AAA vs AA Bonds: What the Rating Difference Means

AAA vs AA Bonds: What the Rating Difference Means

AAA vs AA bonds can look similar at first glance. Both sit near the top of the credit-rating scale. Both are usually treated as high-grade debt categories. Both can appear in portfolios built for income, capital stability, or lower equity exposure.

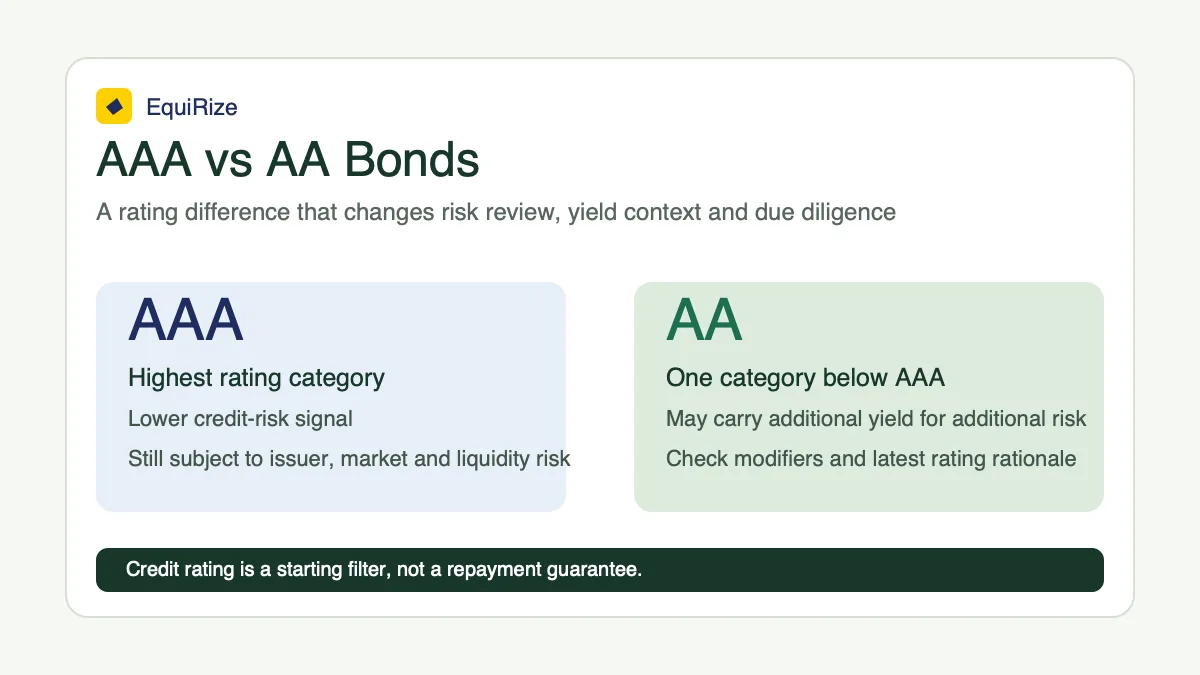

But the rating difference is not cosmetic.

AAA is the highest long-term credit-rating category. AA is one step below it, with AA+, AA and AA- showing relative position within the AA band. In practical terms, the difference affects how a rating agency views the issuer's ability to meet debt obligations, how the market may price the bond, and how much additional diligence an investor should do before subscribing.

A rating is useful. It is not a guarantee. It should help you ask better questions, not replace the work of reading the offer document, rating rationale, issuer details, maturity terms and risk factors.

AAA vs AA Bonds: Quick Comparison

The simplest way to understand AAA vs AA bonds is to separate the rating label from the investment decision.

| Factor | AAA rated bonds | AA rated bonds | What investors should check |

| Rating position | Highest long-term rating category | One category below AAA, with AA+, AA and AA- gradations | Whether the rating applies to the instrument, issuer, or a specific structure |

| Credit-risk interpretation | Lowest credit risk in the rating agency's scale | Very low credit risk, but below AAA | Rating rationale, outlook, watch status and latest review date |

| Yield behaviour | Often lower yield than lower-rated bonds, all else equal | May offer additional yield for additional credit or liquidity risk | Whether the extra yield compensates for the specific risks |

| Rating buffer | More room before falling below top-grade categories | Less buffer than AAA; AA- is closer to A than AA+ | Whether the rating trend is stable, positive, negative, or under watch |

| Liquidity and price | Still subject to market price and liquidity risk | Also subject to market price and liquidity risk, sometimes more visibly | Secondary-market depth, traded volumes and likely exit route |

| What rating does not tell you | It does not guarantee repayment or liquidity | It does not guarantee repayment or liquidity | Tenure, security cover, covenants, tax, concentration and suitability |

The key point: AAA and AA both tell you something about credit quality, but neither tells you everything about the bond.

What AAA and AA Ratings Actually Mean

Credit ratings are opinions issued by credit rating agencies on the creditworthiness of an issuer or a debt instrument. In India, credit rating agencies operate under SEBI's Credit Rating Agencies Regulations, 1999, and publish rating symbols and definitions for different categories of debt instruments. [Source: SEBI Credit Rating Agencies Regulations]

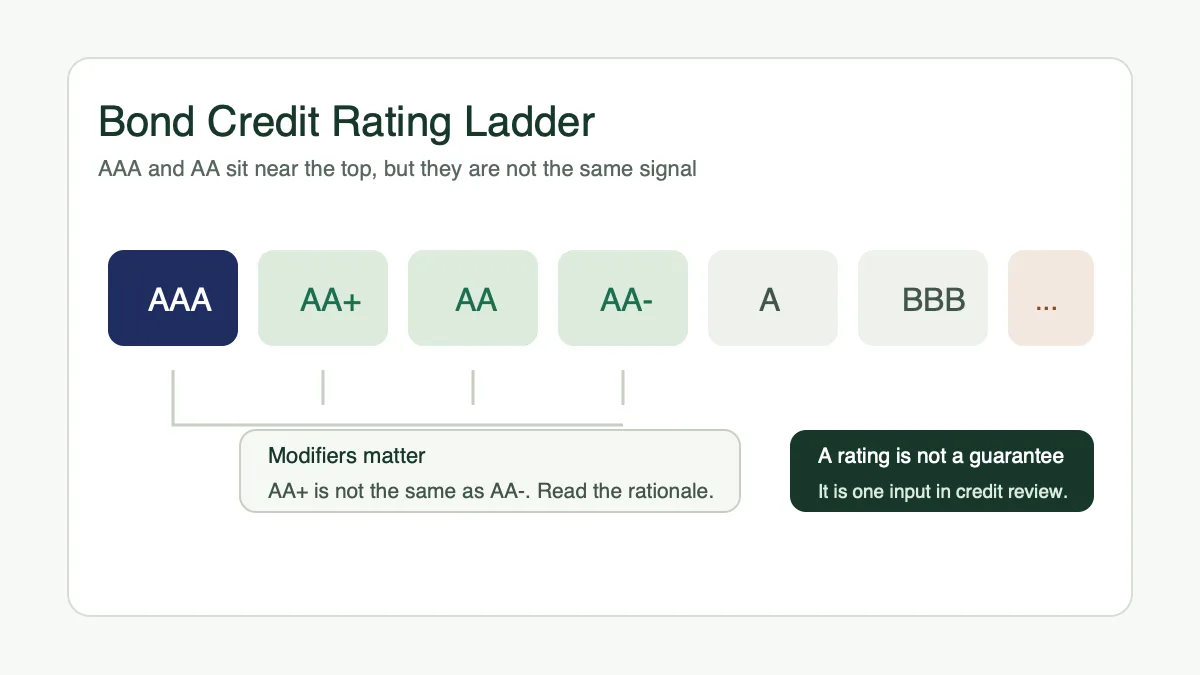

For long-term debt instruments, rating agencies generally use a scale that begins with AAA and moves downward through AA, A, BBB and below. Ratings from BBB- and above are typically referred to as investment grade, although investors should still examine the issuer and instrument in detail.

CRISIL describes AAA-rated instruments as carrying the highest degree of safety regarding timely servicing of financial obligations and the lowest credit risk. It describes AA-rated instruments as carrying a high degree of safety and very low credit risk. [Source: CRISIL credit rating scale]

CARE Ratings uses similar language in its rating definitions: AAA indicates the highest degree of safety regarding timely servicing of financial obligations, while AA indicates a high degree of safety and very low credit risk. [Source: CARE Ratings symbols and definitions]

That difference matters. AAA does not mean "no risk". AA does not mean "weak". Both are rating categories, not repayment promises.

Where AA+, AA and AA- Fit

The plus and minus signs matter.

Rating agencies often use modifiers such as `+` and `-` within categories from AA to C to show relative standing. AA+ is stronger than AA within the AA category. AA is stronger than AA-. AA- is still within the AA family, but it sits closer to the A category than AA+ does.

This is why a bond labelled AA+ should not be casually grouped with AA- without further review. Both may be called AA-rated in shorthand, but the risk signal is not identical.

Why AA Bonds Usually Offer More Yield Than AAA Bonds

Bond yields are not random. They are the market's way of pricing several things at once: credit risk, liquidity, tenure, demand, interest-rate expectations, structure and sometimes investor perception.

All else equal, an AA-rated bond may need to offer a higher yield than a similar AAA-rated bond because investors are taking a slightly higher credit-risk exposure in the rating agency's view. That additional yield is often called a spread or risk premium.

But "higher yield" should not be read as "better opportunity". It should be read as a question:

Why is the yield higher?

Sometimes the answer is credit quality. Sometimes it is tenure. Sometimes it is lower liquidity in the secondary market. Sometimes it is a security structure, a call option, a sector-specific risk, or simply market demand at that point in time.

This is where credit spread becomes useful. Credit spread is the additional yield a corporate bond offers over a comparable government security. It helps investors separate headline yield from the extra risk premium embedded in that yield. For a deeper explanation, see Equirize's guide to credit spread in bonds.

When comparing AAA vs AA bonds, do not compare yield alone. Compare yield after matching maturity, coupon structure, payout frequency, seniority, liquidity and tax treatment.

Rating is a Starting Filter, Not a Final Decision

A rating can reduce noise. It gives investors a first view of how a rating agency assesses credit risk. But a bond is still a specific instrument issued by a specific entity under specific terms.

Two bonds with the same rating can behave differently.

One may be issued by a large public-sector entity with long operating history. Another may be issued by a private issuer in a more cyclical sector. One may be secured with defined cover. Another may be unsecured or subordinated. One may mature in 18 months. Another may mature in 8 years.

The rating symbol is only the beginning.

Check the Issuer, Not Just the Symbol

Tenure changes risk. A three-year bond and a ten-year bond with the same rating are not identical exposures. Longer tenure increases the period over which business, rate-cycle and liquidity conditions can change.

Security and seniority also matter. Secured, unsecured, senior and subordinated instruments can carry different risk implications even when the issuer name is familiar. Investors should review the offer document for security cover, charge details, trustee information and repayment terms.

Check Liquidity and Exit Route

Listed bonds may be sold before maturity, but that does not guarantee a buyer at the price an investor wants. Secondary-market liquidity can vary by issuer, issue size, coupon, remaining tenure and current market conditions.

This matters for both AAA and AA bonds. If you may need to exit before maturity, liquidity risk is not a footnote. It is part of the decision.

For a fuller due-diligence structure, see Equirize's corporate bond evaluation checklist.

What Can Change After You Buy: Outlooks, Watches, and Downgrades

Credit ratings are monitored. They can be affirmed, upgraded, downgraded, placed on watch, or assigned an outlook depending on issuer performance and changing conditions.

A stable outlook generally suggests that the agency does not currently expect a rating change over the relevant horizon. A positive outlook may indicate potential upward pressure. A negative outlook may indicate potential downward pressure. A rating watch usually signals that a specific event or development could affect the rating.

Investors should not treat these labels mechanically. A negative outlook does not automatically mean default. A stable outlook does not eliminate risk. But these signals are useful because they tell you where the agency sees pressure building or easing.

A downgrade can affect the market price of a bond. It may also affect liquidity, because some investors or institutions have internal rules around minimum rating categories. Even if the issuer continues to service payments on time, the bond's market value can move if investors demand a higher yield after a rating change.

This is one reason the offer document and latest rating rationale deserve attention before subscribing, and not only after something changes.

When AAA May Fit and When AA May Fit

This section is educational and not investment advice. The right bond depends on the investor's objective, risk tolerance, time horizon, tax situation, liquidity needs and portfolio concentration.

| Investor priority | How AAA may be viewed | How AA may be viewed | Caution |

| Lower credit-risk exposure | May be preferred by investors who want the highest rating category available | May still be high-grade, but involves a lower rating category | Capital remains at risk in both cases |

| Additional yield | May offer lower yield than AA, all else equal | May offer higher yield for additional risk | Extra yield must be evaluated against issuer and instrument risk |

| Short holding period | Rating helps, but liquidity still matters | Liquidity and market pricing need closer review | Early exit is not guaranteed |

| Defined cash-flow planning | Coupon schedule and maturity can be matched to goals | Same, if risk level is acceptable | Payments depend on issuer performance |

| Portfolio diversification | Can form part of a rating-diversified bond allocation | Can add yield diversity if sized carefully | Diversification does not eliminate risk |

The practical question is not "Is AAA better than AA?" It is: "What risk am I accepting, and is the yield, tenure and structure appropriate for my objective?"

How to Compare Two Bonds with Different Ratings

If you are comparing one AAA-rated bond and one AA-rated bond, use a sequence rather than a shortcut.

First, match maturity. A short-tenure AA bond and a long-tenure AAA bond are not a clean comparison. Tenure affects interest-rate risk, liquidity and reinvestment planning.

Second, compare yield to maturity, not only coupon. Coupon tells you the stated interest rate on face value. Yield to maturity incorporates purchase price, coupon, redemption value and time to maturity. Equirize's yield to maturity guide explains this metric in more detail.

Third, read the rating rationale. Look for the agency's stated strengths, weaknesses and rating sensitivities.

Fourth, review structure. Is the instrument secured or unsecured? Senior or subordinated? Does it have a call option? What is the repayment schedule? What covenants or security cover are disclosed?

Fifth, assess liquidity. Check whether the bond is listed, how actively it trades, and what early exit may realistically involve.

Sixth, consider tax and concentration. Interest income from bonds is generally taxed according to the investor's applicable slab, while capital gains treatment depends on holding period and instrument type. Tax treatment depends on individual circumstances and may change. Please consult a qualified tax advisor.

Finally, read the offer document and risk factors. Ratings compress a lot of analysis into a symbol. The offer document gives you the instrument terms that the symbol cannot fully capture.

EquiRize View: Ratings Help You Ask Better Questions

Equirize is a SEBI-registered Online Bond Platform Provider (OBPP) and a stock broker in the debt segment of BSE and NSE. SEBI formalised the registration and regulatory framework for OBPPs through its circular dated November 14, 2022. Source: SEBI OBPP circular

For investors, the useful role of a bond platform is not to make a rating look like a verdict. It is to make the relevant information easier to review: issuer details, rating, maturity, payout schedule, yield metrics, documents and risk factors.

On Equirize, investors can compare listed bonds by rating, maturity, coupon schedule, YTM and issuer details before reviewing the offer document. You can also read more about Equirize's regulatory profile.

The rating helps you decide what to examine next. The decision still needs context.

Final Take

AAA vs AA bonds differ in degree, not in kind. Both belong near the top of the rating scale, but AAA represents the highest rating category while AA sits one step below it with its own internal gradations.

That difference can affect yield, market pricing, downgrade sensitivity and investor suitability. But it should never be reduced to a simple rule such as "AAA is always right" or "AA is better because it pays more."

Use the rating as a first filter. Then review the issuer, rating rationale, tenure, security, seniority, liquidity, tax treatment, concentration and offer document. The better question is not only what the rating is. It is what the rating does and does not tell you.