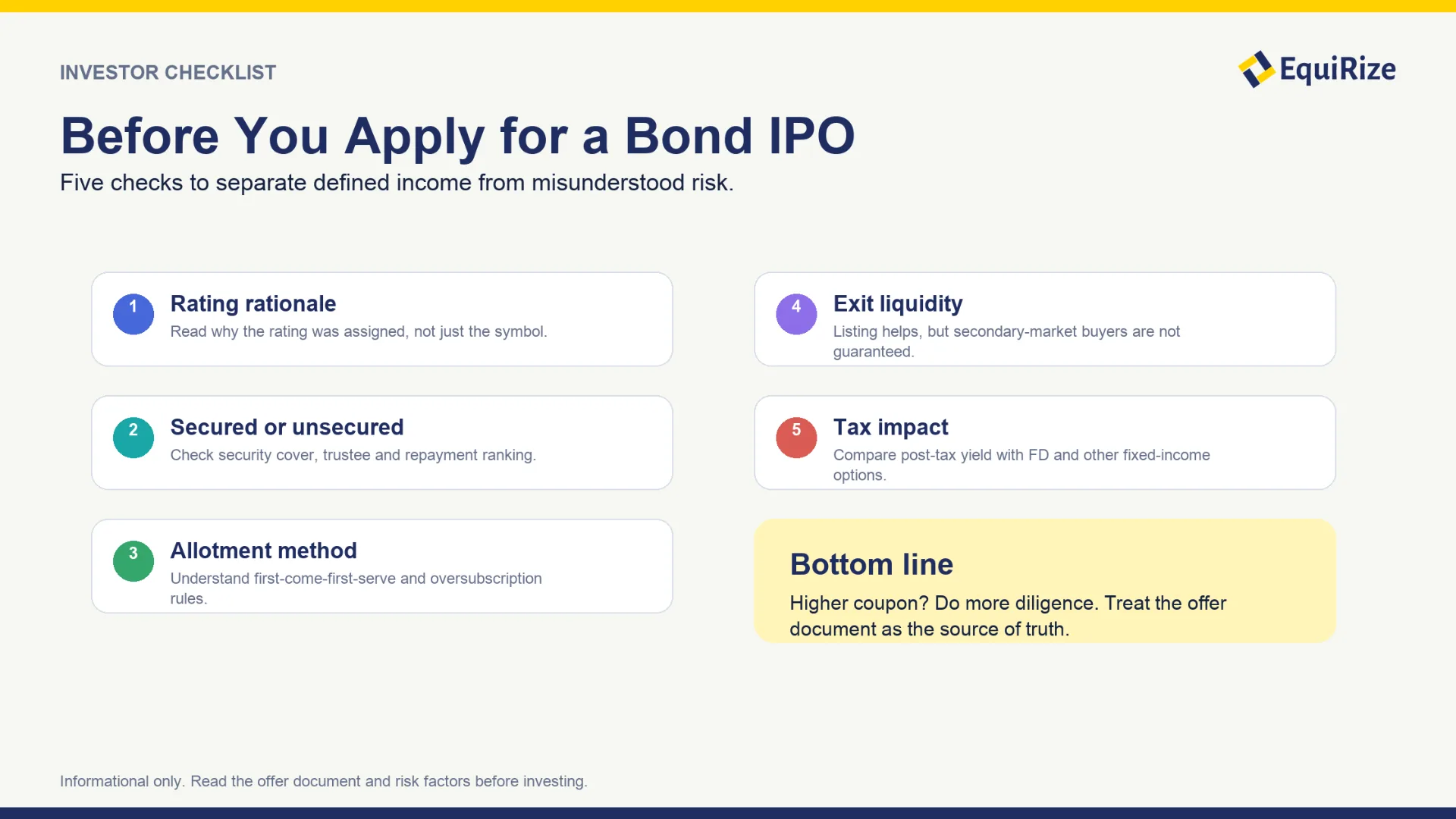

Pay special attention to whether the issue is secured or unsecured and whether the rating outlook is stable, positive, or negative.

2. Select a Regulated Route

You can apply through permitted channels such as brokers, banking interfaces, exchange-supported platforms, and eligible online bond platforms. SEBI's OBPP framework requires online bond platform providers dealing in listed debt securities to operate within a regulated structure.

Using a regulated platform does not make the issuer risk-free, but it improves process transparency and accountability.

3. Choose the Right Series

Many NCD public issues offer multiple series. Each series can have a different tenure, coupon rate, payout frequency, cumulative option, or redemption structure.

Choose based on your cashflow need. A retiree may prefer regular coupon payout. A salaried investor matching a future goal may prefer a maturity aligned with that goal. Do not pick only the highest coupon without checking tenure and credit risk.

4. Apply through ASBA or UPI Where Available

Public issue applications are commonly made through ASBA, where funds are blocked in your bank account and debited only if you receive allotment. UPI may be available depending on the issue and platform flow.

5. Apply Early if the Issue is Attractive

Many bond IPO allotments use first-come-first-serve logic based on the upload of valid applications on the exchange bidding platform. If an issue is oversubscribed, applying late can reduce allotment probability.

If you have read the documents and decided the issue fits your portfolio, avoid waiting until the final day. Popular issues can close early or become oversubscribed quickly.

6. Receive Bonds in Demat After Allotment

After allotment and listing, the bonds are credited to your demat account. Listed NCDs may be available for secondary-market sale on NSE or BSE, subject to liquidity.

How is Bond IPO Allotment Done?

Bond IPO allotment is governed by the offer document, investor category allocation, issue demand, and exchange upload records. For many NCD public issues, allotment within each category is made on a first-come-first-serve basis, based on when valid bids are uploaded. If the issue is oversubscribed, allotment may become proportionate or follow the method stated in the prospectus.

SEBI's corporate bond FAQ states that minimum subscription for a public issue should not be less than 75% of the base issue size or as may be specified. If the minimum subscription is not met, the issue may not proceed as planned and application money is unblocked or refunded according to the offer terms.

How to Check NCD Allotment Status on BSE

You can check application status on the BSE status page where available:

- Visit BSE's "Status of Issue Application" page.

- Select issue type as "Debt".

- Choose the relevant issue name if it appears in the list.

- Enter PAN or application number as required.

- Submit to view the status.

You may also receive updates from the registrar, broker, platform, exchange, depository, SMS, or email.

Secured vs Unsecured NCDs: What is the Difference?

Secured NCDs are backed by identified assets or security cover created in favour of debenture holders through a debenture trustee. If the issuer defaults, secured debenture holders generally have a higher claim on specified secured assets than unsecured creditors, subject to the legal structure.

Unsecured NCDs do not have specific asset backing. Investors rely more directly on the issuer's creditworthiness. Some unsecured NCDs may be subordinated, which means they rank below senior debt.

Is secured vs unsecured NCD which is better? Secured is generally preferable all else being equal, but all else is rarely equal. A secured NCD from a weak issuer may still be riskier than an unsecured bond from a stronger issuer.

Use credit ratings as the first filter, not the final answer. Ratings are opinions and can change. Read the rating rationale to understand leverage, asset quality, liquidity, profitability, sector exposure, and rating sensitivities.

Bond IPO vs Fixed Deposit: Which Gives Better Returns?

Bond IPO vs FD returns comparison is useful only if you compare risk-adjusted and post-tax outcomes. An NCD may show a higher coupon or indicative yield than a fixed deposit, but it also carries credit risk, market-price risk, and liquidity risk.

| Factor | Bank fixed deposit | Bond IPO/NCD public issue |

|---|---|---|

| Return metric | Interest rate | Coupon and indicative yield |

| Return certainty | Contractual, subject to bank terms | Scheduled, subject to issuer repayment ability |

| Regulator framework | RBI-regulated bank deposit framework | SEBI-regulated securities-market issue framework |

| Deposit insurance | Eligible bank deposits covered by DICGC up to applicable limits | No DICGC deposit insurance |

| Liquidity | Premature withdrawal may be available with penalty | Sale possible after listing, but depends on market liquidity |

| Credit risk | Bank credit risk, partly mitigated by insurance limits for eligible deposits | Issuer credit and default risk |

| TDS/tax | Interest taxable; TDS rules may apply | Interest taxable; capital gains may apply if sold |

| Minimum investment | Varies by bank | Often around Rs. 10,000, but varies by issue |

If you need emergency liquidity, a bank FD may be simpler. If you can evaluate issuer risk and hold to maturity, a bond IPO may offer defined fixed-income cashflows with exchange listing.

Can You Sell a Bond IPO Before Maturity?

Yes, listed bonds or NCDs received through a public issue can generally be sold before maturity on the exchange, provided there is a buyer.

The sale price may be above or below your purchase price. If market yields rise after you buy, your bond price can fall. If the issuer's credit perception worsens, the price may fall even if broader rates are stable.

Liquidity varies sharply. A large AAA-rated PSU issue may trade more actively than a smaller NBFC issue. Some bonds show wide bid-ask spreads, so your actual exit price can differ from the theoretical price shown on a platform.

Retail investors should plan to hold bond IPO investments until maturity unless there is a clear secondary-market exit available. Treat listing as an exit option, not a guaranteed liquidity promise.

Risks of Investing in Bond IPOs

Bond IPOs can be useful fixed-income instruments, but they are not risk-free. Read these risks before applying.

Credit Risk/Default Risk

Credit risk is the risk that the issuer delays or defaults on coupon or principal payment. A higher coupon may be compensation for higher credit risk.

Liquidity Risk

After listing, you may not always find a buyer at the price you expect. Thin trading and wide spreads can make exits difficult.

Interest-rate Risk

Bond prices move inversely to market yields. If interest rates rise after allotment, the market price may fall if you sell before maturity.

Reinvestment Risk

If you receive periodic coupons, you may not be able to reinvest those coupons at the same rate.

Concentration Risk

Avoid putting too much money into one issuer, one sector, or one maturity bucket.

Important investor caution: Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities, municipal debt securities, and securitised debt instruments are subject to credit risks, market risks, liquidity risks, and default risks, including delay or default in payment. Read all offer-related documents carefully.

Recent Bond IPOs in India

This section should be updated quarterly before publishing because public issue data changes quickly.

| Issuer/Issue Example | Indicative Coupon or Yield | Tenure | Rating | Minimum Application |

|---|---|---|---|---|

| Power Finance Corporation NCD public issue, Jan 2026 | Up to 7.30% p.a. across series | 5 to 15 years | AAA ratings disclosed in issue material | Rs. 10,000 |

| Recent NBFC NCD public issue | Update from offer document | Update from offer document | Update from offer document | Usually Rs. 10,000 |

| Recent housing finance or gold loan NCD issue | Update from offer document | Update from offer document | Update from offer document | Usually Rs. 10,000 |

Do not describe these returns as guaranteed. Use "coupon", "yield", or "indicative yield" depending on the issue document.

How to Invest in Bond IPOs Through EquiRize

EquiRize helps investors access fixed-income opportunities through a regulated, demat-linked investing journey. EquiRize Securities Private Limited discloses SEBI Registration Number INZ000323730, BSE Membership No. 6914 - Debt Segment, and NSE Membership No. 90472 - Debt Segment.

To explore bond IPOs or listed bond opportunities:

- Visit the EquiRize bonds page and review available issues or listed debt opportunities.

- Complete your onboarding and KYC flow.

- Compare issuer, rating, coupon, maturity, payout frequency, minimum investment, and indicative yield.

- Read the offer document, product note, risk disclosures, and taxation notes.

- Apply through the available payment and exchange-supported process.

- Track allotment and demat credit after the issue process is completed.

EquiRize should be positioned as the access platform, not the repayment guarantor. The issuer is responsible for paying coupon and principal.

Conclusion

Bond IPOs give retail investors access to SEBI-regulated public debt issues with defined coupon terms, demat credit, and exchange listing. They can be useful for fixed-income allocation, but only when the investor understands issuer credit risk, liquidity limits, tax impact, and allotment rules. Before applying, compare the offer document, rating rationale, tenure, security status, and portfolio fit. To explore fixed-income opportunities, review live bond listings on EquiRize and invest only after reading the relevant risk disclosures.